As per Intent Market Research, the EPO Biomarkers Market was valued at USD 56.2 billion in 2023 and will surpass USD 83.7 billion by 2030; growing at a CAGR of 5.9% during 2024 - 2030.

The global EPO (Erythropoietin) biomarkers market has witnessed significant growth due to the increasing prevalence of chronic diseases, the rise in diagnostic testing, and technological advancements in biomarker detection. EPO biomarkers are widely used for detecting and monitoring diseases related to blood disorders, particularly anemia, chronic kidney disease (CKD), and certain cancers. These biomarkers help clinicians assess the production of red blood cells and guide therapeutic interventions, particularly in chronic conditions that affect erythropoiesis. As the demand for more precise and personalized diagnostic solutions grows, the EPO biomarkers market is set to expand across various segments, driven by both innovations in diagnostic technologies and a growing focus on patient-centered care.

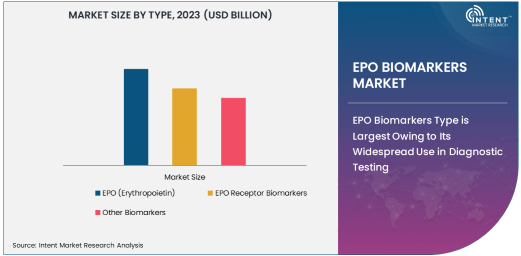

EPO Biomarkers Type is Largest Owing to Its Widespread Use in Diagnostic Testing

Among the various types of EPO biomarkers, EPO (Erythropoietin) remains the largest subsegment in the market, due to its central role in the diagnosis and management of blood-related disorders. Erythropoietin is a glycoprotein hormone that stimulates the production of red blood cells and is crucial for assessing conditions such as anemia, chronic kidney disease (CKD), and certain types of cancer. The EPO biomarker is extensively utilized in clinical settings to monitor treatment efficacy, evaluate disease progression, and predict patient outcomes. Its application in detecting erythropoiesis and guiding therapies for anemia has made it a staple in the diagnostic toolkits of healthcare providers, ensuring its dominance in the overall market.

In addition to its use in blood disorders, EPO testing is increasingly being employed to monitor patients receiving erythropoiesis-stimulating agents (ESAs) for anemia management. The rising number of patients diagnosed with anemia, particularly in regions with aging populations, further drives the demand for EPO biomarkers. The ability to quickly assess red blood cell production and manage anemia effectively has made EPO testing indispensable, thus maintaining its dominance in the EPO biomarkers market.

Cancer Application Segment is Fastest Growing Due to Rising Cancer Incidences

The cancer application segment is the fastest growing within the EPO biomarkers market, primarily due to the increasing incidence of cancer worldwide. Cancer patients often exhibit abnormal EPO levels, which can be indicative of the disease’s progression or the response to treatment. EPO biomarkers, particularly EPO receptor biomarkers, are gaining attention for their role in identifying patients who may develop anemia as a result of cancer or cancer treatments. This trend has accelerated the use of EPO biomarkers in oncology diagnostics, where early detection and personalized treatment plans are crucial for improving patient outcomes.

In addition to diagnosing anemia in cancer patients, EPO biomarkers are also being studied for their potential use in predicting cancer outcomes and monitoring the effectiveness of cancer therapies. With advances in precision medicine, the demand for biomarkers that can provide actionable insights into cancer progression is expected to rise, driving the growth of the EPO biomarkers market in the oncology sector. This growing trend reflects a broader shift towards more targeted and individualized treatment options in cancer care.

Hospitals Segment is Largest End-User Owing to Widespread Use in Diagnostics and Treatment

The hospitals segment is the largest end-user within the EPO biomarkers market, as hospitals are the primary settings for diagnostic testing and treatment administration. Hospitals regularly use EPO biomarkers for diagnosing and managing conditions such as anemia, CKD, and cancer. They offer comprehensive diagnostic and therapeutic services, making them key players in the utilization of biomarker-based tests. EPO testing, particularly for anemia and CKD, is frequently conducted in hospital settings to guide treatment decisions, track patient progress, and evaluate the effectiveness of therapies.

Additionally, hospitals are increasingly integrating advanced biomarker testing technologies into their diagnostics workflows to enhance patient care. As the healthcare landscape evolves, hospitals are adopting more sophisticated diagnostic tools to cater to the growing demand for precision medicine. This shift towards personalized healthcare solutions, coupled with the rising number of patients with chronic conditions, ensures that hospitals remain the dominant end-user of EPO biomarkers, driving the market forward.

North America is Largest Region Due to Advanced Healthcare Infrastructure and Rising Disease Prevalence

North America is the largest region in the EPO biomarkers market, driven by the advanced healthcare infrastructure, high adoption of diagnostic technologies, and the growing prevalence of chronic diseases such as anemia, cancer, and CKD. The region is home to some of the world’s leading pharmaceutical companies, diagnostic laboratories, and research institutions, which significantly contribute to the market's growth. In addition to the well-established healthcare systems, North America benefits from strong healthcare spending and a high level of awareness about chronic diseases, further propelling the demand for EPO biomarkers.

The increasing number of patients diagnosed with chronic conditions, coupled with the aging population, further supports the need for EPO biomarker testing in North America. Furthermore, the region’s focus on personalized medicine and precision diagnostics aligns with the growing role of biomarkers in disease management, particularly in the oncology and renal care sectors. As a result, North America remains the dominant region in the EPO biomarkers market, with sustained growth expected over the coming years.

Leading Companies and Competitive Landscape in the EPO Biomarkers Market

The EPO biomarkers market is highly competitive, with several global players driving innovations in diagnostics and therapeutic solutions. Key companies in the market include AbbVie, Roche Diagnostics, Thermo Fisher Scientific, Amgen Inc., and Siemens Healthineers, among others. These companies are leading the way with advanced diagnostic products that leverage EPO biomarkers for detecting and monitoring a range of blood disorders, particularly anemia, CKD, and cancer.

The competitive landscape is characterized by a combination of pharmaceutical giants, diagnostic companies, and research institutions that are collaborating to advance biomarker-based diagnostics and treatments. These collaborations, along with ongoing research and development efforts, are expected to foster continuous growth in the market. Additionally, companies are focusing on improving the accuracy, sensitivity, and accessibility of EPO biomarker tests, positioning themselves to capture a larger share of the expanding global market. The market is expected to continue evolving as innovations in molecular diagnostics and personalized medicine open new avenues for EPO biomarker applications.

Recent Developments:

- Amgen Inc. received FDA approval for Epogen (Epoetin alfa), a medication targeting EPO receptor biomarkers for treating anemia in chronic kidney disease patients.

- Thermo Fisher Scientific launched a new biomarker analysis tool to improve the accuracy of EPO biomarker testing, aimed at enhancing diagnostics in cancer and anemia management.

- AbbVie entered into a partnership with Roche Diagnostics to jointly develop a next-generation EPO receptor biomarker assay, aiming to improve the precision of chronic kidney disease diagnostics.

- Siemens Healthineers acquired a leading diagnostics company to enhance their portfolio in biomarker-based diagnostic solutions, expanding their presence in the EPO biomarkers market.

- Johnson & Johnson announced the development of a new EPO-targeted therapy for cancer-related anemia, leveraging biomarker-driven diagnostics for personalized treatment plans.

List of Leading Companies:

- AbbVie

- Roche Diagnostics

- Thermo Fisher Scientific

- Novartis

- Amgen Inc.

- Eli Lilly and Co.

- Merck & Co., Inc.

- Bristol Myers Squibb

- Abbott Laboratories

- Siemens Healthineers

- Johnson & Johnson

- Genentech

- Medtronic

- Bio-Rad Laboratories, Inc.

- BD (Becton, Dickinson and Company)

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 56.2 billion |

|

Forecasted Value (2030) |

USD 83.7 billion |

|

CAGR (2024 – 2030) |

5.9% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

EPO Biomarkers Market By Type (EPO, EPO Receptor Biomarkers, Other Biomarkers), By Application (Cancer, Chronic Kidney Disease (CKD), Anemia, Cardiovascular Diseases, Other Applications), By End-User Industry (Hospitals, Diagnostic Laboratories, Research Institutions, Pharmaceutical Companies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

AbbVie, Roche Diagnostics, Thermo Fisher Scientific, Novartis, Amgen Inc., Eli Lilly and Co., Merck & Co., Inc., Bristol Myers Squibb, Abbott Laboratories, Siemens Healthineers, Johnson & Johnson, Genentech, Medtronic, Bio-Rad Laboratories, Inc., BD (Becton, Dickinson and Company) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. EPO Biomarkers Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. EPO (Erythropoietin) |

|

4.2. EPO Receptor Biomarkers |

|

4.3. Other Biomarkers |

|

5. EPO Biomarkers Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Cancer |

|

5.2. Chronic Kidney Disease (CKD) |

|

5.3. Anemia |

|

5.4. Cardiovascular Diseases |

|

5.5. Other Applications |

|

6. EPO Biomarkers Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Diagnostic Laboratories |

|

6.3. Research Institutions |

|

6.4. Pharmaceutical Companies |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America EPO Biomarkers Market, by Type |

|

7.2.7. North America EPO Biomarkers Market, by Application |

|

7.2.8. North America EPO Biomarkers Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US EPO Biomarkers Market, by Type |

|

7.2.9.1.2. US EPO Biomarkers Market, by Application |

|

7.2.9.1.3. US EPO Biomarkers Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. AbbVie |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Roche Diagnostics |

|

9.3. Thermo Fisher Scientific |

|

9.4. Novartis |

|

9.5. Amgen Inc. |

|

9.6. Eli Lilly and Co. |

|

9.7. Merck & Co., Inc. |

|

9.8. Bristol Myers Squibb |

|

9.9. Abbott Laboratories |

|

9.10. Siemens Healthineers |

|

9.11. Johnson & Johnson |

|

9.12. Genentech |

|

9.13. Medtronic |

|

9.14. Bio-Rad Laboratories, Inc. |

|

9.15. BD (Becton, Dickinson and Company) |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the EPO Biomarkers Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the EPO Biomarkers Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the EPO Biomarkers Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA