As per Intent Market Research, the Bone and Joint Health Supplements Market was valued at USD 10.5 billion in 2024-e and will surpass USD 17.1 billion by 2030; growing at a CAGR of 8.6% during 2025 - 2030.

The bone and joint health supplements market is experiencing significant growth due to the increasing global prevalence of musculoskeletal disorders, including arthritis and osteoporosis. The aging population, rising sports injuries, and growing health consciousness are key drivers of this market. As people seek to maintain their mobility, prevent joint-related diseases, and promote overall bone health, the demand for supplements that support bone and joint health is steadily increasing. The growing focus on preventive healthcare and the rising awareness about the benefits of dietary supplements have further fueled the market expansion.

Technological advancements in supplement formulations, including the development of bioavailable ingredients and natural sources of collagen, are enhancing the effectiveness of bone and joint health products. Additionally, the growing popularity of e-commerce and retail platforms is making these supplements more accessible to consumers, contributing to the market's growth.

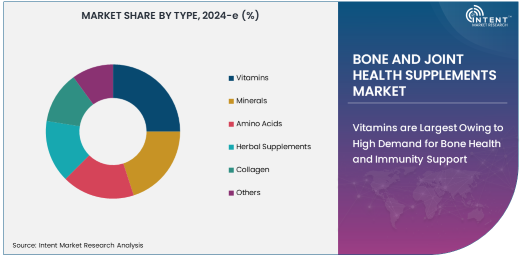

Vitamins are Largest Owing to High Demand for Bone Health and Immunity Support

Vitamins are the largest segment in the bone and joint health supplements market, driven by their critical role in maintaining bone density, joint function, and overall health. Vitamin D, in particular, is widely used to promote calcium absorption, which is essential for bone health, while Vitamin C supports collagen synthesis for joint flexibility. The increasing awareness of the importance of vitamins in preventing osteoporosis and arthritis, especially in aging populations, is driving the demand for these supplements.

Vitamins are often formulated in combination with other nutrients such as calcium and magnesium, making them a popular choice for individuals seeking to support bone strength and prevent musculoskeletal disorders. As the need for bone health supplements continues to rise, vitamins remain the dominant type in the market, particularly for consumers looking for easy-to-consume and effective products.

Tablets are Largest Form Owing to Convenience and Established Consumer Preference

Tablets are the largest form of bone and joint health supplements, primarily due to their convenience, ease of use, and established consumer preference. Tablets are widely available in the market and provide precise dosages of active ingredients, making them a preferred choice for individuals seeking reliable and consistent supplementation. The portability and shelf-stability of tablets also contribute to their widespread adoption, particularly among older adults and individuals with joint and bone health concerns.

Additionally, advancements in tablet formulations, such as time-release tablets and combination formulas, are enhancing the effectiveness of these supplements. As tablets remain the most common and trusted delivery form, they dominate the market, meeting the needs of a broad range of consumers.

Arthritis is Largest Application Owing to High Prevalence and Growing Demand for Pain Relief

Arthritis is the largest application in the bone and joint health supplements market, driven by the high prevalence of osteoarthritis and rheumatoid arthritis, particularly among older adults. These conditions, characterized by joint pain, inflammation, and reduced mobility, are major contributors to the demand for bone and joint health supplements. Arthritis patients are increasingly turning to dietary supplements that contain ingredients such as glucosamine, chondroitin, and MSM (methylsulfonylmethane) to support joint function, reduce inflammation, and alleviate pain.

The rising global prevalence of arthritis, coupled with the growing interest in natural and preventative remedies, is expected to continue driving the demand for bone and joint health supplements focused on arthritis relief. As arthritis remains a leading cause of disability worldwide, it represents the largest application in the bone and joint health supplements market.

Dietary Supplements is Largest End-User Owing to Growing Consumer Preference for Preventive Health

Dietary supplements are the largest end-user in the bone and joint health supplements market, driven by the increasing consumer preference for preventive healthcare. Individuals are becoming more proactive about maintaining their bone and joint health, and dietary supplements are a convenient and effective way to achieve this. As the population ages and the prevalence of bone and joint issues rises, more consumers are seeking supplements to support bone density, joint flexibility, and overall mobility.

The expansion of retail and e-commerce platforms, along with the increasing availability of a wide range of products tailored to specific needs (such as joint mobility or osteoporosis prevention), further fuels the growth of the dietary supplements segment. As consumer demand for natural and effective solutions continues to rise, dietary supplements remain the dominant end-user in the market.

North America is Largest Region Owing to High Prevalence of Bone and Joint Disorders

North America is the largest region in the bone and joint health supplements market, primarily due to the high prevalence of bone and joint disorders such as arthritis and osteoporosis, particularly among the aging population. The United States and Canada are major contributors to the region’s market growth, driven by a strong healthcare system, increased awareness of musculoskeletal health, and a high level of consumer spending on dietary supplements.

Additionally, North America's well-developed retail and e-commerce infrastructure makes bone and joint health supplements widely accessible to consumers. The region’s focus on preventive healthcare and the growing popularity of fitness and wellness trends further contribute to its market dominance.

Leading Companies and Competitive Landscape

The bone and joint health supplements market is highly competitive, with leading players such as GlaxoSmithKline, Amgen, Pfizer, and Nestlé Health Science dominating the space. These companies offer a wide range of bone and joint health supplements, including vitamins, minerals, collagen-based products, and herbal supplements.

The competitive landscape is characterized by ongoing product innovation, with companies focusing on developing new formulations, improving ingredient bioavailability, and offering personalized supplement solutions. Additionally, the rise of e-commerce and direct-to-consumer models has opened new opportunities for market players to reach a broader customer base. Strategic partnerships, acquisitions, and product diversification remain key strategies to strengthen market position and cater to the growing demand for bone and joint health supplements.

Recent Developments:

- In December 2024, Glanbia plc launched a new collagen-based joint health supplement. The product is designed to support joint function and reduce stiffness.

- In November 2024, Herbalife Nutrition Ltd. announced the expansion of its bone health product line. The new products contain high doses of calcium and vitamin D for better bone density.

- In October 2024, Nature's Bounty introduced a new glucosamine supplement for joint mobility. This supplement is targeted at older adults and athletes.

- In September 2024, Abbott Laboratories signed a partnership with an e-commerce platform to sell their joint health supplements online. This aims to make the products more accessible to consumers worldwide.

- In August 2024, Swanson Health Products added a new collagen supplement to its portfolio. The product is clinically tested and marketed for both bone and joint health.

List of Leading Companies:

- Glanbia plc

- Pfizer Inc.

- Amway Corporation

- Nestlé Health Science

- Nature's Bounty

- Herbalife Nutrition Ltd.

- Abbott Laboratories

- GNC Holdings, Inc.

- Swanson Health Products

- Hainan Yatai Health Food Co., Ltd.

- Doctor’s Best, Inc.

- Thorne Research

- Solgar Inc.

- NOW Foods

- New Chapter, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 10.5 billion |

|

Forecasted Value (2030) |

USD 17.1 billion |

|

CAGR (2025 – 2030) |

8.6% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Bone and Joint Health Supplements Market By Type (Vitamins, Minerals, Amino Acids, Herbal Supplements, Collagen), By Form (Tablets, Capsules, Powder, Liquid, Softgels), By Application (Arthritis, Osteoporosis, Sports Injuries, Joint Flexibility & Mobility), By End-User (Pharmaceuticals, Dietary Supplements, Sports Nutrition, Retail & E-commerce) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Glanbia plc, Pfizer Inc., Amway Corporation, Nestlé Health Science, Nature's Bounty, Herbalife Nutrition Ltd., Abbott Laboratories, GNC Holdings, Inc., Swanson Health Products, Hainan Yatai Health Food Co., Ltd., Doctor’s Best, Inc., Thorne Research, Solgar Inc., NOW Foods, New Chapter, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Bone and Joint Health Supplements Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Vitamins |

|

4.2. Minerals |

|

4.3. Amino Acids |

|

4.4. Herbal Supplements |

|

4.5. Collagen |

|

4.6. Others |

|

5. Bone and Joint Health Supplements Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Tablets |

|

5.2. Capsules |

|

5.3. Powder |

|

5.4. Liquid |

|

5.5. Softgels |

|

6. Bone and Joint Health Supplements Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Arthritis |

|

6.2. Osteoporosis |

|

6.3. Sports Injuries |

|

6.4. Joint Flexibility & Mobility |

|

6.5. Others |

|

7. Bone and Joint Health Supplements Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Pharmaceuticals |

|

7.2. Dietary Supplements |

|

7.3. Sports Nutrition |

|

7.4. Retail & E-commerce |

|

7.5. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Bone and Joint Health Supplements Market, by Type |

|

8.2.7. North America Bone and Joint Health Supplements Market, by Form |

|

8.2.8. North America Bone and Joint Health Supplements Market, by Application |

|

8.2.9. North America Bone and Joint Health Supplements Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Bone and Joint Health Supplements Market, by Type |

|

8.2.10.1.2. US Bone and Joint Health Supplements Market, by Form |

|

8.2.10.1.3. US Bone and Joint Health Supplements Market, by Application |

|

8.2.10.1.4. US Bone and Joint Health Supplements Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Glanbia plc |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Pfizer Inc. |

|

10.3. Amway Corporation |

|

10.4. Nestlé Health Science |

|

10.5. Nature's Bounty |

|

10.6. Herbalife Nutrition Ltd. |

|

10.7. Abbott Laboratories |

|

10.8. GNC Holdings, Inc. |

|

10.9. Swanson Health Products |

|

10.10. Hainan Yatai Health Food Co., Ltd. |

|

10.11. Doctor’s Best, Inc. |

|

10.12. Thorne Research |

|

10.13. Solgar Inc. |

|

10.14. NOW Foods |

|

10.15. New Chapter, Inc. |

|

11. Appendix= |

A comprehensive market research approach was employed to gather and analyze data on the Bone and Joint Health Supplements Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Bone and Joint Health Supplements Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Bone and Joint Health Supplements Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA