As per Intent Market Research, the Dual Clutch Transmission Market was valued at USD 15.7 billion in 2023 and will surpass USD 37.8 billion by 2030; growing at a CAGR of 13.3% during 2024 - 2030.

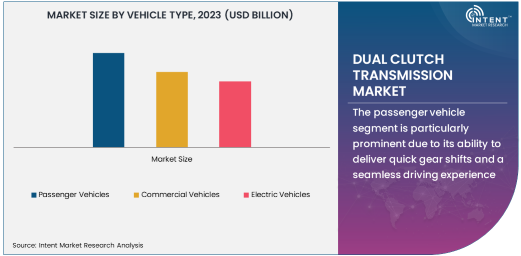

The vehicle type segment in the dual-clutch transmission (DCT) market is diverse, with several categories contributing to its growth. Among these, passenger vehicles dominate the market, driven by the increasing consumer demand for higher performance, better fuel efficiency, and smooth driving experiences. Passenger vehicles are the largest segment, benefiting from the popularity of DCTs in sedans, hatchbacks, and sports cars, where performance and comfort are crucial. The growing automotive industry, especially in emerging economies, is boosting demand for passenger vehicles equipped with dual-clutch transmissions.

The passenger vehicle segment is particularly prominent due to its ability to deliver quick gear shifts and a seamless driving experience, making it highly preferred in mid-to-high-end vehicle models. As consumers continue to prioritize convenience and fuel efficiency, DCT technology has become increasingly essential in mainstream vehicles. Additionally, stringent regulations related to fuel efficiency and emissions have led manufacturers to adopt advanced transmission systems like DCT to meet environmental standards, further accelerating its adoption in passenger vehicles.

Wet Dual Clutch Transmission Segment Is Fastest Growing Due to Performance Benefits

The transmission type segment is experiencing significant advancements, with wet dual-clutch transmissions (DCT) showing the fastest growth. Wet DCTs are preferred for their ability to handle higher torque loads and provide enhanced durability, making them ideal for performance-oriented and heavy-duty applications. The growth in the performance automotive market and the demand for sports cars, luxury sedans, and high-performance vehicles are major drivers for the increasing adoption of wet DCTs. These transmissions offer smoother gear shifts, improved fuel efficiency, and enhanced overall driving experience, which makes them highly suitable for performance and luxury vehicles.

The technology behind wet DCTs, which utilizes a lubrication system for the clutches, provides significant advantages in terms of cooling and extended transmission life. As automakers strive to meet consumer demands for high-performance vehicles, wet DCTs are becoming the preferred choice. Additionally, wet DCTs are also gaining traction in commercial and industrial applications where power and durability are essential. The automotive industry's increasing focus on enhancing vehicle performance and efficiency ensures that wet dual-clutch transmissions will continue to dominate the market in the coming years.

Automotive Application Is Largest Driven by Global Demand for Vehicles

In the application segment, the automotive sector is the largest and most established market for dual-clutch transmissions. As the demand for passenger and commercial vehicles continues to rise globally, automotive manufacturers are increasingly adopting DCT systems for their advantages in fuel efficiency, smoother shifting, and superior performance. The automotive application segment is at the forefront due to the need for advanced transmission systems in modern vehicles, including sedans, SUVs, and performance-oriented models. With vehicle sales reaching new heights, particularly in regions like North America and Europe, the demand for DCT-equipped cars is growing steadily.

Automotive manufacturers are adopting dual-clutch transmissions in response to both consumer preference for smoother, more efficient driving experiences and regulatory pressures for improved fuel efficiency. The widespread adoption of DCT in mid- to high-end models, especially in premium brands like Audi, Volkswagen, and BMW, has cemented automotive as the largest and most influential application segment in the DCT market. As the demand for advanced automotive technology continues to rise, the adoption of dual-clutch systems in vehicles is expected to remain a significant trend.

Dual Clutch Automatic Transmission Technology Is Leading the Market

Among various transmission technologies, dual-clutch automatic transmission (DCT) is gaining significant momentum and is leading the market due to its ability to offer a seamless and high-performance driving experience. DCT technology offers quicker shifts compared to traditional automatic transmissions, with little to no power loss between gears. This makes it particularly desirable in high-performance vehicles and sports cars, where precise gear changes and efficiency are essential. The fast-shifting capability of DCT technology also enhances the overall fuel efficiency and performance of vehicles, making it the technology of choice for automotive manufacturers focused on providing cutting-edge driving experiences.

In addition to the automotive sector, DCT technology is being integrated into electric and hybrid vehicles, further driving its growth. As automakers move towards more eco-friendly solutions while maintaining performance standards, dual-clutch automatic transmissions offer a balance between fuel economy and driving dynamics. The widespread adoption of DCT systems by automakers for both mainstream and high-end models underscores the growing importance of this technology in the global automotive landscape.

Asia Pacific Region Is Fastest Growing Due to Increasing Vehicle Production

The Asia Pacific region is experiencing the fastest growth in the dual-clutch transmission market, driven by the rapid increase in vehicle production and the growing demand for advanced automotive technologies in countries like China, Japan, and South Korea. The rise in disposable income, urbanization, and the growing number of vehicle owners are fueling the demand for both passenger and commercial vehicles equipped with dual-clutch transmissions. Moreover, Asia Pacific is home to several key automotive manufacturing hubs, including China, which is the world's largest car market, and Japan, known for its high-tech automotive solutions.

Additionally, the region’s competitive landscape, marked by the presence of major automotive companies like Toyota, Honda, and Hyundai, is further propelling the adoption of DCTs. The push for fuel-efficient, high-performance vehicles, along with government initiatives aimed at reducing emissions, is significantly boosting the adoption of dual-clutch transmissions in the region. As the automotive industry in Asia continues to expand, the dual-clutch transmission market is poised to benefit from increasing demand and technological advancements.

Leading Companies and Competitive Landscape in the DCT Market

The dual-clutch transmission market is highly competitive, with key players focusing on technological innovation, strategic partnerships, and regional expansion. Leading companies such as ZF Friedrichshafen AG, BorgWarner, Aisin Seiki, and Jatco are at the forefront of the market. These companies have a strong global presence and continuously invest in R&D to enhance the performance and efficiency of their DCT products. ZF Friedrichshafen and BorgWarner, in particular, have been pioneers in the development of both wet and dry dual-clutch transmission systems, catering to a wide range of automotive applications.

The competitive landscape is also influenced by mergers and acquisitions (M&A) activity, as companies strive to expand their portfolios and gain a larger share of the growing market. For example, BorgWarner's acquisition of Akasol was aimed at expanding its electric vehicle portfolio, signaling the growing importance of DCT in the electrification of the automotive industry. Additionally, collaborations between automakers and suppliers to create custom DCT solutions for specific vehicle models are becoming increasingly common. As the demand for more efficient, high-performance vehicles grows, these leading companies are well-positioned to dominate the market with innovative dual-clutch transmission technologies.

Recent Developments:

- ZF has unveiled a next-gen DCT for electric vehicles, offering higher torque and better efficiency for future automotive designs.

- BorgWarner has acquired Akasol to expand its electric vehicle transmission offerings and strengthen its position in the electric vehicle market.

- Aisin Seiki has launched a new 8-speed dual clutch transmission designed to improve fuel efficiency and performance in heavy-duty commercial vehicles.

- Allison Transmission has announced a new range of DCTs designed for electric vehicles, focusing on reducing weight and improving efficiency.

- Continental has expanded its manufacturing capacity for DCT systems in Asia, in response to growing demand from global automakers for high-performance transmission solutions.

List of Leading Companies:

- ZF Friedrichshafen AG

- BorgWarner Inc.

- Aisin Seiki Co., Ltd.

- Continental AG

- Getrag (Magna Powertrain)

- Jatco Ltd.

- Hyundai Transys Inc.

- Honda Motor Co., Ltd.

- Toyota Motor Corporation

- Daimler AG

- Schaeffler Group

- Valeo SA

- Allison Transmission Inc.

- Eaton Corporation

- Volkswagen AG

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 15.7Billion |

|

Forecasted Value (2030) |

USD 37.8 Billion |

|

CAGR (2024 – 2030) |

13.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Dual Clutch Transmission Market By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), By Transmission Type (Wet Dual Clutch Transmission, Dry Dual Clutch Transmission), By Application (Automotive, Motorcycles, Industrial Vehicles), By Technology (Automated Manual Transmission, Dual Clutch Automatic Transmission) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ZF Friedrichshafen AG, BorgWarner Inc., Aisin Seiki Co., Ltd., Continental AG, Getrag (Magna Powertrain), Jatco Ltd., Hyundai Transys Inc., Honda Motor Co., Ltd., Toyota Motor Corporation, Daimler AG, Schaeffler Group, Valeo SA, Allison Transmission Inc., Eaton Corporation, Volkswagen AG |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Dual Clutch Transmission Market, by Vehicle Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Passenger Vehicles |

|

4.2. Commercial Vehicles |

|

4.3. Electric Vehicles |

|

5. Dual Clutch Transmission Market, by Transmission Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Wet Dual Clutch Transmission |

|

5.2. Dry Dual Clutch Transmission |

|

6. Dual Clutch Transmission Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Automotive |

|

6.2. Motorcycles |

|

6.3. Industrial Vehicles |

|

7. Dual Clutch Transmission Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Automated Manual Transmission (AMT) |

|

7.2. Dual Clutch Automatic Transmission (DCT) |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Dual Clutch Transmission Market, by Vehicle Type |

|

8.2.7. North America Dual Clutch Transmission Market, by Transmission Type |

|

8.2.8. North America Dual Clutch Transmission Market, by Application |

|

8.2.9. North America Dual Clutch Transmission Market, by Technology |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Dual Clutch Transmission Market, by Vehicle Type |

|

8.2.10.1.2. US Dual Clutch Transmission Market, by Transmission Type |

|

8.2.10.1.3. US Dual Clutch Transmission Market, by Application |

|

8.2.10.1.4. US Dual Clutch Transmission Market, by Technology |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. ZF Friedrichshafen AG |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. BorgWarner Inc. |

|

10.3. Aisin Seiki Co., Ltd. |

|

10.4. Continental AG |

|

10.5. Getrag (Magna Powertrain) |

|

10.6. Jatco Ltd. |

|

10.7. Hyundai Transys Inc. |

|

10.8. Honda Motor Co., Ltd. |

|

10.9. Toyota Motor Corporation |

|

10.10. Daimler AG |

|

10.11. Schaeffler Group |

|

10.12. Valeo SA |

|

10.13. Allison Transmission Inc. |

|

10.14. Eaton Corporation |

|

10.15. Volkswagen AG |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Dual Clutch Transmission Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Dual Clutch Transmission Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Dual Clutch Transmission Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA