As per Intent Market Research, the Companion Animal Diagnostic Services Market was valued at USD 03.4 billion in 2024-e and will surpass USD 05.6 billion by 2030; growing at a CAGR of 8.9% during 2024 - 2030.

The companion animal diagnostic services market has witnessed significant growth in recent years, driven by the rising trend of pet ownership and increasing awareness about animal health. The growing prevalence of chronic and infectious diseases in pets, coupled with the need for early and accurate diagnosis, has propelled demand for advanced diagnostic services. Furthermore, the integration of advanced technologies, such as molecular diagnostics and diagnostic imaging, has revolutionized the way veterinarians diagnose and monitor animal health. This market is poised for substantial expansion as pet owners increasingly seek preventive care and wellness monitoring for their animals.

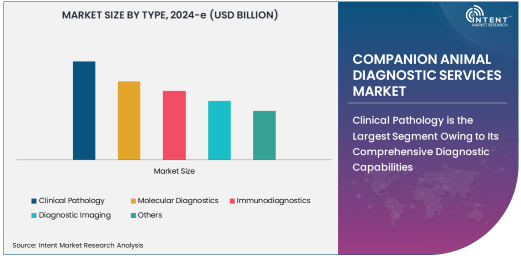

Clinical Pathology is the Largest Segment Owing to Its Comprehensive Diagnostic Capabilities

Clinical pathology dominates the companion animal diagnostic services market, primarily because of its ability to provide a broad spectrum of diagnostic insights. This segment includes tests for hematology, biochemistry, cytology, and urinalysis, which are essential for diagnosing a wide range of conditions in companion animals. The comprehensive nature of clinical pathology services makes it indispensable for routine health check-ups, disease detection, and treatment planning.

Veterinary clinics and hospitals rely heavily on clinical pathology to make informed decisions about an animal’s health. For example, blood tests can help detect infections, organ dysfunction, or nutritional deficiencies, while cytology can aid in diagnosing cancer and other cellular abnormalities. The increasing availability of point-of-care diagnostic devices and advanced laboratory services has further boosted the adoption of clinical pathology. This segment is expected to retain its dominant position as pet owners continue to demand high-quality, evidence-based care for their animals.

Disease Detection is Driving Market Growth Through Early Diagnosis

Disease detection stands out as the largest application in the companion animal diagnostic services market. The rising prevalence of diseases such as diabetes, cancer, heartworm, and tick-borne illnesses in pets has underscored the importance of early and accurate diagnostic services. Disease detection services encompass a variety of diagnostic methods, including blood tests, imaging techniques, and molecular diagnostics, which enable veterinarians to identify and treat conditions promptly.

The demand for disease detection is further fueled by the growing awareness among pet owners about the importance of regular veterinary visits and preventive care. Early diagnosis not only improves the prognosis for animals but also reduces treatment costs in the long run. As veterinary diagnostics continue to evolve, disease detection is likely to remain a key driver of market growth, supported by advancements in technology and the development of novel diagnostic tools.

Veterinary Clinics Lead the Market Owing to Accessibility and Trust

Veterinary clinics are the largest end-users of companion animal diagnostic services due to their widespread accessibility and the trust they have built with pet owners. Clinics often serve as the first point of contact for pet owners seeking medical care for their animals. They provide a range of diagnostic services, from routine health screenings to advanced imaging and molecular tests, ensuring comprehensive care for pets.

The convenience and affordability of veterinary clinics make them a preferred choice for pet owners. Moreover, many clinics have begun investing in state-of-the-art diagnostic equipment to offer in-house testing, reducing turnaround times and enhancing the overall quality of care. As the number of veterinary clinics continues to grow, especially in urban areas, this segment is expected to maintain its leading position in the market.

North America is the Largest Market Due to High Pet Ownership and Advanced Veterinary Infrastructure

North America dominates the companion animal diagnostic services market, driven by the region’s high rate of pet ownership and advanced veterinary infrastructure. The United States, in particular, has a well-established network of veterinary clinics and hospitals equipped with cutting-edge diagnostic technologies. Additionally, the growing trend of treating pets as family members has led to increased spending on their health and wellness.

The availability of pet insurance in North America has also contributed to the growth of the market, as it reduces the financial burden on pet owners and encourages them to seek timely diagnostic services. Furthermore, the presence of leading market players and ongoing research and development activities in veterinary diagnostics have solidified North America’s position as the largest regional market. The region is expected to continue its dominance, supported by increasing awareness about animal health and wellness.

Competitive Landscape and Key Players

The companion animal diagnostic services market is highly competitive, with key players focusing on innovation and expanding their service portfolios to meet the growing demand. Leading companies in this market include IDEXX Laboratories, Inc., Zoetis, Inc., Heska Corporation, Thermo Fisher Scientific, Inc., and Virbac, among others. These companies are investing heavily in research and development to introduce advanced diagnostic tools and technologies, such as PCR-based molecular diagnostics, digital imaging systems, and point-of-care diagnostic devices.

The competitive landscape is further shaped by strategic partnerships, mergers, and acquisitions aimed at enhancing market presence and broadening service offerings. For example, collaborations between diagnostic service providers and veterinary hospitals have enabled the integration of advanced diagnostic capabilities into routine veterinary care. As the market continues to evolve, competition is expected to intensify, with companies striving to differentiate themselves through innovation, quality, and customer service.

Recent Developments:

- IDEXX Laboratories, Inc. launched a new molecular diagnostic panel to enhance disease detection capabilities for veterinary professionals.

- Zoetis Inc. announced the expansion of its companion animal diagnostic portfolio by integrating advanced immunodiagnostic solutions.

- Heska Corporation introduced a wellness monitoring service that combines routine diagnostic testing with preventive healthcare solutions for pets.

- Hallmarq Veterinary Imaging unveiled a next-generation diagnostic imaging system designed specifically for small companion animals.

- Thermo Fisher Scientific partnered with veterinary clinics to develop point-of-care diagnostic tools for rapid disease detection in pets.

List of Leading Companies:

- IDEXX Laboratories, Inc.

- Zoetis Inc.

- Heska Corporation

- Virbac

- Thermo Fisher Scientific

- Neogen Corporation

- IDvet

- Randox Laboratories Ltd.

- Bio-Rad Laboratories, Inc.

- Agrolabo S.p.A.

- Abaxis, Inc. (A Zoetis Company)

- Fujifilm Holdings Corporation

- Hallmarq Veterinary Imaging

- scil animal care company GmbH

- Biocheck, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 03.4 billion |

|

Forecasted Value (2030) |

USD 05.6 billion |

|

CAGR (2025 – 2030) |

8.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Companion Animal Diagnostic Services Market By Type (Clinical Pathology, Molecular Diagnostics, Immunodiagnostics, Diagnostic Imaging), By Application (Disease Detection, Genetic Testing, Wellness Monitoring, Parasite Screening), By End-User (Veterinary Clinics, Veterinary Hospitals, Research Laboratories, Home Care Settings) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

IDEXX Laboratories, Inc., Zoetis Inc., Heska Corporation, Virbac, Thermo Fisher Scientific, Neogen Corporation, IDvet, Randox Laboratories Ltd., Bio-Rad Laboratories, Inc., Agrolabo S.p.A., Abaxis, Inc. (A Zoetis Company), Fujifilm Holdings Corporation, Hallmarq Veterinary Imaging, scil animal care company GmbH, Biocheck, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Companion Animal Diagnostic Services Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Clinical Pathology |

|

4.2. Molecular Diagnostics |

|

4.3. Immunodiagnostics |

|

4.4. Diagnostic Imaging |

|

4.5. Others |

|

5. Companion Animal Diagnostic Services Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Disease Detection |

|

5.2. Genetic Testing |

|

5.3. Wellness Monitoring |

|

5.4. Parasite Screening |

|

5.5. Others |

|

6. Companion Animal Diagnostic Services Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Veterinary Clinics |

|

6.2. Veterinary Hospitals |

|

6.3. Research Laboratories |

|

6.4. Home Care Settings |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Companion Animal Diagnostic Services Market, by Type |

|

7.2.7. North America Companion Animal Diagnostic Services Market, by Application |

|

7.2.8. North America Companion Animal Diagnostic Services Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Companion Animal Diagnostic Services Market, by Type |

|

7.2.9.1.2. US Companion Animal Diagnostic Services Market, by Application |

|

7.2.9.1.3. US Companion Animal Diagnostic Services Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. IDEXX Laboratories, Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Zoetis Inc. |

|

9.3. Heska Corporation |

|

9.4. Virbac |

|

9.5. Thermo Fisher Scientific |

|

9.6. Neogen Corporation |

|

9.7. IDvet |

|

9.8. Randox Laboratories Ltd. |

|

9.9. Bio-Rad Laboratories, Inc. |

|

9.10. Agrolabo S.p.A. |

|

9.11. Abaxis, Inc. (A Zoetis Company) |

|

9.12. Fujifilm Holdings Corporation |

|

9.13. Hallmarq Veterinary Imaging |

|

9.14. scil animal care company GmbH |

|

9.15. Biocheck, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Companion Animal Diagnostic Services Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Companion Animal Diagnostic Services Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Companion Animal Diagnostic Services Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA