As per Intent Market Research, the Wet Waste Management Market was valued at USD 29.4 Billion in 2024-e and will surpass USD 47.6 Billion by 2030; growing at a CAGR of 8.4% during 2025-2030.

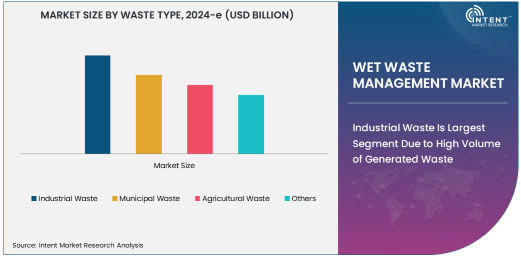

Industrial Waste Is Largest Segment Due to High Volume of Generated Waste

The wet waste management market is evolving rapidly due to increasing urbanization, industrialization, and environmental concerns. Among the various waste types, industrial waste represents the largest segment due to the large volume of waste generated by manufacturing processes, chemical production, and other industrial activities. Industrial waste often contains hazardous materials and requires specialized treatment methods to mitigate its environmental impact. Effective management of industrial waste is critical not only to comply with stringent environmental regulations but also to prevent soil and water contamination, making it a key focus of the wet waste management industry.

The industrial sector’s growing emphasis on sustainability and waste reduction is further driving the demand for efficient waste management solutions. Industrial waste management involves a combination of mechanical, chemical, and biological treatment technologies to handle waste streams effectively. As industries continue to prioritize sustainability in line with global environmental goals, the industrial waste segment is expected to maintain its leadership in the wet waste management market, contributing significantly to market growth.

Biological Treatment Is Fastest Growing Technology Due to Environmental Sustainability Focus

Biological treatment technology is the fastest growing segment in the wet waste management market, driven by the increasing demand for environmentally friendly and sustainable waste disposal methods. Biological treatment, such as composting, anaerobic digestion, and bioremediation, leverages natural processes to break down organic waste, making it a preferred method for managing wet waste, especially from municipal and agricultural sources. This approach not only helps reduce the environmental footprint of waste disposal but also enables the recovery of valuable by-products like biogas and compost.

As global concerns about waste management’s impact on climate change and resource depletion grow, biological treatment technologies are gaining traction due to their eco-friendly nature. The agricultural sector, in particular, is increasingly adopting biological treatment for managing organic waste such as crop residues, animal manure, and food waste. With governments and industries pushing for more sustainable solutions, biological treatment is poised to be a key driver of growth in the wet waste management market in the coming years.

Municipalities Are Largest End-User Due to Growing Urbanization and Waste Generation

Municipalities are the largest end-users in the wet waste management market, driven by the rapid growth of urban populations and the increased generation of municipal waste. The increasing volume of waste produced by urban centers, including food waste, yard waste, and household waste, has created a pressing need for efficient and sustainable waste management solutions. Municipalities are investing heavily in waste collection, sorting, and treatment infrastructure to handle the growing amounts of wet waste generated daily.

Municipal waste management involves various treatment methods, including biological, chemical, and mechanical processes, to ensure that waste is disposed of responsibly, or better yet, recycled or reused. With governments pushing for more sustainable urban development, municipalities are increasingly adopting advanced waste management technologies and integrating waste-to-energy solutions to reduce landfill usage and mitigate environmental impacts. The rapid urbanization occurring globally ensures that municipalities will remain the largest end-user segment in the wet waste management market.

Asia Pacific Is Fastest Growing Region Due to Increasing Waste Generation in Emerging Economies

Asia Pacific is the fastest growing region in the wet waste management market, driven by the rapid urbanization and industrialization occurring across emerging economies such as China, India, and Southeast Asian nations. The region is witnessing a sharp rise in municipal and industrial waste generation as urban populations grow and industries expand. Governments in Asia Pacific are increasingly prioritizing waste management and environmental sustainability, leading to significant investments in waste treatment infrastructure and technologies.

The adoption of advanced waste management practices, such as biological and chemical treatments, is accelerating in the region as countries strive to meet international environmental standards and combat pollution. Additionally, the growing focus on recycling and waste-to-energy technologies is expected to further fuel the growth of the wet waste management market in Asia Pacific. As the region continues to urbanize and industrialize, the demand for effective and efficient wet waste management solutions will only intensify, solidifying Asia Pacific as the fastest growing market.

Leading Companies and Competitive Landscape

The wet waste management market is competitive, with leading companies such as Veolia Environnement, SUEZ, Waste Management, Inc., Republic Services, and Clean Harbors dominating the global market. These companies are continuously expanding their service offerings and investing in innovative waste management technologies to meet the increasing demand for sustainable waste disposal and recycling solutions.

The competitive landscape is marked by a strong emphasis on research and development, with companies focusing on developing eco-friendly technologies and solutions to address the growing environmental concerns associated with waste disposal. Strategic collaborations, mergers, and acquisitions are common in this sector as companies aim to strengthen their position and expand their reach. Additionally, the growing trend toward circular economy models, which focus on reducing waste and reusing resources, is shaping the direction of innovation in the wet waste management market.

Recent Developments:

- Veolia Environment S.A. launched a new waste-to-energy project in North America, focusing on the conversion of wet waste into renewable energy.

- Waste Management, Inc. introduced advanced technologies for organic waste recycling, aiming to reduce methane emissions from landfills.

- Republic Services, Inc. partnered with municipalities to improve wet waste collection and composting programs for local communities.

- Covanta Holding Corporation expanded its wet waste treatment services to include wastewater treatment for industrial clients.

- Cleanaway Waste Management Ltd. announced a new organic waste processing facility that utilizes biological treatment methods to manage food and agricultural waste.

List of Leading Companies:

- Veolia Environment S.A.

- SUEZ Group

- Waste Management, Inc.

- Republic Services, Inc.

- Covanta Holding Corporation

- Clean Harbors, Inc.

- Stericycle, Inc.

- FCC Environment

- Remondis AG & Co. KG

- Biffa Plc

- Recology, Inc.

- Waste Connections, Inc.

- Cleanaway Waste Management Ltd.

- Advanced Disposal Services, Inc.

- GFL Environmental Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 29.4 Billion |

|

Forecasted Value (2030) |

USD 47.6 Billion |

|

CAGR (2025 – 2030) |

8.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wet Waste Management Market By Waste Type (Industrial Waste, Municipal Waste, Agricultural Waste), By Treatment Technology (Mechanical Treatment, Biological Treatment, Chemical Treatment), and By End-User (Municipalities, Industries, Agricultural Sector) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Veolia Environment S.A., SUEZ Group, Waste Management, Inc., Republic Services, Inc., Covanta Holding Corporation, Clean Harbors, Inc., Stericycle, Inc., FCC Environment, Remondis AG & Co. KG, Biffa Plc, Recology, Inc., Waste Connections, Inc., Cleanaway Waste Management Ltd., Advanced Disposal Services, Inc., GFL Environmental Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wet Waste Management Market, by Waste Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Industrial Waste |

|

4.2. Municipal Waste |

|

4.3. Agricultural Waste |

|

4.4. Others |

|

5. Wet Waste Management Market, by Treatment Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Mechanical Treatment |

|

5.2. Biological Treatment |

|

5.3. Chemical Treatment |

|

5.4. Others |

|

6. Wet Waste Management Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Municipalities |

|

6.2. Industries |

|

6.3. Agricultural Sector |

|

6.4. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Wet Waste Management Market, by Waste Type |

|

7.2.7. North America Wet Waste Management Market, by Treatment Technology |

|

7.2.8. North America Wet Waste Management Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Wet Waste Management Market, by Waste Type |

|

7.2.9.1.2. US Wet Waste Management Market, by Treatment Technology |

|

7.2.9.1.3. US Wet Waste Management Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Veolia Environment S.A. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. SUEZ Group |

|

9.3. Waste Management, Inc. |

|

9.4. Republic Services, Inc. |

|

9.5. Covanta Holding Corporation |

|

9.6. Clean Harbors, Inc. |

|

9.7. Stericycle, Inc. |

|

9.8. FCC Environment |

|

9.9. Remondis AG & Co. KG |

|

9.10. Biffa Plc |

|

9.11. Recology, Inc. |

|

9.12. Waste Connections, Inc. |

|

9.13. Cleanaway Waste Management Ltd. |

|

9.14. Advanced Disposal Services, Inc. |

|

9.15. GFL Environmental Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wet Waste Management Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wet Waste Management Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wet Waste Management Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA