As per Intent Market Research, the Fish Skin Disease Market was valued at USD 2.1 billion in 2023 and will surpass USD 3.8 billion by 2030; growing at a CAGR of 8.5% during 2024 - 2030.

The fish skin disease market is experiencing growth due to the rising demand for fish products, along with increased awareness of fish health management in aquaculture and fisheries. Fish, whether farmed or wild-caught, are vulnerable to various skin diseases that can significantly impact their growth, survival, and marketability. These diseases not only affect the fish population but also pose significant economic challenges to the industry. As fish farming has expanded globally, the need for effective disease management has grown, leading to an increased demand for treatments and preventive measures.

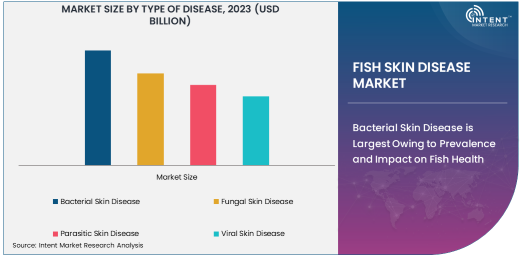

This market encompasses various disease types, treatment options, and affected fish species, with each segment contributing to the market’s dynamics. The following sections delve into the largest and fastest-growing subsegments within each category, highlighting the key factors driving growth across the industry.

Bacterial Skin Disease is Largest Owing to Prevalence and Impact on Fish Health

Bacterial skin diseases are the largest subsegment in the fish skin disease market due to their widespread occurrence and significant impact on both freshwater and saltwater fish populations. Bacterial infections, such as columnaris and Aeromonas, can spread rapidly in aquaculture settings, leading to high mortality rates among fish. These diseases affect fish of all ages and can result in lesions, skin ulcers, and systemic infections, which hinder the overall health of fish populations. The ease of transmission in overcrowded environments such as fish farms makes bacterial skin diseases a key concern for the industry.

The large market share of bacterial skin diseases is driven by their direct impact on fish farming operations and the significant economic losses they cause. Effective management of bacterial infections often involves the use of antibiotics and biosecurity measures. With the growing demand for fish products, especially in regions like Asia and North America, the need for effective bacterial disease management has resulted in increased research and development of novel antibiotics and alternative treatment methods.

Saltwater Fish is Largest Owing to Higher Economic Value and Market Demand

Saltwater fish are the largest segment in the fish type category, driven by their higher economic value in both domestic and international markets. Saltwater species like salmon, tuna, and sea bass are highly sought after in global seafood trade, particularly in high-value markets in Europe, North America, and Asia. These fish are more prone to certain skin diseases due to the unique conditions of marine environments, which can exacerbate the prevalence of diseases such as bacterial and parasitic infections. Saltwater fish farms are also vulnerable to environmental stressors such as water temperature fluctuations and overcrowding, which contribute to the spread of skin diseases.

The substantial market size for saltwater fish can be attributed to the rising demand for seafood and the lucrative nature of saltwater fish farming. As aquaculture expands to meet global seafood consumption, the focus on managing and preventing diseases in saltwater fish farms has become a priority. In addition, the advanced technology and infrastructure required for saltwater fish farming make it a dominant segment in the fish skin disease market.

Antiparasitic Treatments are Fastest Growing Owing to Rising Parasite Resistance

Antiparasitic treatments are the fastest-growing subsegment in the fish skin disease market, driven by the increasing prevalence of parasitic infections in both freshwater and saltwater fish. Parasites like sea lice, Ichthyophthirius, and monogeneans pose a significant threat to fish health, and the growing resistance to conventional treatments has accelerated the development of more effective antiparasitic solutions. These parasites can cause skin lesions, gill damage, and overall health deterioration, leading to high mortality rates in aquaculture settings.

The rise in parasitic resistance to traditional treatments has spurred innovation in antiparasitic treatments, including the development of new formulations and delivery methods. Furthermore, the demand for organic and eco-friendly treatments is driving the growth of the antiparasitic subsegment. With increasing investment in research and development, the antiparasitic treatment market is expected to continue growing, especially as aquaculture operations scale up and seek more sustainable solutions to manage disease outbreaks.

Aquaculture End-Use Industry is Largest Owing to Rising Fish Farming Practices

The aquaculture industry is the largest end-use segment for fish skin disease treatments, owing to the rapid expansion of fish farming practices worldwide. Aquaculture provides a significant portion of the global fish supply, and as the industry continues to grow, the need for effective disease management is becoming increasingly important. Skin diseases in fish farming can lead to severe economic losses, making the adoption of treatment solutions essential for maintaining healthy stocks and ensuring high-quality fish production.

Aquaculture is a highly controlled environment where disease outbreaks can be devastating to fish populations. As fish farming operations scale up to meet the rising demand for seafood, especially in Asia-Pacific and Latin America, there is a growing need for efficient treatment options for fish skin diseases. This trend is expected to continue as more aquaculture farms adopt advanced technologies for disease prevention and management.

Asia-Pacific is Largest Region Owing to Dominance in Aquaculture Production

Asia-Pacific is the largest region in the fish skin disease market, driven by the dominance of countries like China, India, and Vietnam in global aquaculture production. The region accounts for the majority of global fish farming, producing various species of both freshwater and saltwater fish. As aquaculture in Asia-Pacific continues to expand to meet the increasing demand for fish and seafood, the prevalence of fish skin diseases also rises, necessitating greater investments in disease prevention and treatment.

In this region, the focus is on improving fish health and productivity, which has led to increased adoption of treatments for skin diseases. The growing adoption of aquaculture in countries with vast coastlines and abundant freshwater resources ensures that Asia-Pacific will remain the largest market for fish skin disease treatments. Furthermore, the region is a hub for research and development, particularly in developing new treatment options to combat diseases affecting fish stocks.

Competitive Landscape and Leading Companies

The fish skin disease market is competitive, with several key players leading the development of new treatment solutions. Companies such as Elanco Animal Health, Zoetis, and Merck Animal Health are at the forefront, offering a wide range of antibiotics, antifungal, antiparasitic treatments, and vaccines to control and prevent skin diseases in fish. These companies are investing heavily in research and development to address the challenges posed by parasitic resistance and evolving bacterial pathogens.

The competitive landscape is characterized by the presence of both global corporations and specialized players in the aquaculture health sector. Strategic partnerships, acquisitions, and investments in innovation are common, as companies seek to expand their product portfolios and geographic reach. As the market continues to grow, the focus will be on sustainable and eco-friendly treatments, offering significant opportunities for new entrants and established players alike.

Recent Developments:

- Zoetis Inc. launched a new line of vaccines for fish that target common bacterial skin diseases, aimed at improving fish health in aquaculture settings.

- Merck & Co., Inc. expanded its product portfolio with an innovative antibiotic treatment specifically designed to combat fungal skin diseases in fish.

- Boehringer Ingelheim received approval for a new parasitic treatment designed for use in fish farms, significantly reducing skin infections caused by parasites.

- Elanco Animal Health announced a partnership with leading aquaculture farms to provide comprehensive skin disease management programs, incorporating both vaccines and antimicrobial treatments.

- Virbac introduced a new range of skin disease management products tailored for ornamental fish, focusing on bacterial infections and skin lesions caused by poor water conditions.

List of Leading Companies:

- Alltech, Inc.

- BASF SE

- Boehringer Ingelheim

- Cargill, Incorporated

- Dechra Pharmaceuticals

- Elanco Animal Health

- Hy-Line International

- Kemin Industries

- Kyorin Pharmaceutical Co., Ltd.

- Merck & Co., Inc.

- Nutreco N.V.

- Phibro Animal Health

- Vetoquinol S.A.

- Virbac

- Zoetis Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 2.1 Billion |

|

Forecasted Value (2030) |

USD 3.8 Billion |

|

CAGR (2024 – 2030) |

8.5% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Fish Skin Disease Market by Type of Disease (Bacterial Skin Disease, Fungal Skin Disease, Parasitic Skin Disease, Viral Skin Disease), by Fish Type (Freshwater Fish, Saltwater Fish), by Treatment Type (Antibiotics, Antifungal Treatments, Antiparasitic Treatments, Vaccines), by End-Use Industry (Aquaculture, Fisheries) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Alltech, Inc., BASF SE, Boehringer Ingelheim, Cargill, Incorporated, Dechra Pharmaceuticals, Elanco Animal Health, Kemin Industries, Kyorin Pharmaceutical Co., Ltd., Merck & Co., Inc., Nutreco N.V., Phibro Animal Health, Vetoquinol S.A., Zoetis Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

.jpg)

.jpg)