As per Intent Market Research, the Disposable Incontinence Products Market was valued at USD 16.9 Billion in 2024-e and will surpass USD 27.8 Billion by 2030; growing at a CAGR of 7.3% during 2025-2030.

The disposable incontinence products market is experiencing steady growth driven by the rising global aging population, increased healthcare awareness, and the growing demand for comfort and convenience in personal hygiene management. These products, designed to manage urinary and fecal incontinence, include adult diapers, underpads, incontinence pads, liners, and protective underwear. The market is characterized by a broad range of product types designed to address different levels of incontinence, providing consumers with various options suited to their needs. Over the past decade, innovation in these products, including better absorbency, skin-friendly materials, and environmentally conscious alternatives, has fueled market expansion. This growth is further supported by a shift towards increased consumer awareness about incontinence management, driven by aging demographics and lifestyle changes.

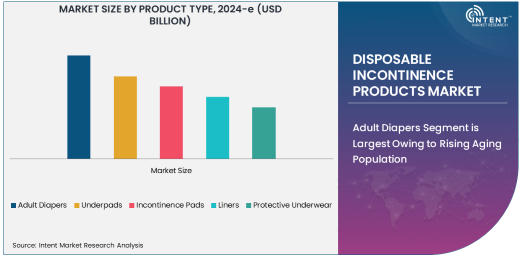

Adult Diapers Segment is Largest Owing to Rising Aging Population

The adult diapers segment dominates the disposable incontinence products market, primarily driven by the aging population. As the global population ages, the demand for products to manage urinary incontinence has surged. Adult diapers are particularly popular among elderly individuals who experience incontinence, as they provide an easy and convenient solution to manage the condition. Moreover, adult diapers have expanded their offerings with various designs, such as pull-ups, that offer enhanced comfort, discretion, and a more natural fit. The demand for these products is especially strong in developed regions, where higher healthcare awareness and advanced healthcare infrastructure support a large aging demographic.

These products are increasingly being seen as a necessity rather than a luxury, encouraging both hospitals and homecare settings to rely on them for patient care. With ongoing advancements in materials and design, such as super-absorbent polymers and breathable fabrics, adult diapers are continuously improving, which contributes to their widespread usage. Given their effectiveness, these products are projected to remain the largest segment within the disposable incontinence market in the coming years.

Homecare Settings Segment is Fastest Growing Owing to Aging Demographics

Among the various end-user industries, homecare settings represent the fastest growing segment in the disposable incontinence products market. As more people with incontinence prefer receiving care at home rather than in hospitals or long-term care facilities, there is an increasing demand for incontinence products designed for at-home use. The shift toward homecare can be attributed to several factors, including the desire for personalized care, the convenience of staying in a familiar environment, and cost-effectiveness compared to institutional care.

Homecare settings often require products like adult diapers, incontinence pads, and underpads, which offer ease of use for caregivers and patients alike. Furthermore, advancements in technology have enabled online retailers to meet the growing demand for these products, making them more accessible. The combination of demographic trends, increasing homecare reliance, and product accessibility through online channels is expected to continue fueling growth in this segment.

Online Retail Channel is Fastest Growing Owing to Increased Consumer Preference for Convenience

The online retail segment is the fastest growing distribution channel in the disposable incontinence products market. The ease of purchasing these products online offers significant advantages in terms of convenience, privacy, and the ability to compare different products. E-commerce platforms enable customers to access a wide variety of incontinence products from different brands, often at competitive prices. This has become especially important in markets where consumer preferences for convenience have increased, particularly in developed economies with high internet penetration.

Online retailers also offer subscription models and regular delivery options, which have further driven consumer adoption of disposable incontinence products. The growing number of e-commerce platforms dedicated to healthcare products and wellness has played a significant role in the expansion of this channel, and it is expected to continue its rapid growth. The rise of digital shopping behaviors, particularly among older populations, is shaping the future of the disposable incontinence product market.

Urinary Incontinence Application is Largest Owing to High Prevalence Rates

Urinary incontinence remains the largest application segment in the disposable incontinence products market. This is primarily due to the high prevalence of urinary incontinence among both men and women, especially in elderly populations. Factors such as aging, certain medical conditions, and childbirth contribute to the widespread occurrence of urinary incontinence, driving the demand for related products. In particular, adult diapers, underpads, and pads designed for urinary incontinence are widely used to manage the condition.

In addition to the aging population, increased awareness and acceptance of incontinence products have helped reduce the stigma associated with urinary incontinence, leading to higher consumption of these products. The medical community's focus on enhancing the quality of life for people with incontinence, coupled with continuous innovation in product design, is expected to sustain the dominance of this application in the market.

North America Region is Largest Owing to High Adoption Rates

North America is the largest region in the disposable incontinence products market, driven by high adoption rates in the United States and Canada. The aging population in North America, along with improved healthcare infrastructure, plays a significant role in the growth of this market. Healthcare systems in these countries provide comprehensive care for the elderly, and incontinence management is a key part of elderly care. Additionally, the widespread availability of incontinence products through multiple distribution channels, including online retail and pharmacies, contributes to the market’s dominance in this region.

Furthermore, North American consumers are increasingly seeking convenient and discreet incontinence solutions, which has prompted the development of innovative products. As disposable incontinence products become more mainstream, the region is expected to continue leading the market. The high purchasing power and healthcare access in North America ensure that demand for these products remains robust.

Competitive Landscape and Leading Companies

The disposable incontinence products market is highly competitive, with several key players dominating the industry. Leading companies such as Procter & Gamble, Kimberly-Clark Corporation, and Essity AB have a strong market presence, driven by their extensive distribution networks and established brands. These companies invest heavily in research and development to innovate and meet the evolving needs of consumers, focusing on factors such as comfort, absorbency, and skin health.

Competitive dynamics in the market are further shaped by the increasing presence of regional and local players who focus on cost-effective solutions to cater to price-sensitive segments. The entry of new players and growing competition from online retailers also contribute to price pressure, compelling established companies to enhance their product offerings and expand their reach through diverse distribution channels. Partnerships, acquisitions, and product innovations remain key strategies for companies aiming to maintain a competitive edge in the global market.

Recent Developments:

- Procter & Gamble introduced a new line of disposable incontinence products focused on enhanced absorbency and comfort.

- Kimberly-Clark announced the expansion of its manufacturing capabilities in Europe, aiming to increase production of its adult incontinence products.

- Unicharm has partnered with hospitals and healthcare institutions to offer bulk incontinence products to support patient care.

- Essity acquired a key regional player in the incontinence market to strengthen its product portfolio and reach in emerging markets.

- Hengan International has expanded its disposable incontinence products in supermarkets and online channels to better serve consumers.

List of Leading Companies:

- Procter & Gamble

- Kimberly-Clark Corporation

- Unicharm Corporation

- Essity AB

- Johnson & Johnson

- Ontex International

- Hengan International Group

- Medline Industries

- Cardinal Health

- First Quality Enterprises

- Attends Healthcare Products

- Domtar Corporation

- TENA (SCA Hygiene)

- Drylock Technologies

- Oji Holdings Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 16.9 Billion |

|

Forecasted Value (2030) |

USD 27.8 Billion |

|

CAGR (2025 – 2030) |

7.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Disposable Incontinence Products by Product Type (Adult Diapers, Underpads, Incontinence Pads, Liners, Protective Underwear), End-User Industry (Hospitals, Homecare Settings, Long-Term Care Facilities, Ambulatory Surgical Centers, Retail), Distribution Channel (Online Retail, Supermarkets/Hypermarkets, Pharmacies, Convenience Stores, Direct Sales), Application (Urinary Incontinence, Fecal Incontinence, Mixed Incontinence, Overflow Incontinence, Stress Incontinence) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Procter & Gamble, Kimberly-Clark Corporation, Unicharm Corporation, Essity AB, Johnson & Johnson, Ontex International, Hengan International Group, Medline Industries, Cardinal Health, First Quality Enterprises, Attends Healthcare Products, Domtar Corporation, TENA (SCA Hygiene), Drylock Technologies, Oji Holdings Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Disposable Incontinence Products Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Adult Diapers |

|

4.2. Underpads |

|

4.3. Incontinence Pads |

|

4.4. Liners |

|

4.5. Protective Underwear |

|

5. Disposable Incontinence Products Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Hospitals |

|

5.2. Homecare Settings |

|

5.3. Long-term Care Facilities |

|

5.4. Ambulatory Surgical Centers |

|

5.5. Retail |

|

6. Disposable Incontinence Products Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Online Retail |

|

6.2. Supermarkets/Hypermarkets |

|

6.3. Pharmacies |

|

6.4. Convenience Stores |

|

6.5. Direct Sales |

|

7. Disposable Incontinence Products Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Urinary Incontinence |

|

7.2. Fecal Incontinence |

|

7.3. Mixed Incontinence |

|

7.4. Overflow Incontinence |

|

7.5. Stress Incontinence |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Disposable Incontinence Products Market, by Product Type |

|

8.2.7. North America Disposable Incontinence Products Market, by End-User Industry |

|

8.2.8. North America Disposable Incontinence Products Market, by Distribution Channel |

|

8.2.9. North America Disposable Incontinence Products Market, by Application |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Disposable Incontinence Products Market, by Product Type |

|

8.2.10.1.2. US Disposable Incontinence Products Market, by End-User Industry |

|

8.2.10.1.3. US Disposable Incontinence Products Market, by Distribution Channel |

|

8.2.10.1.4. US Disposable Incontinence Products Market, by Application |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Procter & Gamble |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Kimberly-Clark Corporation |

|

10.3. Unicharm Corporation |

|

10.4. Essity AB |

|

10.5. Johnson & Johnson |

|

10.6. Ontex International |

|

10.7. Hengan International Group |

|

10.8. Medline Industries |

|

10.9. Cardinal Health |

|

10.10. First Quality Enterprises |

|

10.11. Attends Healthcare Products |

|

10.12. Domtar Corporation |

|

10.13. TENA (SCA Hygiene) |

|

10.14. Drylock Technologies |

|

10.15. Oji Holdings Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Disposable Incontinence Products Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Disposable Incontinence Products Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Disposable Incontinence Products Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA