As per Intent Market Research, the Dental Autoclave Market was valued at USD 0.9 billion in 2024-e and will surpass USD 1.5 billion by 2030; growing at a CAGR of 9.3% during 2025 - 2030.

The dental autoclave market is witnessing significant growth, driven by the rising emphasis on sterilization and infection control in dental settings. As regulatory bodies impose stringent hygiene standards, the demand for advanced sterilization equipment continues to surge globally. Dental autoclaves, designed for efficient sterilization of instruments, play a pivotal role in ensuring patient safety and compliance with health standards.

Key trends influencing the market include technological advancements, such as automated cycles and faster sterilization processes, and the growing number of dental procedures worldwide. The increasing prevalence of dental disorders and the expansion of dental care infrastructure, particularly in developing regions, further fuel the demand for dental autoclaves.

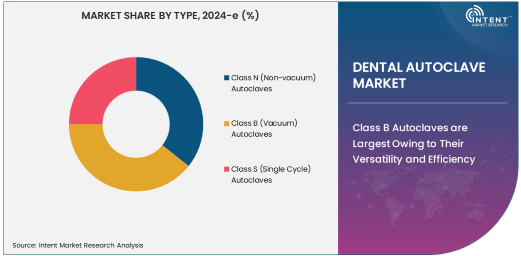

Class B Segment is Largest Owing to Superior Versatility

Class B autoclaves dominate the market, accounting for the largest share due to their versatility and ability to sterilize a wide variety of instruments. Equipped with advanced vacuum technology, these autoclaves ensure thorough sterilization by removing air pockets even in hollow instruments, which are commonly used in dental practices.

The segment benefits from the growing awareness among dental professionals about the importance of complete sterilization. Moreover, their compliance with global sterilization standards, such as EN 13060, makes Class B autoclaves a preferred choice for dental clinics and hospitals. Their ability to handle complex sterilization needs positions them as an essential component in modern dental care.

Steam Sterilization is Fastest Owing to High Efficiency

Steam sterilization is experiencing the fastest growth within the technology segment, driven by its proven efficiency and environmental sustainability. As a widely accepted method, it utilizes high-temperature steam to kill bacteria, viruses, and spores effectively, making it ideal for dental instruments.

This technology is gaining traction due to its quick processing times and compatibility with most reusable dental tools. Additionally, the push for eco-friendly sterilization solutions has bolstered its adoption, as it eliminates the need for chemical-based sterilants. Innovations in steam autoclaves, such as faster cycles and energy-efficient designs, further contribute to the growth of this subsegment.

Small Capacity Autoclaves Lead Owing to Growing Adoption in Clinics

Small capacity autoclaves, with a capacity of up to 20 liters, hold the largest share in the capacity segment, primarily due to their widespread use in dental clinics. These compact and cost-effective units are tailored to meet the sterilization needs of small-scale practices, where space and budget constraints are key considerations.

The segment's growth is supported by the rising number of independent dental practitioners and small clinics worldwide. Easy installation, portability, and the ability to handle frequent sterilization cycles make these autoclaves a popular choice among clinicians seeking reliable and efficient solutions.

Hospitals Segment is Fastest Owing to Increasing Patient Load

Among end-use industries, hospitals are the fastest-growing segment, driven by the increasing patient load and the need for large-scale sterilization solutions. With a higher frequency of complex dental surgeries and procedures, hospitals demand advanced autoclaves capable of processing larger instrument loads efficiently.

This growth is further propelled by the integration of dental care units within multi-specialty hospitals, particularly in urban areas. Hospitals often prefer advanced autoclave models with features like automated controls and higher sterilization speeds to ensure seamless operations in high-pressure environments.

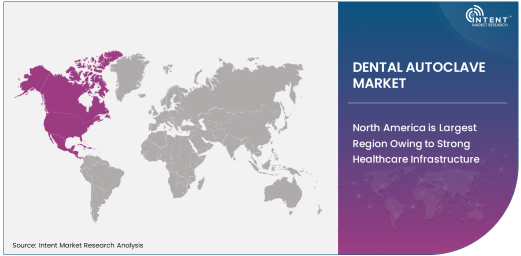

Asia-Pacific is Fastest Growing Region Owing to Expanding Infrastructure

The Asia-Pacific region is the fastest-growing market for dental autoclaves, fueled by the rapid expansion of healthcare infrastructure and increasing dental awareness. Countries like China, India, and Southeast Asian nations are witnessing a surge in dental clinics and hospitals, creating a robust demand for sterilization equipment.

Government initiatives aimed at improving oral healthcare and the rising prevalence of dental ailments further drive market growth in the region. Additionally, the cost-effectiveness of manufacturing in this region attracts global players, leading to a competitive and dynamic market landscape.

Competitive Landscape and Leading Companies

The dental autoclave market is marked by intense competition, with key players focusing on innovation and strategic partnerships to strengthen their market presence. Leading companies such as Midmark Corporation, Tuttnauer, and MELAG Medical Technology dominate the market with their diverse product portfolios and global distribution networks.

Emerging players are also making significant strides by introducing cost-effective and technologically advanced solutions tailored to regional demands. The competitive landscape is characterized by continuous advancements, such as faster sterilization cycles, energy efficiency, and user-friendly interfaces, ensuring a steady evolution of the market.

Recent Developments:

- In December 2024, Getinge AB launched an advanced Class B dental autoclave, featuring improved sterilization efficiency and faster cycle times, catering to high-demand dental clinics.

- In November 2024, SciCan unveiled a new portable dental autoclave aimed at small dental practices and mobile clinics, offering compact design and powerful sterilization.

- In October 2024, STERIS Corporation introduced an innovative vacuum-assisted autoclave, which significantly reduces energy consumption while maintaining high sterilization standards.

- In September 2024, Midmark Corporation received FDA approval for its new high-capacity dental autoclave, designed to handle larger volumes in hospital settings.

- In August 2024, MELAG Medizintechnik GmbH expanded its product range to include a high-efficiency autoclave for laboratories, improving both performance and sustainability.

List of Leading Companies:

- Tuttnauer

- Getinge AB

- Astell Scientific

- Belimed

- Midmark Corporation

- STERIS Corporation

- SciCan

- MELAG Medizintechnik GmbH & Co. KG

- Shinva Medical Instrument Co., Ltd.

- CISA S.p.A.

- CLEANING SYSTEMS

- Laoken

- Merck KGaA

- Sterifast

- ZIRBUS technology GmbH

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.9 billion |

|

Forecasted Value (2030) |

USD 1.5 billion |

|

CAGR (2025 – 2030) |

9.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Dental Autoclave Market By Type (Class N (Non-vacuum) Autoclaves, Class B (Vacuum) Autoclaves, Class S (Single Cycle) Autoclaves), By Technology (Steam Sterilization, Dry Heat Sterilization, Chemical Vapor Sterilization), By Capacity (Small Capacity Autoclaves (Up to 20 Liters), Medium Capacity Autoclaves (20-50 Liters), Large Capacity Autoclaves (Above 50 Liters)), By End-Use Industry (Dental Clinics, Hospitals, Dental Laboratories) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Tuttnauer, Getinge AB, Astell Scientific, Belimed, Midmark Corporation, STERIS Corporation, SciCan, MELAG Medizintechnik GmbH & Co. KG, Shinva Medical Instrument Co., Ltd., CISA S.p.A., CLEANING SYSTEMS, Laoken, Merck KGaA, Sterifast, ZIRBUS technology GmbH |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Dental Autoclave Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Class N (Non-vacuum) Autoclaves |

|

4.2. Class B (Vacuum) Autoclaves |

|

4.3. Class S (Single Cycle) Autoclaves |

|

5. Dental Autoclave Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Steam Sterilization |

|

5.2. Dry Heat Sterilization |

|

5.3. Chemical Vapor Sterilization |

|

6. Dental Autoclave Market, by Capacity (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Small Capacity Autoclaves (Up to 20 Liters) |

|

6.2. Medium Capacity Autoclaves (20-50 Liters) |

|

6.3. Large Capacity Autoclaves (Above 50 Liters) |

|

7. Dental Autoclave Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Dental Clinics |

|

7.2. Hospitals |

|

7.3. Dental Laboratories |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Dental Autoclave Market, by Type |

|

8.2.7. North America Dental Autoclave Market, by Technology |

|

8.2.8. North America Dental Autoclave Market, by Capacity |

|

8.2.9. North America Dental Autoclave Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Dental Autoclave Market, by Type |

|

8.2.10.1.2. US Dental Autoclave Market, by Technology |

|

8.2.10.1.3. US Dental Autoclave Market, by Capacity |

|

8.2.10.1.4. US Dental Autoclave Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Tuttnauer |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Getinge AB |

|

10.3. Astell Scientific |

|

10.4. Belimed |

|

10.5. Midmark Corporation |

|

10.6. STERIS Corporation |

|

10.7. SciCan |

|

10.8. MELAG Medizintechnik GmbH & Co. KG |

|

10.9. Shinva Medical Instrument Co., Ltd. |

|

10.10. CISA S.p.A. |

|

10.11. CLEANING SYSTEMS |

|

10.12. Laoken |

|

10.13. Merck KGaA |

|

10.14. Sterifast |

|

10.15. ZIRBUS technology GmbH |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Dental Autoclave Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Dental Autoclave Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Dental Autoclave Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA