As per Intent Market Research, the Genital Warts Treatment Market was valued at USD 1.1 billion in 2023 and will surpass USD 2.0 billion by 2030; growing at a CAGR of 9.0% during 2024 - 2030.

The genital warts treatment market is driven by the increasing prevalence of human papillomavirus (HPV) infections, which are the primary cause of genital warts. As the awareness of HPV-related diseases grows, there is a higher demand for effective treatments for genital warts. This market encompasses a range of treatment options, including prescription drugs, over-the-counter drugs, surgical treatments, and other therapeutic interventions, with a focus on providing relief and reducing the transmission of the virus. The availability of both topical and surgical treatments offers patients a variety of ways to manage and eliminate genital warts.

The market is also influenced by factors such as growing healthcare awareness, the availability of advanced treatments, and the increasing focus on sexual health. The rise in sexually transmitted diseases (STDs) globally, especially among young adults, has also spurred the growth of the genital warts treatment market. Additionally, the ease of access to various distribution channels such as online platforms and pharmacies has made these treatments more accessible, further contributing to market growth.

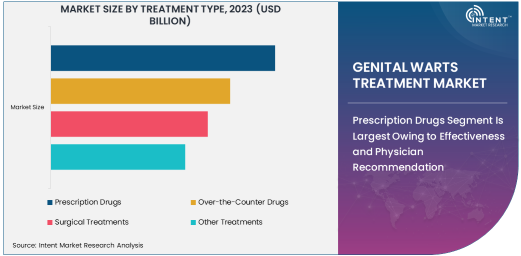

Prescription Drugs Segment Is Largest Owing to Effectiveness and Physician Recommendation

Among the various treatment options, prescription drugs represent the largest segment in the genital warts treatment market. Medications like imiquimod and podophyllotoxin are widely prescribed by healthcare professionals due to their proven efficacy in treating genital warts. Imiquimod, a topical immune response modifier, works by stimulating the body's immune system to fight the wart-causing virus. Podophyllotoxin, another common treatment, directly destroys the wart tissue and inhibits the replication of the virus. These prescription drugs are preferred for their targeted action, minimal invasiveness, and long-term effectiveness.

As physicians continue to recommend these drugs for patients, their widespread use maintains the dominant share of the prescription drugs segment. The growth of this segment is also fueled by the increasing availability of these drugs and their coverage by insurance plans, making them more accessible to a larger number of individuals. As a result, prescription drugs will continue to hold the largest share of the genital warts treatment market, driven by their efficacy and trusted usage in clinical practice.

Over-the-Counter Drugs Segment Is Fastest Growing Due to Convenience and Accessibility

The over-the-counter (OTC) drugs segment is the fastest-growing within the genital warts treatment market. OTC products such as wart removal creams and salicylic acid-based treatments are gaining popularity due to their ease of use, accessibility, and affordability. These treatments can be purchased without a prescription, making them particularly attractive for individuals seeking at-home management of genital warts. Salicylic acid, a common ingredient in OTC treatments, works by softening the wart tissue, allowing it to peel off gradually.

The convenience of purchasing these products at pharmacies, as well as online platforms, has contributed to the segment's rapid growth. As consumers become more comfortable managing their health issues privately, the demand for OTC treatments for genital warts is expected to rise. Additionally, the availability of a variety of formulations, including gels and creams, ensures that individuals can find a product that suits their needs, further fueling the growth of this segment.

Surgical Treatments Segment Holds Significant Share Due to Effectiveness in Severe Cases

Surgical treatments such as cryotherapy, electrocautery, and laser surgery hold a significant share of the genital warts treatment market due to their effectiveness in removing warts that do not respond to topical treatments. Cryotherapy involves freezing the warts with liquid nitrogen, causing them to fall off over time. Electrocautery uses heat to burn the warts, while laser surgery targets and vaporizes the wart tissue using focused light. These procedures are often used for more extensive or persistent warts that require professional intervention.

Although surgical treatments are more invasive compared to topical treatments, they remain a preferred choice for severe or recurrent cases. The increasing availability of skilled practitioners and advanced technology in hospitals and clinics contributes to the growth of this segment. As a result, surgical treatments will continue to play an important role in the genital warts treatment market, especially for individuals who need a more definitive solution to their condition.

Pharmacies Are Largest Distribution Channel Owing to Convenience and Accessibility

Pharmacies are the largest distribution channel in the genital warts treatment market. This is primarily due to the convenience and accessibility they offer to consumers seeking both prescription and over-the-counter treatments. Pharmacies provide a wide range of products, from topical treatments to prescription medications, making it easy for individuals to find suitable options for genital warts treatment. Moreover, the presence of licensed pharmacists ensures that customers receive proper guidance on the safe and effective use of these products.

The continued dominance of pharmacies as a distribution channel is supported by the growth of retail pharmacy chains and the increasing availability of online pharmacy platforms. These channels ensure that both OTC and prescription treatments are readily available to consumers, contributing to the steady growth of the genital warts treatment market.

North America Leads the Genital Warts Treatment Market

North America leads the genital warts treatment market, driven by the high prevalence of HPV infections, strong healthcare infrastructure, and widespread awareness of sexual health. The region's healthcare system offers comprehensive access to both prescription and over-the-counter treatments, supported by insurance coverage that makes treatments more affordable. Moreover, the United States has a high level of education and awareness about sexually transmitted infections, which has led to increased demand for effective genital warts treatments.

The region's robust pharmaceutical industry, coupled with the availability of advanced treatment options such as cryotherapy and laser surgery, further strengthens its position in the global market. North America's leadership in the genital warts treatment market is expected to continue, driven by ongoing innovation, public health initiatives, and the availability of diverse treatment options.

Competitive Landscape and Leading Companies

The genital warts treatment market is competitive, with several key players offering a range of treatments across prescription drugs, over-the-counter products, and surgical procedures. Leading companies in this market include GlaxoSmithKline, Merck & Co., 3M Healthcare, and Bausch Health Companies. These companies are focused on expanding their product offerings, improving treatment efficacy, and increasing access to treatments through various distribution channels.

The competitive landscape is also shaped by ongoing research and development efforts aimed at introducing new, more effective treatments for genital warts. With the growing demand for convenient, non-invasive options, companies are investing in innovative OTC products that allow for easy, at-home treatment. Additionally, advancements in laser surgery and cryotherapy technologies are helping to improve the outcomes of surgical treatments, keeping companies at the forefront of this dynamic market.

Recent Developments:

- In November 2024, Merck & Co. announced the successful results of a clinical trial for a new topical treatment for genital warts.

- In October 2024, GlaxoSmithKline launched a new HPV vaccine to prevent genital warts caused by high-risk strains.

- In September 2024, Bayer AG reported a breakthrough in improving cryotherapy techniques for genital warts treatment, enhancing recovery times.

- In August 2024, Pfizer Inc. partnered with a healthcare provider to improve access to genital wart treatments in underserved regions.

- In July 2024, Astellas Pharma Inc. received approval for a new oral medication aimed at preventing the recurrence of genital warts in patients.

List of Leading Companies:

- Merck & Co., Inc.

- GlaxoSmithKline

- Pfizer Inc.

- Bayer AG

- Mylan N.V.

- Novartis International AG

- Astellas Pharma Inc.

- Teva Pharmaceuticals

- Amgen Inc.

- Sanofi S.A.

- AbbVie Inc.

- Boehringer Ingelheim

- Johnson & Johnson

- Eli Lilly and Company

- Baxter International Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.1 billion |

|

Forecasted Value (2030) |

USD 2.0 billion |

|

CAGR (2024 – 2030) |

9.0% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Genital Warts Treatment Market By Treatment Type (Prescription Drugs, Over-the-Counter Drugs, Surgical Treatments, Other Treatments), By Distribution Channel (Online, Pharmacies, Hospitals and Clinics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Merck & Co., Inc., GlaxoSmithKline, Pfizer Inc., Bayer AG, Mylan N.V., Novartis International AG, Astellas Pharma Inc., Teva Pharmaceuticals, Amgen Inc., Sanofi S.A., AbbVie Inc., Boehringer Ingelheim, Johnson & Johnson, Eli Lilly and Company, Baxter International Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Genital Warts Treatment Market, by Treatment Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Prescription Drugs |

|

4.1.1. Imiquimod |

|

4.1.2. Podophyllotoxin |

|

4.1.3. Others |

|

4.2. Over-the-Counter Drugs |

|

4.2.1. Wart removal creams |

|

4.2.2. Salicylic acid-based products |

|

4.2.3. Others |

|

4.3. Surgical Treatments |

|

4.3.1. Cryotherapy |

|

4.3.2. Electrocautery |

|

4.3.3. Laser surgery |

|

4.4. Other Treatments |

|

5. Genital Warts Treatment Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Online |

|

5.2. Pharmacies |

|

5.3. Hospitals and Clinics |

|

6. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Regional Overview |

|

6.2. North America |

|

6.2.1. Regional Trends & Growth Drivers |

|

6.2.2. Barriers & Challenges |

|

6.2.3. Opportunities |

|

6.2.4. Factor Impact Analysis |

|

6.2.5. Technology Trends |

|

6.2.6. North America Genital Warts Treatment Market, by Treatment Type |

|

6.2.7. North America Genital Warts Treatment Market, by Distribution Channel |

|

6.2.8. By Country |

|

6.2.8.1. US |

|

6.2.8.1.1. US Genital Warts Treatment Market, by Treatment Type |

|

6.2.8.1.2. US Genital Warts Treatment Market, by Distribution Channel |

|

6.2.8.2. Canada |

|

6.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

6.3. Europe |

|

6.4. Asia-Pacific |

|

6.5. Latin America |

|

6.6. Middle East & Africa |

|

7. Competitive Landscape |

|

7.1. Overview of the Key Players |

|

7.2. Competitive Ecosystem |

|

7.2.1. Level of Fragmentation |

|

7.2.2. Market Consolidation |

|

7.2.3. Product Innovation |

|

7.3. Company Share Analysis |

|

7.4. Company Benchmarking Matrix |

|

7.4.1. Strategic Overview |

|

7.4.2. Product Innovations |

|

7.5. Start-up Ecosystem |

|

7.6. Strategic Competitive Insights/ Customer Imperatives |

|

7.7. ESG Matrix/ Sustainability Matrix |

|

7.8. Manufacturing Network |

|

7.8.1. Locations |

|

7.8.2. Supply Chain and Logistics |

|

7.8.3. Product Flexibility/Customization |

|

7.8.4. Digital Transformation and Connectivity |

|

7.8.5. Environmental and Regulatory Compliance |

|

7.9. Technology Readiness Level Matrix |

|

7.10. Technology Maturity Curve |

|

7.11. Buying Criteria |

|

8. Company Profiles |

|

8.1. Merck & Co., Inc. |

|

8.1.1. Company Overview |

|

8.1.2. Company Financials |

|

8.1.3. Product/Service Portfolio |

|

8.1.4. Recent Developments |

|

8.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

8.2. GlaxoSmithKline |

|

8.3. Pfizer Inc. |

|

8.4. Bayer AG |

|

8.5. Mylan N.V. |

|

8.6. Novartis International AG |

|

8.7. Astellas Pharma Inc. |

|

8.8. Teva Pharmaceuticals |

|

8.9. Amgen Inc. |

|

8.10. Sanofi S.A. |

|

8.11. AbbVie Inc. |

|

8.12. Boehringer Ingelheim |

|

8.13. Johnson & Johnson |

|

8.14. Eli Lilly and Company |

|

8.15. Baxter International Inc. |

|

9. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Genital Warts Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Genital Warts Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Genital Warts Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA