As per Intent Market Research, the Emollients Market was valued at USD 09.4 billion and will surpass USD 14.9 billion by 2030; growing at a CAGR of 6.8% during 2024 - 2030.

The emollients market is experiencing substantial growth, driven by increasing demand for personal care and cosmetic products, as well as pharmaceuticals and medical treatments. Emollients are ingredients used in a wide range of products such as skincare lotions, creams, ointments, and cosmetics. These ingredients function by forming a barrier on the skin’s surface, preventing moisture loss and providing hydration, which makes them a critical component in the personal care and healthcare industries. As skin health becomes a top priority for consumers and the demand for multifunctional skincare products rises, the emollients market is expanding rapidly.

Emollients are classified based on their type, source, and application, with each segment offering specific benefits suited to different consumer needs. The rise in awareness of skin conditions such as eczema, psoriasis, and dry skin, combined with the growing trend for natural and plant-based ingredients, is driving the market's expansion. Additionally, the growing demand for anti-aging and moisturizing products has contributed to the adoption of emollients in various skincare applications. This market growth is further fueled by innovations in formulations, including the use of emollients in combination with other active ingredients to enhance the efficacy of skincare, pharmaceutical, and medical products.

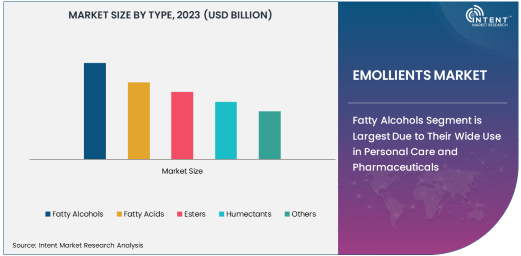

Fatty Alcohols Segment is Largest Due to Their Wide Use in Personal Care and Pharmaceuticals

The fatty alcohols segment holds the largest share in the emollients market, owing to their versatility and broad application across personal care, pharmaceuticals, and healthcare products. Fatty alcohols, such as cetyl alcohol and stearyl alcohol, are used primarily as emulsifying agents, moisturizers, and skin conditioning agents in lotions, creams, shampoos, and other cosmetic formulations. These alcohols are derived from natural fats and oils, making them an ideal choice for consumers looking for ingredients with a more natural or plant-based origin.

The large adoption of fatty alcohols in personal care & cosmetics is a key factor driving the segment's dominance. They are commonly used in moisturizers, body lotions, and hair care products due to their ability to improve texture, enhance skin hydration, and increase the stability of emulsions. Fatty alcohols also play a vital role in the pharmaceutical industry, where they are included in topical formulations for their soothing properties and ability to aid the absorption of active ingredients through the skin. Given the increasing demand for skin care products that provide long-lasting hydration and skin barrier protection, fatty alcohols are expected to continue their dominance in the market, particularly in the personal care and pharmaceutical applications.

Plant-based Source Segment Grows Rapidly Due to Consumer Preference for Natural Ingredients

The plant-based source segment is experiencing rapid growth, driven by the increasing preference for natural and sustainable ingredients in personal care and pharmaceutical products. Plant-based emollients, derived from sources such as coconut oil, shea butter, and olive oil, are gaining popularity as consumers become more conscious of the environmental impact of synthetic chemicals and seek more eco-friendly and cruelty-free products. These plant-based ingredients are often perceived as safer and gentler on the skin, making them particularly appealing in products for sensitive skin or dermatological treatments.

Plant-based emollients are not only used in personal care & cosmetics but are also becoming more prevalent in pharmaceuticals and medical & dermatological treatments. With growing awareness of the benefits of natural skincare and the increasing number of people looking for hypoallergenic and non-toxic products, the demand for plant-based emollients is expected to rise. The natural ingredients used in these emollients provide essential fatty acids, antioxidants, and vitamins that nourish and protect the skin, contributing to the segment's rapid growth. As the demand for plant-based products continues to rise, the plant-based emollient segment is expected to be one of the fastest-growing in the market.

Cosmetics & Skincare End-User Industry Drives the Demand for Emollients

The cosmetics & skincare industry is the largest end-user of emollients, accounting for a significant share of the market. The rising demand for skin moisturizers, anti-aging creams, sunscreens, and other skincare products has created a strong need for emollients that improve the texture, feel, and hydration of products. Emollients play a crucial role in enhancing the skin’s appearance, providing smoothness, and reducing the effects of aging by preventing moisture loss and improving skin elasticity. They are widely used in facial care products, body creams, lip balms, and hair care products to restore and maintain skin moisture, which is essential for healthy skin.

The growth of the cosmetics & skincare industry is driven by consumers' increasing focus on self-care and the desire for products that promote healthy, youthful skin. Emollients that offer additional benefits, such as soothing properties or protection from environmental factors, are gaining traction in the market. The rise in popularity of clean beauty products and natural ingredients further boosts the demand for emollients, especially those derived from plant-based sources. As the skincare industry continues to expand and evolve, emollients will remain a core ingredient in skincare formulations, driving market growth in the coming years.

Asia Pacific Region Leads the Emollients Market Due to Growing Consumer Demand for Personal Care Products

The Asia Pacific region is the largest and fastest-growing market for emollients, driven by increasing consumer demand for personal care products, rising awareness of skincare, and growing disposable incomes. Countries such as China, India, Japan, and South Korea are witnessing significant growth in the personal care and cosmetics sectors, with consumers increasingly seeking high-quality skincare products. The rapid urbanization and changing lifestyles in these countries have contributed to higher consumer spending on personal care and health-related products.

