As per Intent Market Research, the Elevator Components Market was valued at USD 20.7 billion in 2024-e and will surpass USD 33.3 billion by 2030; growing at a CAGR of 8.2% during 2024 - 2030.

The global elevator components market is witnessing significant growth, driven by increasing urbanization, the expansion of commercial and residential infrastructure, and the rising demand for advanced mobility solutions in high-rise buildings. Elevator systems are essential for the vertical transportation of people and goods, particularly in densely populated urban areas. As the need for efficient and reliable elevator systems grows, so does the demand for high-quality elevator components. The market for these components encompasses various elements, such as traction machines, hydraulic systems, control systems, doors and door operators, safety components, cabins, and ropes and cables, all playing vital roles in ensuring the optimal functioning of elevators.

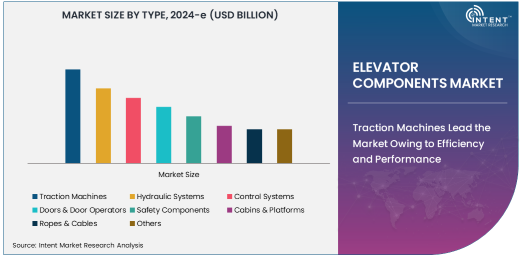

Among these various components, traction machines are emerging as a key subsegment, largely due to their growing demand in modern elevator designs, particularly in high-rise and commercial buildings. Traction machines offer significant advantages over traditional hydraulic systems, including higher energy efficiency, smoother operation, and reduced maintenance costs. As a result, they are becoming increasingly preferred for elevator systems that require high performance and energy efficiency, driving the growth of the traction machines subsegment in the elevator components market.

Traction Machines Lead the Market Owing to Efficiency and Performance

Traction machines are expected to dominate the elevator components market, owing to their critical role in the operation of modern elevators, particularly in high-rise buildings. These machines use a system of pulleys, ropes, and counterweights to lift and lower elevator cabins, providing a more energy-efficient and smooth ride compared to hydraulic systems. As commercial and residential buildings continue to rise in height, the demand for traction-based elevator systems is also on the rise. Traction elevators are known for their speed, reliability, and energy efficiency, making them a preferred choice in urban areas, where space and energy optimization are crucial.

The growth of urbanization, especially in emerging economies, is further fueling the demand for traction machines. These systems not only provide superior operational performance but also contribute to the overall sustainability of building operations by minimizing energy consumption. With a growing focus on green building initiatives and the need for cost-effective solutions, traction machines are poised to maintain their leadership in the market. Additionally, the rise of smart buildings with integrated technologies that require precise control over elevator operations is also contributing to the increasing adoption of traction elevators.

Safety Components Continue to Evolve, Offering Enhanced Protection

Safety components represent another significant subsegment of the elevator components market. These components, including safety brakes, overspeed governors, and emergency communication systems, play a crucial role in ensuring the safety of passengers and goods during elevator operation. The growing emphasis on safety regulations, especially in commercial and residential infrastructure, is driving the demand for advanced safety systems. With increasing awareness about building safety and a rise in regulatory standards across various regions, the demand for innovative safety components is higher than ever.

The integration of advanced technologies in safety components, such as digital sensors and IoT (Internet of Things) connectivity, is further enhancing their effectiveness. These technologies allow for real-time monitoring of elevator systems and enable predictive maintenance, reducing the risk of failures and accidents. As elevators become more sophisticated and are expected to serve a larger volume of passengers, the need for highly reliable safety components will continue to rise, positioning this segment for steady growth in the coming years.

Commercial Application Leads the Elevator Components Market

The commercial application of elevator components is the largest segment in the market, driven by the increasing construction of high-rise office buildings, shopping malls, and hotels. Commercial properties typically require advanced and efficient elevator systems to ensure smooth vertical transportation for large volumes of people, especially in skyscrapers. Traction machines, control systems, and doors & door operators are the primary components in commercial elevators, contributing to enhanced operational performance and passenger convenience.

With the rise of urbanization and a shift toward modern office spaces, demand for commercial elevator systems continues to grow. The demand for high-speed elevators that provide energy efficiency, reliability, and safety is expected to remain strong as more cities experience vertical growth. Additionally, the growing preference for smart elevators that provide features such as touchless controls and automated scheduling further boosts the commercial segment, particularly in regions with strong real estate development.

OEM Segment Dominates the Elevator Components Market

The OEM (Original Equipment Manufacturer) segment is the largest end-user segment in the elevator components market. Elevator OEMs are responsible for manufacturing and assembling elevator systems for new buildings, and as a result, they are the primary consumers of elevator components. The increasing demand for high-performance and energy-efficient elevator systems in both residential and commercial buildings is contributing to the growth of the OEM segment. OEMs are continuously looking for advanced, reliable, and cost-effective components to meet the evolving needs of the market.

As new construction projects continue to rise in urban areas, particularly in emerging economies, the OEM segment is expected to maintain its dominant position. Manufacturers are focused on improving the quality and functionality of their elevator components to offer competitive solutions that meet regulatory standards and customer demands. The integration of automation and smart technologies into elevator systems is also driving innovation in the OEM segment, further contributing to its dominance in the market.

Asia Pacific to See Significant Growth in Elevator Components Market

The Asia Pacific region is expected to witness substantial growth in the elevator components market. The rapid urbanization, particularly in countries such as China, India, and Japan, is driving the demand for advanced elevator systems in residential, commercial, and industrial buildings. The region’s large construction sector, with numerous high-rise building projects, is boosting the demand for efficient elevator systems and components.

As the demand for energy-efficient and high-performance elevators continues to rise in the region, key players are focusing on expanding their manufacturing and distribution capabilities in Asia Pacific. The growing middle-class population and rising disposable income are also contributing to the increased construction of residential and commercial buildings, further driving the demand for elevator systems. The need for modernization in older buildings is also contributing to the growth of the elevator components market in this region.

Competitive Landscape: Key Players and Strategic Initiatives

The elevator components market is highly competitive, with several global and regional players competing for market share. Leading companies in the market include KONE Corporation, Thyssenkrupp AG, Schindler Group, Otis Elevator Company, and Mitsubishi Electric Corporation. These companies focus on product innovation, strategic partnerships, and expanding their geographical presence to strengthen their position in the market.

In addition to traditional players, several new entrants are focusing on developing technologically advanced elevator components to meet the growing demand for smart, energy-efficient, and safe elevator systems. The competitive landscape is characterized by investments in R&D to enhance product offerings and the integration of automation and IoT technologies into elevator systems. Companies are also focusing on expanding their service portfolios to include maintenance, repair, and modernization services, thereby ensuring a steady revenue stream. As the market evolves, leading players are expected to continue focusing on providing innovative and sustainable solutions to meet the evolving needs of the global elevator industry.

Recent Developments:

- Otis Worldwide Corporation unveiled a new, energy-efficient elevator system designed to reduce operational costs in commercial buildings.

- Kone Corporation launched a new elevator control system aimed at improving elevator efficiency and reducing waiting times.

- Mitsubishi Electric Corporation introduced a new safety feature in its elevator components to enhance user protection in emergency situations.

- Thyssenkrupp AG expanded its elevator components portfolio with a new line of eco-friendly hydraulic systems.

- Schindler Group announced the introduction of a predictive maintenance solution that leverages IoT technology to reduce downtime and improve elevator performance.

List of Leading Companies:

- Thyssenkrupp AG

- Schindler Group

- Otis Worldwide Corporation

- Kone Corporation

- Mitsubishi Electric Corporation

- Hitachi Ltd.

- Fujitec Co., Ltd.

- Hyundai Elevator Co., Ltd.

- Toshiba Corporation

- Johnson Lifts Pvt. Ltd.

- Hyundai Elevator Co., Ltd.

- Omega Elevators Pvt. Ltd.

- ZIEHL-ABEGG International GmbH

- Wittur Group

- Eleiko Group

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 20.7 billion |

|

Forecasted Value (2030) |

USD 33.3 billion |

|

CAGR (2025 – 2030) |

8.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Elevator Components Market By Type (Traction Machines, Hydraulic Systems, Control Systems, Doors & Door Operators, Safety Components, Cabins & Platforms, Ropes & Cables), By Application (Residential, Commercial, Industrial, Institutional), By End-User (OEM (Original Equipment Manufacturers), Aftermarket) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Thyssenkrupp AG, Schindler Group, Otis Worldwide Corporation, Kone Corporation, Mitsubishi Electric Corporation, Hitachi Ltd., Fujitec Co., Ltd., Hyundai Elevator Co., Ltd., Toshiba Corporation, Johnson Lifts Pvt. Ltd., Hyundai Elevator Co., Ltd., Omega Elevators Pvt. Ltd., ZIEHL-ABEGG International GmbH, Wittur Group, Eleiko Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Elevator Components Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Traction Machines |

|

4.2. Hydraulic Systems |

|

4.3. Control Systems |

|

4.4. Doors & Door Operators |

|

4.5. Safety Components |

|

4.6. Cabins & Platforms |

|

4.7. Ropes & Cables |

|

4.8. Others |

|

5. Elevator Components Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Residential |

|

5.2. Commercial |

|

5.3. Industrial |

|

5.4. Institutional |

|

5.5. Others |

|

6. Elevator Components Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. OEM (Original Equipment Manufacturers) |

|

6.2. Aftermarket |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Elevator Components Market, by Type |

|

7.2.7. North America Elevator Components Market, by Application |

|

7.2.8. North America Elevator Components Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Elevator Components Market, by Type |

|

7.2.9.1.2. US Elevator Components Market, by Application |

|

7.2.9.1.3. US Elevator Components Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Thyssenkrupp AG |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Schindler Group |

|

9.3. Otis Worldwide Corporation |

|

9.4. Kone Corporation |

|

9.5. Mitsubishi Electric Corporation |

|

9.6. Hitachi Ltd. |

|

9.7. Fujitec Co., Ltd. |

|

9.8. Hyundai Elevator Co., Ltd. |

|

9.9. Toshiba Corporation |

|

9.10. Johnson Lifts Pvt. Ltd. |

|

9.11. Hyundai Elevator Co., Ltd. |

|

9.12. Omega Elevators Pvt. Ltd. |

|

9.13. ZIEHL-ABEGG International GmbH |

|

9.14. Wittur Group |

|

9.15. Eleiko Group |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Elevator Components Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Elevator Components Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Elevator Components Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA