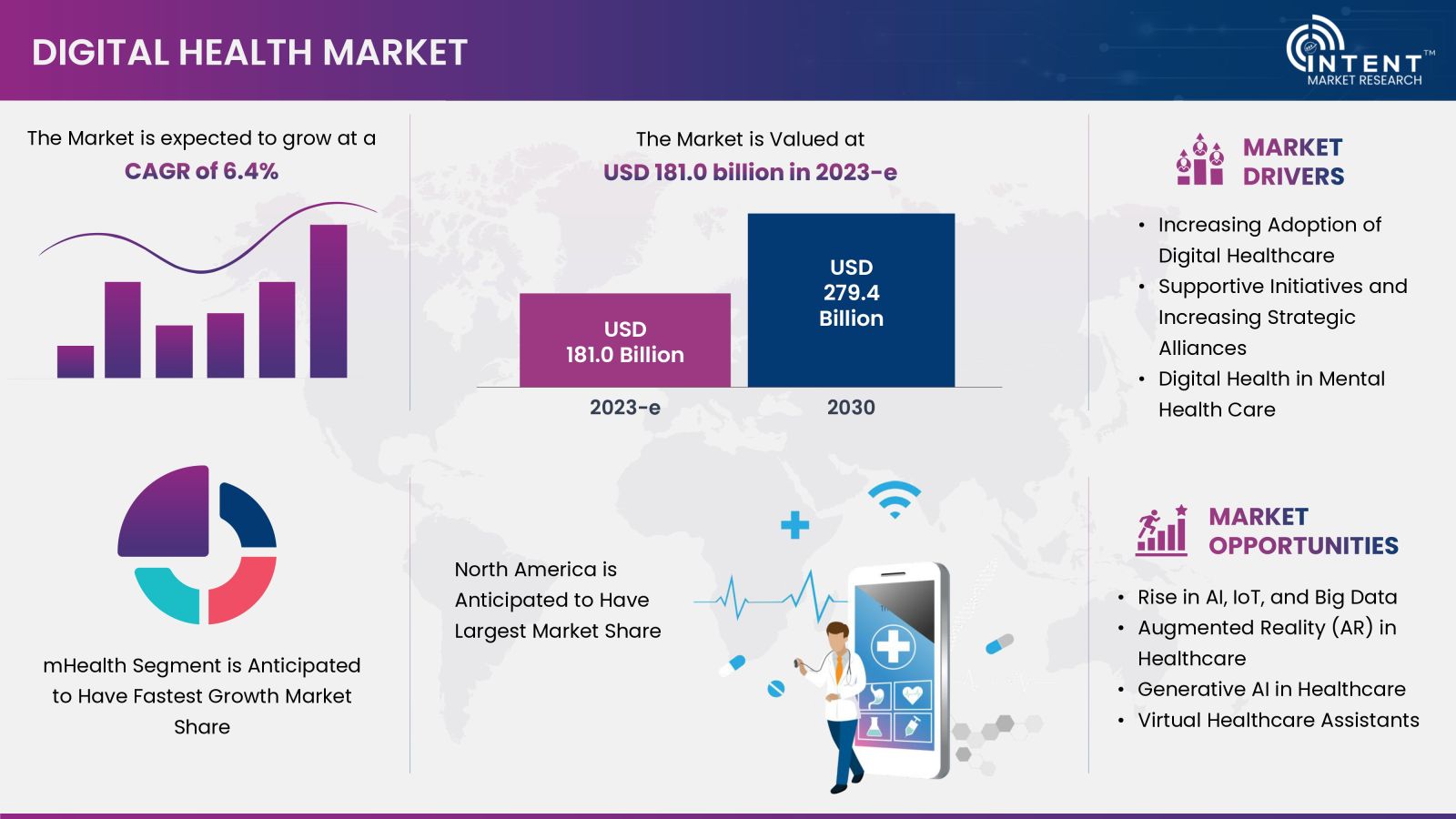

According to Intent Market Research, the Digital Health Market is expected to grow from USD 181.0 billion in 2023-e at a CAGR of 6.4% to touch USD 279.4 billion by 2030. The digital health market is dominated by key players such as Abbott, Beckman Coulter, Boston Scientific, Medtronic, J&J MedTech, Philips Healthcare, GE Healthcare, Siemens Healthineers, Teladoc, Samsung Healthcare, and McKesson. The increasing adoption of digital healthcare solutions is driving the overall market growth.

Click here to: Get FREE Sample Pages of this Report

The digital health market is anticipated to grow significantly due to various benefits associated with digital health such as chronic disease management with remote monitoring, expanding the reach of healthcare professionals, and enhanced patient-to-physician communication. The integration of advanced technologies such as AI, IoT, big data and healthcare analytics is shaping the global market landscape.

The increasing demand for digital health reflects the healthcare industry's recognition of its potential to enhance healthcare delivery and disease management. This trend is driving ongoing research and innovation in the field.

Digital Health Market Dynamics

Increasing Adoption of Digital Healthcare is Expected to Drive the Market over the Forecast Period

The rising adoption of digital health is attributed to the accelerated integration of well-established digital health technologies into conventional care operations. This deliberate initiative is poised to revolutionize the healthcare sector by improving effectiveness, lowering costs, and broadening access and capabilities for delivering care. The deployment of these technologies is expected to impact individuals' daily routines, propel progress in population health management, and ultimately play a role in enhancing global life expectancy and overall quality of life.

For instance, in January 2023, according to American Medical Association, a US-based organization, there was a surge in the utilization of telehealth, reaching a peak of 70% in 2020. Moreover, the percentage of physicians utilizing an accredited Electronic Health Record (EHR) system rose from 72% in 2019 to 78% in 2021. Therefore, the increasing adoption of digital health solutions is estimated to foster the digital health market growth.

COVID-19 has Significantly Boosted Use of Digital Health Solutions

The COVID-19 pandemic has accelerated the rise of digital health, which includes various solutions like telemedicine, remote monitoring, connected devices, digital health platforms, and health apps. This comprehensive concept extends to the analysis of health data and its application in big data systems, notably in epidemiological research and AI-driven diagnostic support. These solutions are instrumental in facilitating online medical consultations from home and enhancing the efficiency of patient diagnosis and treatment processes.

Teleconsultations have experienced an unprecedented surge amid the pandemic. In April 2020, telehealth visits comprised 69% of total ambulatory visits in the United States. KRY, a Swedish digital health provider, saw a doubling in demand for teleconsultations. Top Doctors' demand in Italy, Spain, and the UK surged thirtyfold. UK-based AccuRx quickly responded by developing a video chat tool in a weekend, facilitating over one million video consultations within months and being adopted by 6,700 doctors' practices.

Data security and privacy concerns may hinder the digital health market growth

In the present interconnected digital landscape, the healthcare sector heavily relies on technology to store, manage, and share patient information, creating a vulnerability to data breaches and cyber-attacks. The protection of health data is an essential requirement. In December 2023, Xtelligent, a US-based digital healthcare media and events company, published that the HHS Office for Civil Rights (OCR) received reports of healthcare data breaches involving over 540 organizations and affecting 112 million individuals. This marks a change from the figures of 2022, where 590 organizations reported breaches, impacting 48.6 million individuals. Such health data breaches may hinder the market.

Digital Health Market Segment Insights

The Hardware Segment Held the Largest Market Share

Hardware is an essential part of digital health devices, which includes wearable devices, trackers, remote patient monitoring devices, telehealth equipment, and point-of-care devices among others. These devices are designed to deliver healthcare solutions by remotely monitoring patient conditions through vital data measurement. These devices monitor health metrics such as heart rate, physical activity, and sleep patterns, and provide medication schedules and diet plans for weight management.

Major market players are developing innovative devices for remote monitoring of vital data of patients to deliver improved patient care. These monitoring devices are connected to healthcare solutions that display information on mobile applications. For instance, in January 2022, Roche, a Switzerland-based healthcare company, launched the Cobas pulse system, a professional blood glucose management solution equipped with mobile digital health features. This innovative product aims to enhance patient care within the healthcare industry.

.jpg)

mHealth Segment Is Anticipated to Be the Fastest Growing Market Share

The mHealth sector is poised to emerge as the most rapidly expanding market segment, owing to its diverse applications that encompass a wide range of activities. These activities include the dissemination of health information, remote monitoring of patients, data collection through mobile platforms, and the delivery of healthcare services. Leading entities within the market are actively developing mobile health solutions, particularly focusing on managing chronic diseases.

In October 2023, Abbott announced its collaboration with WeightWatchers, a US-based healthcare service company. Both the players jointly launched a mobile health app designed to assist individuals with diabetes in comprehending the impact of food and physical activity on their glucose levels.

Health & Fitness Segment Held the Largest Share in Digital Health Market

Health & fitness segment has captured the largest share in the digital health market. It involves adopting a lifestyle that fosters good health and optimal functioning of the body and mind. This includes engaging in regular physical activity and maintaining a balanced and nutritious diet. It also prioritizing mental well-being, practicing preventive health measures, ensuring sufficient sleep, and embracing a holistic approach that recognizes the interplay of various factors.

The rising awareness of personal health and fitness spending is changing the healthcare industry. Increasing shift towards exercise is leading to individuals, communities, and nations increasingly recognizing the importance of proactive health management. In January 2021, Sensor Tower, a US-based market intelligence and performance metrics company, stated that spending on mobile apps in the Health & Fitness category in Europe experienced a substantial year-over-year increase of 70.2% in 2020, reaching an estimated USD 544.2 million.

Hospitals & Clinics Segment To Drive the Digital Health Market

The healthcare landscape anticipates hospitals & clinics to secure the largest market share, primarily attributed to the integration of electronic health records (EHRs), telemedicine services, health information systems, mobile health applications, and wearable devices within these healthcare facilities.

The overarching goal is to optimize patient care, simplify administrative workflows, and foster improved communication among healthcare professionals. This concerted effort is designed to enhance operational efficiency and elevate healthcare outcomes within hospitals and clinics, positioning at the forefront of the evolving healthcare technology landscape.

Hospitals and clinics are increasing their digital health capabilities through collaboration with major players in the market. For instance, in May 2022, Honeywell, a US-based company announced a strategic collaboration with Narayana Health, an India-based private hospital. This collaboration is expected to empower Narayana Health to provide technology-driven, cost-effective, and easily accessible healthcare solutions for a broader audience.

North America is Anticipated to be the Largest Market Share in Digital Health Market

North America's held the largest share in the digital health market in 2023. The growth of digital health is attributed to factors such as robust healthcare infrastructure, rising adoption of digital health solutions and presence of major players. Major players in the market are focusing on development and commercialization of advanced remote health solutions. For instance, in October 2023, Ricoh USA, a US-based company launched RICOH Remote Patient Monitoring (RPM) Enablement, the latest comprehensive managed services solution tailored for health systems. This service aims to enhance RPM workflows, fostering greater efficiency and sustainability, ultimately contributing to enhanced experiences for both patients and care delivery teams.

Major Industry Players Are Enhancing Their Positions by Focusing On Technological Innovation

The market is characterized by intense competition due to the presence of numerous international and domestic players. The digital health market is dominated by key players such as Abbott, Fitbit, GE Healthcare, J&J MedTech, Masimo, McKesson, Medtronic, Omron Healthcare, Oracle Cerner, Philips, Roche, Samsung, Siemens Healthineers, Teladoc, and Veradigm (Allscripts) among others. These industry leaders are primarily focused on acquiring smaller players and developing advanced drug candidates to improve patient outcomes.

- In October 2023, Veradigm, a US-based healthcare company, and Holmusk, a Singapore-based digital health solutions and data analytics announced their strategic collaboration to fuel innovation in behavioral health. By utilizing each company's unique capabilities, the partnership fosters innovation in mental health and produces the data required to advance the area. During this second stage of the partnership, Holmusk's NeuroBlu Database will receive cohorts of millions of individuals with behavioral health issues and associated de-identified clinical data from Veradigm.

- In November 2022, Abbott, a US-based medical device and pharmaceutical company launched the FreeStyle LibreLink app to measure glucose levels without pricking. The glucose data is sent from the sensor to the mobile app via Near-Field Communication (NFC) technology. Their smartphone, users may use it to assist in managing their diet, insulin use, medicine, and exercise by tracking their eight-hour glucose history and real-time trend patterns.

Get your custom research report today

Digital Health Market Coverage

The report provides key insights into the digital health market, and it focuses on technological developments, trends, and initiatives taken by the government in this sector. The report delves into market drivers, restraints, and opportunities, and analyzes key players as well as the competitive landscape within the market. The report offers the market size and forecasts for the digital health market in value (USD billion) for all the above segments.

.jpg)

The report provides key insights into the digital health market, and it focuses on technological developments, trends, and initiatives taken by the government in this sector. The report delves into market drivers, restraints, and opportunities, and analyzes key players as well as the competitive landscape within the market. The report offers the market size and forecasts for the digital health market in value (USD billion) for all the above segments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023-e) | USD 181.0 billion |

| Forecast Revenue (2030) | USD 297.4 billion |

| CAGR (2024-2030) | 6.4% |

| Base Year for Estimation | 2023-e |

| Historic Year | 2022 |

| Forecast Period | 2024-2030 |

| Report Coverage | Market Forecast, Market Dynamics, Competitive Landscape, and Recent Developments |

| Segments Covered | By Offering (Software, Services, Hardware), By Technology (mHealth, Telehealth, Healthcare Analytics, Digital Health Systems, and Others), By Application (Health & Fitness, Disease Monitoring, Behavioural Health, and Others), By End-users (Hospitals & Clinics, Fitness Enthusiasts, and Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, France, UK, Spain, Italy), Asia Pacific (China, Japan, South Korea, India), Latin America (Brazil, Mexico, Argentina), Middle East and Africa (Saudi Arabia, South Africa, Turkey, United Arab Emirates) |

| Competitive Landscape | Abbott, Beckman Coulter, Biotricity, Boston Scientific, Carbon Health, DarioHealth, Doctor on Demand, Epic Systems, Fitbit, GE Healthcare, HXS, J&J MedTech, Masimo, McKesson, Medtronic, My mHealth, Noom, Omada Health, Omron Healthcare, Oracle Cerner, Persistent Systems, Philips Healthcare, Qardio, Qualcomm, Roche, Samsung Healthcare, Siemens Healthineers, Spring Health, Teladoc, Thermo Fisher, T-Systems, Veradigm (Allscripts), Verana Health, and Zyter |

| Customization Scope | Customization for segments, regions, and country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to choose from: single-user User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

|

1.Introduction |

|

1.1.Key Research Objective |

|

1.2.Market Definition |

|

1.3.Report Scope |

|

1.4.Currency & Conversion |

|

2.Research Methodology |

|

2.1.Research Approach |

|

2.2.Data Collection, Analysis And Interpretation |

|

2.3.Market Size Estimation & Data Triangulation |

|

2.4.Key Sources |

|

3.Executive Summary |

|

4.Market Insights |

|

4.1.Market Growth Drivers |

|

4.1.1.Increasing Adoption of Digital Healthcare |

|

4.1.2.Supportive Initiatives and Increasing Strategic Alliances |

|

4.1.3.Rise in AI, IoT, Big Data |

|

4.1.4.High Penetration of Smartphones |

|

4.1.5.Positive Impact of COVID-19 Pandemic On the Market |

|

4.2.Market Growth Restraints |

|

4.2.1.Data Security and Privacy Concerns |

|

4.2.2.Limited Access to Technology |

|

4.3.Market Growth Opportunities |

|

4.3.1.Augmented Reality (AR) in Healthcare |

|

4.3.2.Digital Health in Mental Health Care |

|

4.3.3.Healthcare Robotics |

|

4.4.Market Growth Challenges |

|

4.4.1.Lack of Interoperability |

|

4.4.2.Resistance to Change |

|

4.5.Market Growth Trends |

|

4.5.1.Virtual Healthcare Assistants |

|

4.5.2.Generative AI (GenAI) in Healthcare |

|

4.5.3.Digital Twins in Healthcare |

|

5.Premium Insights |

|

5.1.Regulatory Framework |

|

5.2.Use Case Analysis |

|

5.3.Technology Analysis |

|

6.Digital Health Market, By Offering (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.Software |

|

6.2.Services |

|

6.3.Hardware |

|

7.Digital Health Market, By Technology (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

7.1.mHealth |

|

7.1.1.Wearable |

|

7.1.2.Apps |

|

7.2.Telehealthcare |

|

7.3.Healthcare Analytics |

|

7.4.Digital Health Systems |

|

7.4.1.Electronic Health Records (EHR) |

|

7.4.2.E-prescribing System |

|

7.5.Others |

|

8.Digital Health Market, By Application (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

8.1.Health & Fitness |

|

8.2.Disease Monitoring |

|

8.3.Behavioural Health |

|

8.4.Others |

|

9.Digital Health Market, By End-users (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

9.1.Hospitals & Clinics |

|

9.2.Fitness Enthusiasts |

|

9.3.Others |

|

10.Digital Health Market, Regional Outlook (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

10.1.Global Market Synopsis |

|

10.2.North America |

|

10.2.1.North America Digital Health Market Outlook |

|

10.2.1.1.North America Digital Health Market, By Offering |

|

10.2.1.2. North America Digital Health Market, By Technology |

|

10.2.1.3. North America Digital Health Market, By Application |

|

10.2.1.4. North America Digital Health Market, By End-users |

|

*Note: Cross-segmentation by segments for each region will be covered as shown above. |

|

10.2.2.US |

|

10.2.2.1.US Digital Health Market, By Offering |

|

10.2.2.2.US Digital Health Market, By Technology |

|

10.2.2.3.US Digital Health Market, By Application |

|

10.2.2.4.US Digital Health Market, By End-users |

|

*Note: Cross-segmentation by segments for each country will be covered as shown above. |

|

10.2.3.Canada |

|

10.3.Europe |

|

10.3.1.Europe Digital Health Market Outlook |

|

10.3.2.UK |

|

10.3.3.Germany |

|

10.3.4.France |

|

10.3.5.Italy |

|

10.3.6.Rest of Europe |

|

10.4.Asia-Pacific |

|

10.4.1.Asia-Pacific Digital Health Market Outlook |

|

10.4.2.China |

|

10.4.3.India |

|

10.4.4.Japan |

|

10.4.5.South Korea |

|

10.4.6.Rest of APAC |

|

10.5.Latin America |

|

10.5.1.Latin America Digital Health Market Outlook |

|

10.6.Middle East & Africa |

|

10.6.1.Middle East & Africa Digital Health Market Outlook |

|

11.Competitive Landscape |

|

11.1.Market Share Analysis |

|

11.2.Company Strategy Analysis |

|

11.3.Competitive Matrix |

|

12.Company Profiles |

|

12.1.Major Players |

|

12.1.1.Abbott |

|

12.1.1.1.Company Synopsis |

|

12.1.1.2.Company Financials |

|

12.1.1.3.Product/Service Portfolio |

|

12.1.1.4.Recent Developments |

|

*Note: All the companies in section 12.1 will cover the same sub-chapters as above. |

|

12.1.2.Beckman Coulter |

|

12.1.3.Boston Scientific |

|

12.1.4.Epic Systems |

|

12.1.5.Fitbit |

|

12.1.6.GE Healthcare |

|

12.1.7.J&J MedTech |

|

12.1.8.Masimo |

|

12.1.9.McKesson |

|

12.1.10.Medtronic |

|

12.1.11.Omron Healthcare |

|

12.1.12.Oracle Cerner |

|

12.1.13.Philips Healthcare |

|

12.1.14.Qualcomm |

|

12.1.15.Roche |

|

12.1.16.Samsung Healthcare |

|

12.1.17.Siemens Healthineers |

|

12.1.18.Teladoc Health |

|

12.1.19.Thermo Fisher |

|

12.1.20.T-Systems |

|

12.1.21.Veradigm (Allscripts) |

|

12.1.22.Verana Health |

|

12.2.Start-ups |

|

12.2.1.Biotricity |

|

12.2.2.Carbon Health |

|

12.2.3.DarioHealth |

|

12.2.4.Doctor on Demand, Inc. |

|

12.2.5.HealthShare Exchange (HSX) |

|

12.2.6.My mHealth Limited |

|

12.2.7.Noom, Inc. |

|

12.2.8.Omada Health |

|

12.2.9.Qardio |

|

12.2.10.Spring Health |

|

12.2.11.Zyter |

|

13.Appendix |

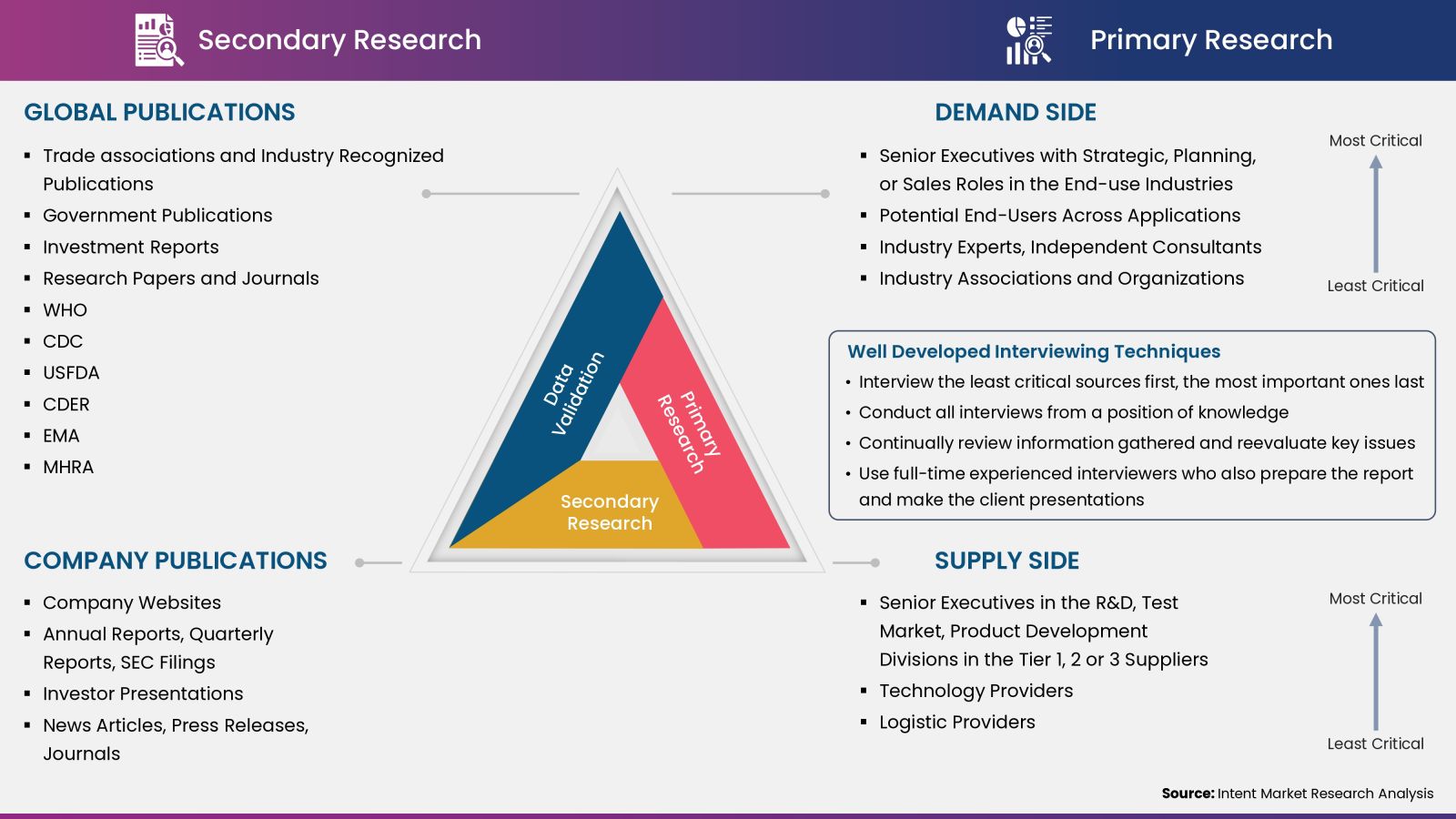

Intent Market Research employs a rigorous methodology to minimize residual errors by carefully defining the scope, validating findings through primary research, and consistently updating our in-house database. This dynamic approach allows us to capture ongoing market fluctuations and adapt to evolving market uncertainties.

The research factors used in our methodology vary depending on the specific market being analyzed. To begin with, we incorporate both demand and supply side information into our model to identify and address market gaps. Additionally, we also employ approaches such as Macro-Indicator Analysis, Factor Analysis, Value Chain-Based Sizing, and forecasting to further increase the accuracy of the numbers and validate the findings.

Research Approach

- Secondary Research Approach: During the initial phase of the research process, we acquire and accumulate extensive data continuously. This data is carefully filtered and validated through a variety of secondary sources.

- Primary Research Approach: Following the consolidation of data gathered through secondary research, we initiate a validation and verification process to verify all the market numbers and assumptions by engaging with the subject matter experts.

Data Collection, Analysis and Interpretation:

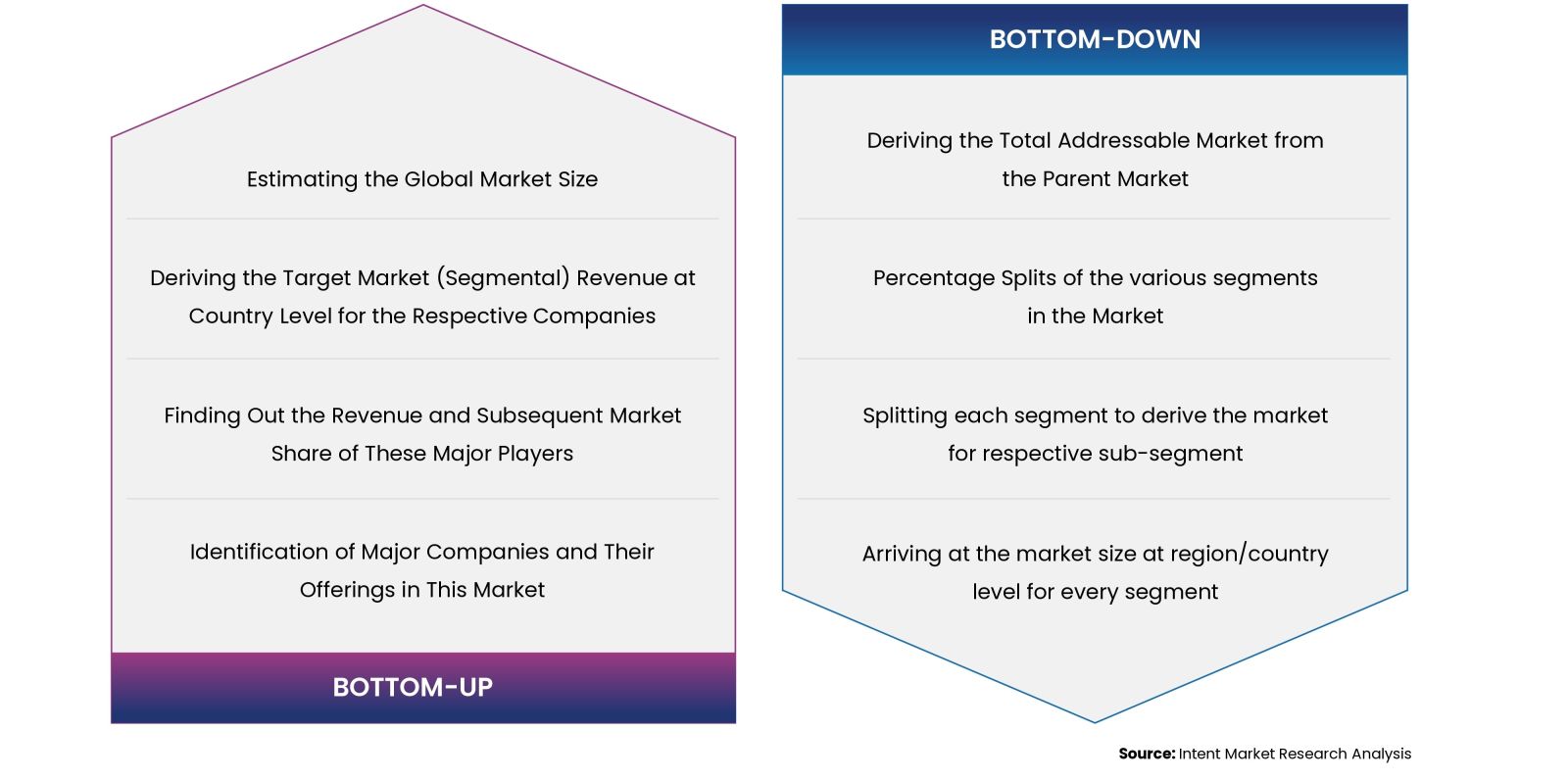

Research Methodology

Our market research methodology utilizes both top-down and bottom-up approaches to segment and estimate quantitative aspects of the market. We also employ multi-perspective analysis, examining the market from distinct viewpoints.