The region's strong manufacturing base for cosmetics and skincare products, coupled with the rising popularity of natural and organic beauty products, has further contributed to the demand for plant-based emollients. Additionally, the growing prevalence of skin conditions such as eczema and acne in Asia Pacific has led to an increased demand for pharmaceutical products that incorporate emollients for skin relief. The region's increasing emphasis on beauty standards, coupled with the rise in disposable income and the expanding middle class, is expected to drive the emollients market in Asia Pacific, making it the dominant region in the global market.

Competitive Landscape and Leading Companies

The competitive landscape of the emollients market is highly dynamic, with several global and regional players competing for market share. Leading companies in the market include BASF SE, Evonik Industries AG, Croda International Plc, Lonza Group, and Clariant AG. These companies have established themselves as key players in the emollients market through strategic product innovations, mergers and acquisitions, and a strong focus on sustainable and natural ingredients. To stay competitive, these companies are investing in the development of new emollient formulations that meet the growing consumer demand for safe, effective, and eco-friendly products.

In addition to large multinational companies, numerous regional players also dominate the market by catering to local demands for specific types of emollients. Many companies are focusing on research and development to introduce innovative emollient solutions that offer superior moisturizing, anti-aging, and skin-soothing properties. With the increasing trend of natural and plant-based ingredients, many players are diversifying their portfolios by incorporating organic and sustainable emollients into their product lines. The competitive environment is also characterized by strong distribution networks, with companies leveraging online retail, third-party distributors, and direct sales channels to expand their reach in key markets.

Recent Developments:

- BASF SE introduced a new range of plant-based emollients aimed at enhancing skin hydration and offering natural alternatives in personal care formulations.

- Evonik Industries expanded its production capabilities for emollients used in medical and dermatological applications, focusing on treating sensitive skin conditions.

- Croda International Plc launched a new line of biodegradable emollients designed for sustainable skincare formulations in line with growing consumer demand for eco-friendly products.

- The Dow Chemical Company developed an advanced emollient compound for use in high-performance moisturizers and anti-aging skincare treatments.

- Ashland Global Holdings Inc. entered into a strategic partnership with a pharmaceutical company to supply emollients for topical treatments, focusing on improving skin barrier repair.

List of Leading Companies:

- BASF SE

- Evonik Industries

- Croda International Plc

- The Dow Chemical Company

- Ashland Global Holdings Inc.

- Lonza Group

- Innospec Inc.

- Clariant International Ltd.

- Stepan Company

- AkzoNobel N.V.

- Solvay S.A.

- Kao Corporation

- Godrej Industries Ltd.

- Sabinsa Corporation

- Galaxy Surfactants Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 9.4 billion |

|

Forecasted Value (2030) |

USD 14.9 billion |

|

CAGR (2024 – 2030) |

6.8% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Emollients Market By Type (Fatty Alcohols, Fatty Acids, Esters, Humectants), By Source (Plant-based, Animal-based, Synthetic), By Application (Personal Care & Cosmetics, Pharmaceuticals, Medical & Dermatological Treatments, Industrial), By End-Use Industry (Cosmetics & Skincare, Pharmaceuticals, Healthcare, Personal Care), and By Distribution Channel (Direct Sales, Third-Party Distributors, Online Retail) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

BASF SE, Evonik Industries, Croda International Plc, The Dow Chemical Company, Ashland Global Holdings Inc., Lonza Group, Innospec Inc., Clariant International Ltd., Stepan Company, AkzoNobel N.V., Solvay S.A., Kao Corporation, Godrej Industries Ltd., Sabinsa Corporation, Galaxy Surfactants Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Emollients Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Fatty Alcohols |

|

4.2. Fatty Acids |

|

4.3. Esters |

|

4.4. Humectants |

|

4.5. Others |

|

5. Emollients Market, by Source (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Plant-based |

|

5.2. Animal-based |

|

5.3. Synthetic |

|

6. Emollients Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Personal Care & Cosmetics |

|

6.2. Pharmaceuticals |

|

6.3. Medical & Dermatological Treatments |

|

6.4. Industrial |

|

7. Emollients Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Cosmetics & Skincare |

|

7.2. Pharmaceuticals |

|

7.3. Healthcare |

|

7.4. Personal Care |

|

8. Emollients Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Direct Sales |

|

8.2. Third-Party Distributors |

|

8.3. Online Retail |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Emollients Market, by Type |

|

9.2.7. North America Emollients Market, by Source |

|

9.2.8. North America Emollients Market, by Application |

|

9.2.9. North America Emollients Market, by End-User Industry |

|

9.2.10. North America Emollients Market, by Distribution Channel |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Emollients Market, by Type |

|

9.2.11.1.2. US Emollients Market, by Source |

|

9.2.11.1.3. US Emollients Market, by Application |

|

9.2.11.1.4. US Emollients Market, by End-User Industry |

|

9.2.11.1.5. US Emollients Market, by Distribution Channel |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. BASF SE |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Evonik Industries |

|

11.3. Croda International Plc |

|

11.4. The Dow Chemical Company |

|

11.5. Ashland Global Holdings Inc. |

|

11.6. Lonza Group |

|

11.7. Innospec Inc. |

|

11.8. Clariant International Ltd. |

|

11.9. Stepan Company |

|

11.10. AkzoNobel N.V. |

|

11.11. Solvay S.A. |

|

11.12. Kao Corporation |

|

11.13. Godrej Industries Ltd. |

|

11.14. Sabinsa Corporation |

|

11.15. Galaxy Surfactants Ltd. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Emollients Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Emollients Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Emollients Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA