As per Intent Market Research, the Esophageal Cancer Drugs Market was valued at USD 3.8 billion in 2023 and will surpass USD 6.1 billion by 2030; growing at a CAGR of 7.1% during 2024 - 2030.

The global esophageal cancer drugs market has shown significant growth due to increasing incidences of esophageal cancer, advancements in drug development, and improving healthcare infrastructure. Esophageal cancer, a highly aggressive and prevalent type of cancer, requires specialized therapies, which has prompted the market to grow steadily. The market includes a range of drug types, therapy options, and end-user categories, catering to various stages of treatment, from diagnosis to long-term management. In this market, drug types such as chemotherapy, targeted therapy, and immunotherapy have gained substantial traction. As we move forward, the demand for innovative and effective cancer therapies is expected to rise, expanding the market even further.

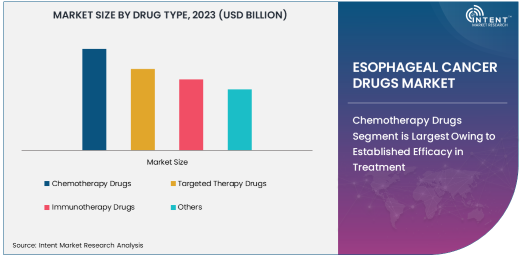

Chemotherapy Drugs Segment is Largest Owing to Established Efficacy in Treatment

The chemotherapy drugs segment holds the largest share in the esophageal cancer drugs market. Chemotherapy has long been the backbone of cancer treatment, offering a broad range of drugs that target rapidly dividing cells, which include cancer cells. In esophageal cancer, chemotherapy is often used in conjunction with surgery or radiation therapy, especially in advanced stages. Drugs like cisplatin, 5-fluorouracil (5-FU), and paclitaxel are widely used and have demonstrated proven efficacy in treating esophageal cancer. The widespread use of chemotherapy drugs is further supported by their availability, affordability, and proven clinical benefits.

Chemotherapy remains the go-to therapy for esophageal cancer, particularly in patients who are not eligible for surgery or those who have advanced-stage disease. Despite the emergence of newer drug classes like immunotherapy and targeted therapies, chemotherapy continues to dominate due to its extensive use in standard treatment regimens. Furthermore, chemotherapy plays an essential role in pre-operative and adjuvant settings, making it indispensable in the treatment of esophageal cancer.

Combination Therapy Segment is Fastest Growing Due to Enhanced Efficacy

The combination therapy segment is the fastest-growing within the esophageal cancer drugs market. Combination therapy, which involves using two or more drugs with different mechanisms of action, has shown promising results in treating various types of cancer, including esophageal cancer. Combining chemotherapy with immunotherapy or targeted therapy has proven to improve the overall survival rate and response rates among patients. For instance, the combination of immune checkpoint inhibitors like pembrolizumab (Keytruda) with chemotherapy is becoming increasingly popular in treating advanced esophageal cancer.

Combination therapy is gaining attention because it addresses multiple pathways involved in cancer progression, offering more comprehensive and effective treatment. With increasing research and clinical trials supporting the efficacy of combined treatment approaches, this segment is expected to grow rapidly, driven by higher success rates in clinical outcomes and more personalized treatment options for patients.

Oncology Clinics Segment is Largest End-User Owing to Specialized Care

Oncology clinics are the largest end-user segment for esophageal cancer drugs. These clinics are specialized centers focused on the diagnosis, treatment, and management of cancer, providing tailored therapeutic solutions for esophageal cancer patients. Oncology clinics are equipped with the latest technologies and offer access to advanced cancer drugs, including chemotherapy, targeted therapies, and immunotherapies. The increasing number of oncology clinics globally, along with better access to specialized care, has contributed to the growth of this segment.

Patients often visit oncology clinics for second opinions, treatment plans, and participation in clinical trials. These clinics are the main point of contact for cancer patients, offering expertise in cancer management and providing a range of treatments. The growing demand for specialized cancer treatment has made oncology clinics the most significant end-user segment in the market.

Retail Pharmacies Segment is Leading in Distribution Channels Due to Accessibility

The retail pharmacies segment is the leading distribution channel for esophageal cancer drugs. Retail pharmacies, which include both physical and online stores, play a key role in ensuring that patients have easy access to their prescribed cancer medications. These pharmacies cater to outpatient care, offering chemotherapy drugs and supportive care drugs that are essential for esophageal cancer patients. Retail pharmacies are strategically positioned in urban and rural areas, making them highly accessible to patients.

With the growing preference for outpatient care and convenience, retail pharmacies are benefiting from an increase in prescriptions for cancer drugs. Furthermore, the rise of online pharmacies has further expanded the reach of retail pharmacies, especially in regions with limited access to hospitals and clinics. This segment is expected to continue leading in terms of distribution, owing to its broad accessibility and ability to deliver medications in a timely manner.

Asia Pacific Region is the Fastest Growing Due to Increased Cancer Incidence

Asia Pacific is the fastest-growing region in the esophageal cancer drugs market. The region has seen a significant rise in the incidence of esophageal cancer, particularly in countries such as China, India, and Japan, due to a combination of lifestyle factors, smoking, alcohol consumption, and dietary habits. This surge in cancer cases has driven the demand for esophageal cancer drugs. Additionally, the Asia Pacific region has been investing heavily in healthcare infrastructure, research, and drug development, making it an attractive market for pharmaceutical companies.

The rapid growth of the pharmaceutical sector and increasing awareness about cancer treatment options in the region are key drivers of market growth. With improving healthcare systems, government initiatives, and growing healthcare expenditures, the Asia Pacific market is expected to expand significantly over the next few years. This growth will be fueled by both the increasing demand for cancer drugs and the rising healthcare access in emerging economies.

Leading Companies and Competitive Landscape

The esophageal cancer drugs market is highly competitive, with major pharmaceutical companies and biotech firms leading the market through innovative drug development and strategic partnerships. Companies like Merck & Co., Bristol-Myers Squibb, and Roche are at the forefront, offering a range of oncology drugs, including immunotherapies, chemotherapy agents, and targeted therapies. These companies invest significantly in research and clinical trials to develop new and more effective treatments for esophageal cancer, enhancing patient outcomes and survival rates.

The competitive landscape is marked by mergers and acquisitions, collaborations, and partnerships to bring new therapies to market faster. Leading firms are increasingly focusing on combination therapies to provide more effective treatments for patients. As a result, the market is expected to see continued innovation, strategic partnerships, and increasing competition to cater to the growing global demand for esophageal cancer treatments.

Recent Developments:

- Merck & Co. received FDA approval for Keytruda in the treatment of esophageal cancer, offering new hope for patients with advanced disease.

- Bristol-Myers Squibb announced a partnership with a biotechnology firm to jointly develop new targeted therapies for esophageal cancer patients, expanding their oncology pipeline.

- AstraZeneca launched a clinical trial focused on the combination of immunotherapy and chemotherapy to treat esophageal cancer, aiming to improve survival rates.

- Pfizer's new drug, Palbociclib, received regulatory approval in Europe for use in combination with chemotherapy to treat esophageal cancer in patients with metastatic disease.

- Roche's Tecentriq was granted approval by the FDA for a new indication to treat esophageal cancer, furthering its position as a key player in immuno-oncology.

List of Leading Companies:

- Merck & Co., Inc.

- Bristol-Myers Squibb

- AstraZeneca PLC

- Roche Holding AG

- Pfizer Inc.

- Novartis AG

- Eli Lilly and Company

- Johnson & Johnson

- Amgen Inc.

- AbbVie Inc.

- Boehringer Ingelheim

- Sanofi S.A.

- Gilead Sciences

- Takeda Pharmaceutical Company Limited

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.8 Billion |

|

Forecasted Value (2030) |

USD 6.1 Billion |

|

CAGR (2024 – 2030) |

7.1% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Esophageal Cancer Drugs Market By Drug Type (Chemotherapy Drugs, Targeted Therapy Drugs, Immunotherapy Drugs), By Therapy Type (Monotherapy, Combination Therapy), By End-User (Hospitals, Oncology Clinics, Research Laboratories, Home Care Settings), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Merck & Co., Inc., Bristol-Myers Squibb, AstraZeneca PLC, Roche Holding AG, Pfizer Inc., Novartis AG, Eli Lilly and Company, Johnson & Johnson, Amgen Inc., AbbVie Inc., Boehringer Ingelheim, Sanofi S.A., Gilead Sciences, Takeda Pharmaceutical Company Limited, Bayer AG |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Esophageal Cancer Drugs Market, by Drug Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Chemotherapy Drugs |

|

4.2. Targeted Therapy Drugs |

|

4.3. Immunotherapy Drugs |

|

4.4. Others |

|

5. Esophageal Cancer Drugs Market, by Therapy Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Monotherapy |

|

5.2. Combination Therapy |

|

6. Esophageal Cancer Drugs Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Oncology Clinics |

|

6.3. Research Laboratories |

|

6.4. Home Care Settings |

|

7. Esophageal Cancer Drugs Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Hospital Pharmacies |

|

7.2. Retail Pharmacies |

|

7.3. Online Pharmacies |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Esophageal Cancer Drugs Market, by Drug Type |

|

8.2.7. North America Esophageal Cancer Drugs Market, by Therapy Type |

|

8.2.8. North America Esophageal Cancer Drugs Market, by End-User |

|

8.2.9. North America Esophageal Cancer Drugs Market, by Distribution Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Esophageal Cancer Drugs Market, by Drug Type |

|

8.2.10.1.2. US Esophageal Cancer Drugs Market, by Therapy Type |

|

8.2.10.1.3. US Esophageal Cancer Drugs Market, by End-User |

|

8.2.10.1.4. US Esophageal Cancer Drugs Market, by Distribution Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Merck & Co., Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Bristol-Myers Squibb |

|

10.3. AstraZeneca PLC |

|

10.4. Roche Holding AG |

|

10.5. Pfizer Inc. |

|

10.6. Novartis AG |

|

10.7. Eli Lilly and Company |

|

10.8. Johnson & Johnson |

|

10.9. Amgen Inc. |

|

10.10. AbbVie Inc. |

|

10.11. Boehringer Ingelheim |

|

10.12. Sanofi S.A. |

|

10.13. Gilead Sciences |

|

10.14. Takeda Pharmaceutical Company Limited |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Esophageal Cancer Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Esophageal Cancer Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Esophageal Cancer Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA