As per Intent Market Research, the Flexible Electronics Market was valued at USD 39.8 billion in 2023 and will surpass USD 82.2 billion by 2030; growing at a CAGR of 10.9% during 2024 - 2030.

The flexible electronics market is expanding rapidly as technological innovations continue to transform how electronic devices are designed and used across various industries. Flexible electronics are characterized by the ability to bend, fold, stretch, and conform to different shapes, making them ideal for applications in consumer electronics, automotive, healthcare, and other sectors. This ability to integrate electronic functionality into non-traditional forms has opened up numerous opportunities for growth in areas such as wearables, automotive electronics, and energy harvesting.

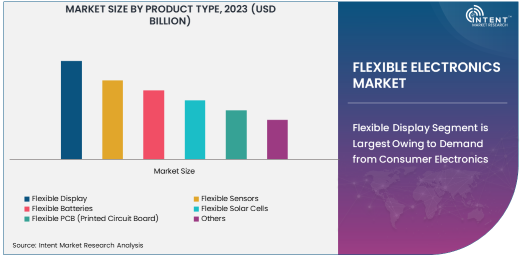

Flexible Display Segment is Largest Owing to Demand from Consumer Electronics

Flexible displays are the largest segment in the flexible electronics market, driven by the growing demand for innovative and portable consumer electronics. The consumer electronics industry has increasingly embraced flexible displays for smartphones, tablets, wearables, and televisions, as these displays offer superior durability, lightweight construction, and the ability to be integrated into unconventional designs. Flexible OLED (Organic Light Emitting Diode) technology, in particular, is a key driver, providing high-quality displays that are bendable and capable of offering high resolution and vibrant colors, which enhances the consumer experience.

As mobile devices and wearable technology continue to evolve, flexible displays are expected to become even more prevalent, enabling new form factors and features in consumer electronics. The widespread adoption of flexible displays is also supported by ongoing improvements in manufacturing processes and materials, which help to reduce costs and improve performance. This segment’s growth is expected to continue in the coming years as manufacturers explore new applications, including foldable smartphones and flexible TV screens.

Automotive Segment is Fastest Growing Owing to Technological Advancements

The automotive industry is the fastest-growing sector in the flexible electronics market, with increasing adoption of flexible sensors and displays in vehicles. Automotive manufacturers are increasingly incorporating flexible electronics into dashboards, instrument clusters, and infotainment systems, as well as for advanced driver assistance systems (ADAS) and sensors. Flexible electronics are being integrated into vehicles to create more user-friendly, energy-efficient, and aesthetically pleasing designs while also providing added functionality in areas like in-cabin displays and environmental monitoring.

In addition, flexible electronics are playing a crucial role in the development of electric vehicles (EVs) and autonomous driving technologies, where lightweight and flexible components are essential for efficiency and performance. As automakers strive to create more connected and intuitive vehicles, the demand for flexible electronic components will continue to grow, offering vast potential for further innovations in this sector.

Printed Electronics Technology is Largest Owing to Cost Efficiency and Scalability

Printed electronics, which are a significant subsegment within the flexible electronics technology category, are the most widely used due to their scalability, cost efficiency, and ability to produce large-area flexible devices. This technology enables the manufacturing of thin, lightweight, and flexible circuits using printing techniques such as screen printing, inkjet printing, and gravure printing. The cost-effective nature of printed electronics allows for high-volume production, making them ideal for mass-market applications like flexible displays, sensors, and smart packaging.

The growing demand for affordable, large-area electronics in consumer electronics, automotive, and healthcare applications has further boosted the adoption of printed electronics. As innovations continue in ink and material development, printed electronics are expected to see widespread use in new products such as smart textiles, flexible batteries, and energy-efficient lighting systems.

Wearable Devices Application is Largest Owing to Consumer Demand for Smart Technology

Wearable devices remain the largest application of flexible electronics, primarily due to the increasing demand for health monitoring and fitness tracking solutions. The rise of smartwatches, fitness bands, and medical devices has created a strong market for flexible circuits, displays, and sensors, as these devices require lightweight, comfortable, and durable components. Flexible electronics enable the development of smaller, more efficient devices that can be seamlessly integrated into wearables without compromising on performance or comfort.

As health and fitness tracking becomes more mainstream, the wearable devices market will continue to drive demand for flexible electronics, especially as more advanced sensors and components are integrated into these devices. The trend toward personalized health monitoring, as well as the growing interest in augmented reality (AR) glasses and other wearable tech, is expected to further fuel the growth of this segment.

Asia Pacific Region is Largest Owing to Robust Manufacturing Capabilities

The Asia Pacific region holds the largest share of the flexible electronics market, owing to its strong manufacturing infrastructure, technological advancements, and growing demand for flexible devices. Countries such as China, Japan, South Korea, and Taiwan are at the forefront of flexible electronics production, with a large number of companies based in these countries driving innovation and meeting the growing demand from global markets. The presence of leading consumer electronics manufacturers, along with substantial investments in research and development, has helped to establish the region as the center of the flexible electronics market.

Asia Pacific’s dominance is also supported by its large consumer base, which is fueling the growth of applications such as wearable devices, automotive electronics, and smart packaging. Additionally, the region benefits from favorable government policies and significant investments in technology development, which continue to foster growth in flexible electronics.

Leading Companies and Competitive Landscape

The competitive landscape of the flexible electronics market is characterized by a mix of well-established technology companies and new entrants focused on innovation. Major players such as LG Electronics, Samsung Electronics, Sony Corporation, and Panasonic Corporation are at the forefront of the flexible electronics market, driving advancements in flexible displays, sensors, and other key components. These companies leverage their extensive R&D capabilities, global reach, and established manufacturing expertise to gain a competitive edge.

In addition to these industry giants, several emerging companies are also making their mark, particularly in niche segments like flexible solar cells, stretchable electronics, and smart textiles. Strategic collaborations, mergers, and acquisitions are common in the market, with companies seeking to strengthen their technological capabilities and expand their market presence. As demand for flexible electronics continues to rise, competition will intensify, with companies striving to develop more innovative, cost-effective, and high-performance products to meet the evolving needs of the market.

Recent Developments:

- LG Electronics has launched a new flexible OLED display for automotive applications, enhancing the vehicle’s dashboard with curved, lightweight, and durable screens.

- Panasonic Corporation has entered a partnership with a leading automotive manufacturer to supply flexible batteries for electric vehicle applications, expanding its portfolio in energy storage.

- Sony Corporation unveiled its next-generation flexible sensors that offer enhanced performance for wearable healthcare devices, improving user experience and monitoring accuracy.

- 3M Company recently acquired a flexible sensor technology company to integrate its advanced sensors into 3M's healthcare and industrial applications, aiming to diversify its offerings in the flexible electronics market.

- Dow Inc. has invested heavily in the development of high-performance conductive inks for printed electronics, enhancing the manufacturing process for flexible circuits and displays.

List of Leading Companies:

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Sony Corporation

- Flexible Electronics Inc.

- BASF SE

- Applied Materials Inc.

- Dow Inc.

- Koninklijke Philips N.V.

- 3M Company

- AIST (National Institute of Advanced Industrial Science and Technology)

- Xiaomi Corporation

- Nanosys Inc.

- Sensirion AG

- Flex Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 39.8 Billion |

|

Forecasted Value (2030) |

USD 82.2 Billion |

|

CAGR (2024 – 2030) |

10.9% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Flexible Electronics Market By Product Type (Flexible Display, Flexible Sensors, Flexible Batteries, Flexible Solar Cells, Flexible PCB), By End-User Industry (Consumer Electronics, Automotive, Healthcare, Aerospace & Defense, Industrial & Manufacturing, Retail & Advertising, Energy & Power), By Technology (Organic Electronics, Inorganic Electronics, Hybrid Electronics, Printed Electronics, Stretchable Electronics), and By Application (Wearable Devices, Automotive Electronics, Healthcare Devices, Smart Packaging, Smart Textiles, Consumer Electronics, Industrial Automation, Energy Harvesting) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

LG Electronics, Samsung Electronics, Panasonic Corporation, Sony Corporation, Flexible Electronics Inc., BASF SE, Applied Materials Inc., Dow Inc., Koninklijke Philips N.V., 3M Company, AIST (National Institute of Advanced Industrial Science and Technology), Xiaomi Corporation, Nanosys Inc., Sensirion AG, Flex Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Flexible Electronics Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Flexible Display |

|

4.2. Flexible Sensors |

|

4.3. Flexible Batteries |

|

4.4. Flexible Solar Cells |

|

4.5. Flexible PCB (Printed Circuit Board) |

|

4.6. Others |

|

5. Flexible Electronics Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Consumer Electronics |

|

5.2. Automotive |

|

5.3. Healthcare |

|

5.4. Aerospace & Defense |

|

5.5. Industrial & Manufacturing |

|

5.6. Retail & Advertising |

|

5.7. Energy & Power |

|

5.8. Others |

|

6. Flexible Electronics Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Organic Electronics |

|

6.2. Inorganic Electronics |

|

6.3. Hybrid Electronics |

|

6.4. Printed Electronics |

|

6.5. Stretchable Electronics |

|

7. Flexible Electronics Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Wearable Devices |

|

7.2. Automotive Electronics |

|

7.3. Healthcare Devices |

|

7.4. Smart Packaging |

|

7.5. Smart Textiles |

|

7.6. Consumer Electronics (Smartphones, Tablets) |

|

7.7. Industrial Automation |

|

7.8. Energy Harvesting |

|

7.9. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Flexible Electronics Market, by Product Type |

|

8.2.7. North America Flexible Electronics Market, by End-User Industry |

|

8.2.8. North America Flexible Electronics Market, by Technology |

|

8.2.9. By Country |

|

8.2.9.1. US |

|

8.2.9.1.1. US Flexible Electronics Market, by Product Type |

|

8.2.9.1.2. US Flexible Electronics Market, by End-User Industry |

|

8.2.9.1.3. US Flexible Electronics Market, by Technology |

|

8.2.9.2. Canada |

|

8.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. LG Electronics |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Samsung Electronics |

|

10.3. Panasonic Corporation |

|

10.4. Sony Corporation |

|

10.5. Flexible Electronics Inc. |

|

10.6. BASF SE |

|

10.7. Applied Materials Inc. |

|

10.8. Dow Inc. |

|

10.9. Koninklijke Philips N.V. |

|

10.10. 3M Company |

|

10.11. AIST (National Institute of Advanced Industrial Science and Technology) |

|

10.12. Xiaomi Corporation |

|

10.13. Nanosys Inc. |

|

10.14. Sensirion AG |

|

10.15. Flex Ltd. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Flexible Electronics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Flexible Electronics Market. The research methodoloagy encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

a

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Flexible Electronics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA