As per Intent Market Research, the ESIM Market was valued at USD 1.1 billion in 2023 and will surpass USD 4.8 billion by 2030; growing at a CAGR of 23.0% during 2024 - 2030.

The eSIM (embedded SIM) market has experienced significant growth due to the increasing adoption of digital SIM technology across various devices and industries. eSIM technology allows users to activate cellular plans remotely, eliminating the need for traditional SIM cards. With the rise in connected devices, the market has witnessed a surge in demand, particularly in sectors such as telecommunications, automotive, healthcare, and consumer electronics. eSIM provides increased flexibility and efficiency for both consumers and enterprises by offering remote provisioning capabilities, enabling easy device management and network transitions.

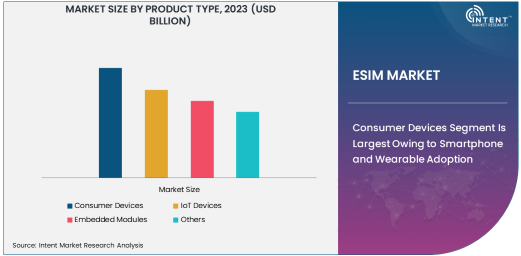

Consumer Devices Segment Is Largest Owing to Smartphone and Wearable Adoption

The consumer devices segment is the largest in the eSIM market, driven primarily by the increasing adoption of smartphones and wearables. With major smartphone manufacturers like Apple, Samsung, and Google integrating eSIM technology into their devices, the demand for eSIM-enabled consumer electronics has surged. Wearables, such as smartwatches, also contribute significantly to this segment’s growth, as eSIM provides enhanced connectivity options without the need for a physical SIM card. This segment's dominance can be attributed to the widespread consumer acceptance of eSIM-enabled smartphones, alongside the convenience and flexibility eSIM offers for users on the go.

The growing trend of eSIM adoption in consumer devices is expected to continue expanding as more regions embrace eSIM technology, making it easier for users to switch mobile operators or add multiple network profiles on a single device. Additionally, the demand for compact and efficient devices that provide better connectivity and space efficiency further boosts the growth of this subsegment.

Remote Provisioning Connectivity Type Is Fastest Growing Due to Seamless Activation

Remote provisioning is the fastest-growing connectivity type within the eSIM market. This method allows users to activate their mobile network profiles remotely, without needing to physically swap SIM cards or visit a carrier's store. As mobile operators and device manufacturers increasingly focus on improving the user experience, remote provisioning has become the preferred choice due to its convenience, security, and cost-effectiveness. It enables users to quickly activate a mobile service or switch operators, which is especially useful in the IoT and consumer electronics sectors where seamless device management is crucial.

The rise of remote provisioning is driven by its ability to simplify global roaming, streamline device deployments in industries like automotive and healthcare, and provide flexible connectivity for IoT devices. As eSIM technology evolves, more service providers are adopting remote provisioning to cater to a broader range of devices, further contributing to its rapid growth.

Telecommunications End-User Industry Is Largest Owing to Network Expansion

The telecommunications industry remains the largest end-user segment for eSIM technology, driven by the widespread deployment of eSIM-enabled devices and the growing demand for flexible and scalable connectivity solutions. Mobile operators are increasingly adopting eSIM technology to enhance customer experience and reduce operational costs associated with physical SIM cards. Telecommunications companies are also capitalizing on the benefits of eSIM to offer seamless switching between network operators and improved global roaming capabilities, which is essential for an increasingly mobile consumer base.

Telecom companies are focusing on expanding their eSIM offerings to include a broader array of devices, from smartphones to wearables and automotive solutions. This shift is expected to further solidify the telecom sector as the leading end-user of eSIM technology, supporting the growth of network infrastructures and enhancing mobile service offerings.

Asia Pacific Region Is Fastest Growing Due to Rapid Digitization

The Asia Pacific (APAC) region is expected to be the fastest-growing market for eSIM technology. Countries like China, India, Japan, and South Korea are witnessing rapid digitization, with increased demand for connected devices, smart homes, and IoT applications. In particular, the growing automotive industry in APAC is embracing eSIM technology to enable seamless connectivity for smart vehicles. Additionally, the rise of 5G networks across APAC countries further boosts the adoption of eSIM solutions, as it supports faster, more reliable, and flexible mobile network connectivity.

The expansion of telecom operators in APAC is also contributing to the growth of eSIM adoption, with many operators offering eSIM services for smartphones and IoT devices. The ongoing push for digital transformation in key industries, including automotive and healthcare, positions APAC as a key region for the expansion of eSIM technology.

Competitive Landscape and Leading Companies

The eSIM market is highly competitive, with several key players dominating the space. Leading companies such as Qualcomm, Apple, Gemalto (Thales Group), NXP Semiconductors, and Infineon Technologies are at the forefront, continuously innovating and expanding their eSIM portfolios to meet the growing demand. Qualcomm, for example, has been instrumental in developing eSIM technology for mobile devices, while Apple has integrated eSIM in its iPhone and other consumer devices, driving widespread adoption. Gemalto (now part of Thales Group) has strengthened its position with eSIM solutions for both consumer and IoT devices, while NXP and Infineon focus on providing secure eSIM modules for a wide range of applications.

As competition intensifies, companies are focusing on strategic partnerships, acquisitions, and product innovations to stay ahead in the market. The competitive landscape also reflects the growing emphasis on remote provisioning and the integration of eSIM solutions into 5G networks, which is expected to play a key role in shaping the future of mobile connectivity.

Recent Developments:

- In 2024, Apple introduced eSIM support for additional markets, making it easier for users to activate plans without needing a physical SIM, further solidifying its commitment to eSIM technology.

- Qualcomm unveiled new eSIM solutions designed for the automotive sector in Q1 2024, enabling seamless connectivity for autonomous vehicles and other smart transportation solutions.

- Thales Group acquired the eSIM business of a leading European company to bolster its portfolio in mobile connectivity and IoT solutions, focusing on remote provisioning services.

- Deutsche Telekom launched a new eSIM-based service in early 2024, targeting IoT device manufacturers with tailored connectivity solutions for large-scale operations.

- Verizon received regulatory approval in the U.S. in 2024 for a new service model that uses eSIM for easy activation of mobile plans across multiple devices, enhancing flexibility for consumers.

List of Leading Companies:

- Arm Holdings

- Apple Inc.

- Qualcomm Inc.

- Gemalto (Thales Group)

- Infineon Technologies AG

- NXP Semiconductors

- STMicroelectronics

- Verizon Communications

- AT&T Inc.

- Vodafone Group

- Deutsche Telekom AG

- Samsung Electronics

- Cisco Systems, Inc.

- Redmi (Xiaomi)

- Ublox

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.1 Billion |

|

Forecasted Value (2030) |

USD 4.8 Billion |

|

CAGR (2024 – 2030) |

23.0% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

eSIM Market By Product Type (Consumer Devices, IoT Devices, Embedded Modules), By Connectivity Type (Remote Provisioning, On-Device Provisioning), By End-User Industry (Telecommunications, Automotive, Healthcare, Consumer Electronics, Industrial Applications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Arm Holdings, Apple Inc., Qualcomm Inc., Gemalto (Thales Group), Infineon Technologies AG, NXP Semiconductors, STMicroelectronics, Verizon Communications, AT&T Inc., Vodafone Group, Deutsche Telekom AG, Samsung Electronics, Cisco Systems, Inc., Redmi (Xiaomi), Ublox |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. eSIM Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Consumer Devices |

|

4.2. IoT Devices |

|

4.3. Embedded Modules |

|

4.4. Others |

|

5. eSIM Market, by Connectivity Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Remote Provisioning |

|

5.2. On-Device Provisioning |

|

6. eSIM Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Telecommunications |

|

6.2. Automotive |

|

6.3. Healthcare |

|

6.4. Consumer Electronics |

|

6.5. Industrial Applications |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America eSIM Market, by Product Type |

|

7.2.7. North America eSIM Market, by Connectivity Type |

|

7.2.8. North America eSIM Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US eSIM Market, by Product Type |

|

7.2.9.1.2. US eSIM Market, by Connectivity Type |

|

7.2.9.1.3. US eSIM Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Arm Holdings |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Apple Inc. |

|

9.3. Qualcomm Inc. |

|

9.4. Gemalto (Thales Group) |

|

9.5. Infineon Technologies AG |

|

9.6. NXP Semiconductors |

|

9.7. STMicroelectronics |

|

9.8. Verizon Communications |

|

9.9. AT&T Inc. |

|

9.10. Vodafone Group |

|

9.11. Deutsche Telekom AG |

|

9.12. Samsung Electronics |

|

9.13. Cisco Systems, Inc. |

|

9.14. Redmi (Xiaomi) |

|

9.15. Ublox |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the eSIM Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the eSIM Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the eSIM Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA