As per Intent Market Research, the Data Center Robotics Market was valued at USD 4.0 billion in 2024-e and will surpass USD 11.2 billion by 2030; growing at a CAGR of 18.5% during 2024 - 2030.

The data center robotics market has experienced significant growth as the demand for automated solutions in data centers intensifies. With the rapid expansion of data-driven technologies, including cloud computing, artificial intelligence, and big data, the need for efficient, scalable, and secure data center operations has become paramount. Robotics in data centers helps streamline various processes such as server maintenance, inventory management, security, and cable management, offering improved operational efficiency, cost-effectiveness, and accuracy. The integration of robotics enables data center operators to handle large volumes of tasks that would traditionally require manual labor, reducing human error and optimizing workflows.

Automation through robotics is increasingly seen as a strategic investment in data center management, particularly as organizations seek to meet the growing demand for higher performance, reduced operational costs, and energy efficiency. Robotics solutions can facilitate 24/7 operations, provide real-time monitoring, and enhance the security and safety of critical data infrastructures. As the digital landscape continues to evolve, the data center robotics market is expected to expand rapidly, with diverse robotic solutions entering the market to meet specific operational needs.

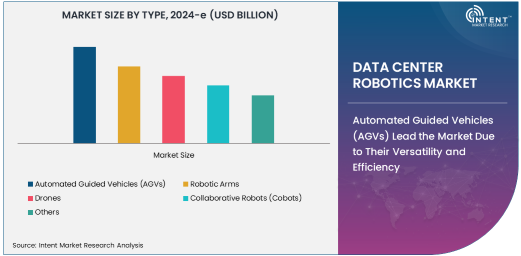

Automated Guided Vehicles (AGVs) Lead the Market Due to Their Versatility and Efficiency

Automated Guided Vehicles (AGVs) are the largest and fastest-growing segment in the data center robotics market. AGVs are highly versatile and can transport materials, servers, and other essential components within the data center, enabling efficient and automated handling of heavy or cumbersome objects. They operate on predefined paths using various technologies, including laser guidance, magnetic strips, and cameras, to navigate autonomously within the facility. This allows for streamlined logistics and inventory management, freeing up human resources for more strategic tasks.

AGVs are also instrumental in server maintenance and equipment relocation, as they can transport servers from one location to another, significantly reducing downtime and enhancing overall system availability. In addition, AGVs help with cable management and monitoring tasks by moving equipment or cables to designated areas, improving workflow organization and reducing the risk of accidents. With their flexibility and ability to reduce labor costs, AGVs are quickly becoming a key component of data center automation, particularly in large-scale facilities where manual labor would be inefficient or impractical. As the demand for more automated, scalable data centers rises, AGVs are poised to dominate the market in terms of both market share and growth rate.

Cloud Service Providers Drive Demand for Data Center Robotics

Cloud service providers are one of the largest end-users of data center robotics, largely due to the need for highly efficient and automated operations in their data centers. As the demand for cloud storage and computing services grows, these providers are looking to improve their operational capacity and reduce costs through automation. Robotics solutions such as AGVs, robotic arms, and collaborative robots (cobots) are increasingly being deployed in data centers to handle repetitive and time-consuming tasks, including server maintenance, cable management, and inventory monitoring.

Cloud service providers require large, complex data centers that can operate around the clock without human intervention. By integrating robotics, they can ensure greater operational efficiency, faster response times, and a reduced risk of downtime. Automation also enables these providers to scale their operations quickly, improving their ability to meet customer demands. As the cloud services market expands, the adoption of robotic solutions is expected to accelerate, further boosting the demand for data center robotics.

Hardware Segment Dominates the Market Due to Physical Infrastructure Needs

The hardware segment is the largest in the data center robotics market, as it includes the physical robots, automated guided vehicles, robotic arms, drones, and cobots that perform the majority of tasks within data centers. These systems are integral to the automation of data centers, providing the physical infrastructure required to move and manipulate materials, servers, cables, and other essential components.

Hardware-driven automation in data centers ensures that tasks such as server maintenance, inventory management, and data center monitoring can be performed with minimal human intervention, increasing productivity and operational uptime. As data centers grow larger and more complex, the demand for more advanced, efficient, and reliable hardware components will continue to rise. With technological advancements improving the capabilities and flexibility of robotics, the hardware segment will remain a key driver of growth in the data center robotics market.

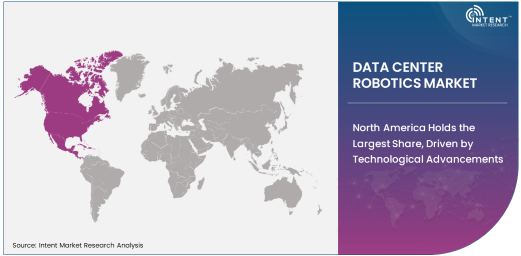

North America Holds the Largest Share, Driven by Technological Advancements

North America dominates the global data center robotics market, with the United States leading the charge due to its advanced technological infrastructure and concentration of data centers. The region is home to many of the world's largest cloud service providers, telecommunications companies, and IT infrastructure providers, all of whom are increasingly relying on robotics to enhance operational efficiency. With large-scale data centers being critical to the operations of cloud service providers and telecommunications companies, robotics solutions are being adopted to streamline various functions, from inventory management to server maintenance.

North American companies are also at the forefront of robotics development, investing heavily in research and development to improve automation solutions for data centers. The growing need for scalability, reliability, and energy efficiency in data centers has made automation through robotics a key strategy for reducing operational costs and enhancing productivity. As the digital landscape continues to expand, the North American region is expected to remain the largest market for data center robotics, with continued advancements in robotics technology driving further adoption in the region.

Competitive Landscape and Key Players

The data center robotics market is competitive, with several key players driving innovation and technological advancements in the sector. Leading companies such as KUKA Robotics, GreyOrange, ABB Ltd., Locus Robotics, and Fetch Robotics are at the forefront of developing robotics solutions for data centers. These companies offer a variety of robotic solutions, including AGVs, robotic arms, collaborative robots (cobots), and drones, which are designed to meet the specific needs of data centers in terms of automation, efficiency, and scalability.

In addition to established players, there are also several emerging companies focused on developing specialized robotics solutions tailored to data center applications. These companies are investing in the development of advanced sensors, artificial intelligence, and machine learning algorithms to enhance the capabilities of their robots, ensuring they can operate in dynamic, complex environments. Strategic partnerships, mergers and acquisitions, and collaborations with data center operators and cloud service providers are common strategies used by companies to strengthen their market position and expand their product offerings.

Recent Developments:

- ABB Ltd. introduced a new robotic system designed to streamline server maintenance and inventory management in large-scale data centers.

- Honeywell International Inc. launched an automated guided vehicle (AGV) specifically built for data center applications, enhancing operational efficiency.

- Fetch Robotics announced the integration of their collaborative robots into major cloud data centers, improving maintenance and logistics tasks.

- Siemens AG unveiled a new robotic arm designed to assist with high-precision tasks in the management and maintenance of data center infrastructure.

- KUKA AG expanded its robotics offering to include automated solutions for cable management and security in data centers.

List of Leading Companies:

- ABB Ltd.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- Qualcomm Technologies Inc.

- Teradyne Inc.

- Geek+

- Fetch Robotics

- Stäubli Robotics

- KUKA AG

- Panasonic Corporation

- Blue Prism

- Clearpath Robotics

- Dematic

- Locus Robotics

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 4.0 billion |

|

Forecasted Value (2030) |

USD 11.2 billion |

|

CAGR (2025 – 2030) |

18.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Data Center Robotics Market By Type (Automated Guided Vehicles (AGVs), Robotic Arms, Drones, Collaborative Robots (Cobots)), By Application (Server Maintenance, Data Center Monitoring, Inventory Management, Cable Management, Security and Surveillance), By End-User (Cloud Service Providers, Data Center Operators, Telecommunications Companies, IT Infrastructure Providers), By Component (Hardware, Software, Services) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ABB Ltd., Honeywell International Inc., Rockwell Automation Inc., Siemens AG, Qualcomm Technologies Inc., Teradyne Inc., Geek+, Fetch Robotics, Stäubli Robotics, KUKA AG, Panasonic Corporation, Blue Prism, Clearpath Robotics, Dematic, Locus Robotics |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Data Center Robotics Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Automated Guided Vehicles (AGVs) |

|

4.2. Robotic Arms |

|

4.3. Drones |

|

4.4. Collaborative Robots (Cobots) |

|

4.5. Others |

|

5. Data Center Robotics Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Server Maintenance |

|

5.2. Data Center Monitoring |

|

5.3. Inventory Management |

|

5.4. Cable Management |

|

5.5. Security and Surveillance |

|

5.6. Others |

|

6. Data Center Robotics Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Cloud Service Providers |

|

6.2. Data Center Operators |

|

6.3. Telecommunications Companies |

|

6.4. IT Infrastructure Providers |

|

7. Data Center Robotics Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hardware |

|

7.2. Software |

|

7.3. Services |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Data Center Robotics Market, by Type |

|

8.2.7. North America Data Center Robotics Market, by Application |

|

8.2.8. North America Data Center Robotics Market, by End-User |

|

8.2.9. North America Data Center Robotics Market, by Component |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Data Center Robotics Market, by Type |

|

8.2.10.1.2. US Data Center Robotics Market, by Application |

|

8.2.10.1.3. US Data Center Robotics Market, by End-User |

|

8.2.10.1.4. US Data Center Robotics Market, by Component |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. ABB Ltd. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Honeywell International Inc. |

|

10.3. Rockwell Automation Inc. |

|

10.4. Siemens AG |

|

10.5. Qualcomm Technologies Inc. |

|

10.6. Teradyne Inc. |

|

10.7. Geek+ |

|

10.8. Fetch Robotics |

|

10.9. Stäubli Robotics |

|

10.10. KUKA AG |

|

10.11. Panasonic Corporation |

|

10.12. Blue Prism |

|

10.13. Clearpath Robotics |

|

10.14. Dematic |

|

10.15. Locus Robotics |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Data Center Robotics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Data Center Robotics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Data Center Robotics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA