As per Intent Market Research, the Drone In A Box Market was valued at USD 3.7 billion in 2023 and will surpass USD 14.2 billion by 2030; growing at a CAGR of 21.2% during 2024 - 2030.

The Drone in a Box (DIB) market is witnessing substantial growth driven by advancements in autonomous drone technology and the increasing demand for efficient, cost-effective solutions across various industries. A Drone in a Box system consists of a drone paired with its supporting infrastructure, including charging stations and software, allowing for autonomous operation, data collection, and even delivery services. This technology is poised to revolutionize applications in industries such as logistics, agriculture, energy, defense, and environmental monitoring. The convenience and automation provided by DIB systems make them highly attractive for applications that require continuous monitoring and remote operations.

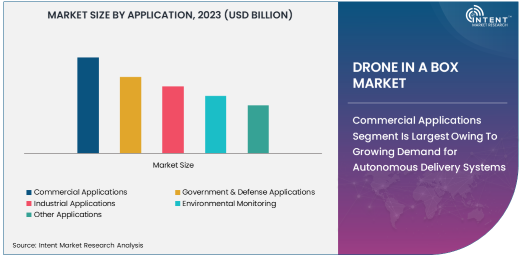

Commercial Applications Segment Is Largest Owing To Growing Demand for Autonomous Delivery Systems

The commercial applications segment of the Drone in a Box market holds the largest share. This can be attributed to the increasing use of autonomous drones for last-mile delivery in logistics and e-commerce sectors. DIB systems are ideal for remote, quick deliveries of packages, especially in urban areas, as they are capable of launching, recharging, and landing autonomously, without the need for human intervention. The widespread adoption of drones by logistics companies to improve efficiency, reduce delivery costs, and expand reach in both urban and rural areas has made commercial applications the key driver of the market.

With advancements in autonomous delivery systems, companies like Amazon and UPS have already begun deploying drones for parcel deliveries. The ability of drones to operate without human oversight ensures faster, safer, and more cost-efficient logistics operations. Furthermore, the deployment of drone fleets integrated with DIB systems enables real-time package tracking and rapid deliveries, further fueling the demand for drone technology in commercial applications.

Fully Autonomous Systems Segment Is Fastest Growing Owing To Advancements in AI and Machine Learning

The fully autonomous systems segment is the fastest-growing category within the Drone in a Box market. These systems are designed to operate without human input, relying on AI, machine learning, and sensors for navigation, decision-making, and task execution. With the growing demand for automation in sectors such as logistics, agriculture, and infrastructure monitoring, fully autonomous drones have become increasingly popular as they offer 24/7 operations with minimal human oversight.

The rapid development of AI and machine learning technologies has enabled these drones to perform complex tasks such as real-time obstacle avoidance, precise navigation in crowded environments, and autonomous route planning. As fully autonomous systems continue to evolve, they are expected to gain even more traction in industries looking to enhance operational efficiency and reduce labor costs, thus propelling market growth.

Logistics & Delivery Segment Is Largest Owing To E-commerce Boom

Among the various end-user industries, the logistics and delivery segment dominates the Drone in a Box market. The growing demand for faster deliveries, particularly in the wake of the e-commerce boom, has created a significant opportunity for drone solutions. Logistics companies are increasingly investing in autonomous drones integrated with DIB systems to enhance their last-mile delivery capabilities. These drones can transport goods efficiently over short distances, bypassing ground traffic and reducing delivery times.

E-commerce giants such as Amazon and Alibaba are leading the way by testing and deploying drone fleets to deliver parcels swiftly and cost-effectively. The convenience of drone deliveries also aligns with consumer expectations for faster shipping and real-time tracking, making logistics and delivery the largest end-user industry for drone-in-a-box systems.

Charging Stations Segment Is Largest Owing To Integral Role in Drone Operations

In terms of components, charging stations make up the largest share of the Drone in a Box market. These stations are essential for maintaining the continuous operation of autonomous drones, particularly in remote areas or for operations requiring long durations. As DIB systems are designed for autonomous flight, they rely on charging stations to ensure the drones are powered up and ready to be deployed at any time. These stations can automatically recharge drones, ensuring minimal downtime and increased operational efficiency.

The growth of charging station infrastructure is directly linked to the expanding use of drones across various industries. In addition to supporting drones in delivery, agriculture, and infrastructure monitoring, charging stations are integral for maintaining the scalability of drone fleets. As more businesses embrace drone technology, the demand for reliable, fast-charging stations continues to rise.

Ground-Based Systems Deployment Segment Is Largest Owing To Infrastructure Support

Among the various deployment types, ground-based systems are the largest due to their robust infrastructure and ease of maintenance. Ground-based DIB systems offer a secure, easily monitored environment for charging and storing drones between operations. These systems are commonly used in industries such as agriculture, logistics, and environmental monitoring, where drones are frequently deployed for repetitive tasks such as surveillance, crop monitoring, or deliveries.

While airborne and hybrid systems also have their place, ground-based systems are the most cost-effective and practical solution for most applications. Their ability to provide continuous, autonomous operations makes them ideal for large-scale deployment in industries requiring consistent monitoring and long-duration tasks.

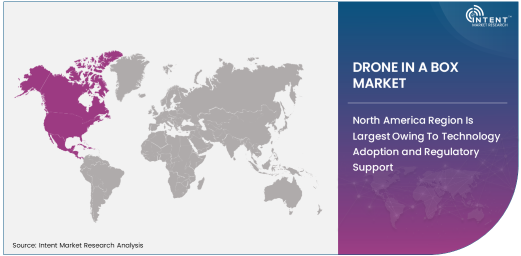

North America Region Is Largest Owing To Technology Adoption and Regulatory Support

The North American region is the largest market for Drone in a Box systems, driven by the region’s advanced technological infrastructure, strong regulatory framework, and high adoption of drone technologies across industries. The United States, in particular, is at the forefront of drone innovations, with companies such as Amazon, UPS, and Alphabet investing heavily in drone technology for logistics and delivery applications. Moreover, North America has some of the most supportive regulatory environments, with government agencies like the FAA (Federal Aviation Administration) implementing clear regulations for drone operations, enabling faster market growth.

The region is also home to several key players in the drone technology space, further supporting its dominance. As demand for autonomous delivery and industrial drone services increases, North America is expected to maintain its leadership position in the Drone in a Box market.

Leading Companies and Competitive Landscape

The Drone in a Box market is highly competitive, with several key players actively innovating and expanding their portfolios. Leading companies such as Percepto, Skycatch, Airobotics, DJI, and Kespry are at the forefront of market development. These companies are continuously improving their autonomous drone capabilities and introducing new features, such as better battery life, AI-powered navigation, and enhanced sensors for more accurate data collection.

Competition is also intensifying as companies look to differentiate their products through the introduction of advanced software, data analytics platforms, and integrated charging systems. Partnerships between drone manufacturers and end-users across industries like agriculture, logistics, and defense are expected to drive future market growth. As the market evolves, the demand for comprehensive solutions that combine drones, charging stations, and software platforms will continue to shape the competitive landscape, pushing innovation in autonomous systems.

Recent Developments:

- Percepto recently launched its upgraded Percepto Sparrow, a fully autonomous drone solution with enhanced AI capabilities for industrial inspection and surveillance applications.

- Airobotics signed a partnership with ABB to integrate its autonomous drone solutions with ABB’s industrial automation systems, providing a smarter approach to industrial inspection.

- DJI Innovations unveiled a new drone-in-a-box system designed for industrial and agricultural monitoring, offering automated, end-to-end data collection solutions.

- Ehang received regulatory approval from the Civil Aviation Administration of China (CAAC) for its Ehang 216 drone to operate in urban air mobility networks, enhancing the commercial viability of its drones-in-a-box systems.

- Kespry was acquired by Verisk Analytics, strengthening its position in the commercial drone industry and advancing their autonomous drone solutions for aerial surveying and mapping applications.

List of Leading Companies:

- Percepto

- Skycatch

- Airobotics

- ABB

- Intel Corporation

- DJI Innovations

- Autel Robotics

- Flytrex

- PrecisionHawk

- Aerospace Technologies

- Ehang

- Airbus

- Lockheed Martin

- Parrot

- Kespry

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.7 Billion |

|

Forecasted Value (2030) |

USD 14.2 Billion |

|

CAGR (2024 – 2030) |

21.2% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Drone in a Box Market By Application (Commercial Applications, Government & Defense Applications, Industrial Applications, Environmental Monitoring), By Type (Fully Autonomous Systems, Semi-Autonomous Systems, Manual Systems), By End-User Industry (Agriculture, Logistics & Delivery, Military & Defense, Energy & Utilities), By Component (Drones, Charging Stations, Software, Sensors, Communication Systems), and By Deployment (Ground-Based Systems, Airborne Systems, Hybrid Systems) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Percepto, Skycatch, Airobotics, ABB, Intel Corporation, DJI Innovations, Autel Robotics, Flytrex, PrecisionHawk, Aerospace Technologies, Ehang, Airbus, Lockheed Martin, Parrot, Kespry |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Drone In A Box Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Commercial Applications |

|

4.2. Government & Defense Applications |

|

4.3. Industrial Applications |

|

4.4. Environmental Monitoring |

|

4.5. Others |

|

5. Drone In A Box Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Fully Autonomous Systems |

|

5.2. Semi-Autonomous Systems |

|

5.3. Manual Systems |

|

6. Drone In A Box Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Agriculture |

|

6.2. Logistics & Delivery |

|

6.3. Military & Defense |

|

6.4. Energy & Utilities |

|

6.5. Other Industries |

|

7. Drone In A Box Market, by Component (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Drones |

|

7.2. Charging Stations |

|

7.3. Software |

|

7.4. Sensors |

|

7.5. Communication Systems |

|

7.6. Other Components |

|

8. Drone In A Box Market, by Deployment (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Ground-Based Systems |

|

8.2. Airborne Systems |

|

8.3. Hybrid Systems |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Drone In A Box Market, by Application |

|

9.2.7. North America Drone In A Box Market, by Type |

|

9.2.8. North America Drone In A Box Market, by End-User Industry |

|

9.2.9. North America Drone In A Box Market, by Component |

|

9.2.10. North America Drone In A Box Market, by |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Drone In A Box Market, by Application |

|

9.2.11.1.2. US Drone In A Box Market, by Type |

|

9.2.11.1.3. US Drone In A Box Market, by End-User Industry |

|

9.2.11.1.4. US Drone In A Box Market, by Component |

|

9.2.11.1.5. US Drone In A Box Market, by |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Percepto |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Skycatch |

|

11.3. Airobotics |

|

11.4. ABB |

|

11.5. Intel Corporation |

|

11.6. DJI Innovations |

|

11.7. Autel Robotics |

|

11.8. Flytrex |

|

11.9. PrecisionHawk |

|

11.10. Aerospace Technologies |

|

11.11. Ehang |

|

11.12. Airbus |

|

11.13. Lockheed Martin |

|

11.14. Parrot |

|

11.15. Kespry |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Drone in a Box Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Drone in a Box Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Drone in a Box Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA