As per Intent Market Research, the Body Control Module Market was valued at USD 17.2 Billion in 2024-e and will surpass USD 29.7 Billion by 2030; growing at a CAGR of 8.1% during 2025-2030.

The Body Control Module (BCM) market has witnessed significant growth as the automotive industry continues to evolve with the integration of advanced electronics and vehicle automation. BCMS are essential in modern vehicles, as they manage and coordinate a variety of critical systems, including lighting, climate control, power windows, and advanced safety features. The growing demand for more connected and automated vehicles, including the rise of electric vehicles (EVs) and the increasing adoption of smart technology in vehicles, is propelling the BCM market. With advancements in automotive electronics, BCMS have become integral to enhancing the safety, efficiency, and user experience in vehicles.

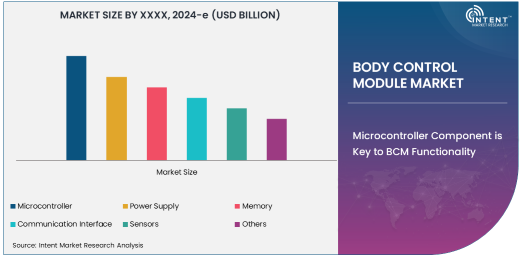

Microcontroller Component is Key to BCM Functionality

In the body control module, the microcontroller segment is the largest owing to its fundamental role in managing various electronic systems within a vehicle. Microcontrollers act as the brain of the BCM, processing signals and controlling the communication between different vehicle subsystems. The demand for more efficient, integrated, and high-performance microcontrollers has grown significantly as vehicles have become more complex and reliant on electronics. With the automotive industry leaning towards electrification and automation, microcontrollers that support advanced functionalities such as autonomous driving, enhanced safety features, and infotainment systems are expected to continue driving market growth.

Microcontrollers provide the computing power required to process data from various sensors and subsystems in real time. As car manufacturers prioritize the integration of features like driver assistance systems, lighting control, and HVAC management, the role of the microcontroller has expanded, creating a significant market demand for these components. Additionally, advancements in semiconductor technology and the push for more energy-efficient automotive electronics are likely to spur further growth in the microcontroller segment of the BCM market.

Electric Vehicles Segment is Fastest Growing

Among the different vehicle types, electric vehicles (EVs) are the fastest-growing segment in the BCM market. The global shift towards sustainable mobility, driven by environmental concerns and government regulations, has created a surge in demand for EVs. As electric vehicles rely heavily on advanced electronic systems, the need for efficient and intelligent body control modules has risen. BCMs in EVs manage not only traditional features like lighting and climate control but also essential systems related to battery management, regenerative braking, and energy optimization, making them even more critical in the electric vehicle sector.

The increasing adoption of electric vehicles is attributed to several factors, including technological advancements in battery efficiency, cost reductions in EV production, and favorable government policies and incentives. As EVs continue to grow in popularity, the demand for BCMs designed specifically for these vehicles is expected to expand. Additionally, with automakers shifting toward fully electric and hybrid vehicles, body control modules that provide seamless integration of powertrain systems and other electronic functionalities are becoming increasingly important in the EV market.

Lighting Control Application is Largest in BCM Systems

Lighting control remains the largest application segment in the body control module market. Vehicle lighting, including headlights, tail lights, interior lights, and indicator lights, is managed by the BCM to ensure optimal performance, safety, and efficiency. As automotive lighting technology evolves, with the rise of LED, adaptive, and matrix headlights, the role of BCMs in managing these systems becomes more complex and critical. BCMS help reduce energy consumption while providing the precise control needed for modern vehicle lighting systems.

The importance of lighting control has increased with the adoption of advanced lighting technologies, which offer enhanced visibility and safety for drivers. The growing focus on improving driver safety and compliance with global lighting regulations further drives the demand for more sophisticated BCM systems that can manage these lighting features efficiently. Additionally, as vehicles incorporate more intelligent lighting systems, the demand for integrated body control modules that can coordinate lighting with other vehicle functions will continue to grow.

OEMs Segment is Largest End-User

Original Equipment Manufacturers (OEMs) dominate the body control module market in terms of end-users. OEMs are the largest consumers of BCMs as they integrate these systems into their vehicle production lines. As automotive manufacturers continue to prioritize the incorporation of advanced electronic systems to meet consumer demands for safety, comfort, and connectivity, the role of OEMs in the body control module market becomes increasingly important. OEMs leverage BCMs to ensure that vehicles meet regulatory standards and provide the latest features in terms of infotainment, driver assistance, and vehicle security.

The growing demand for electric vehicles, autonomous systems, and connected car technologies has further boosted the demand for body control modules from OEMs. Manufacturers are working closely with semiconductor and electronics companies to develop BCMs that can handle the complexity and integration of these advanced technologies. The OEM market segment is expected to continue expanding as new vehicle models and technologies are introduced, making BCMs a vital component of modern automotive production.

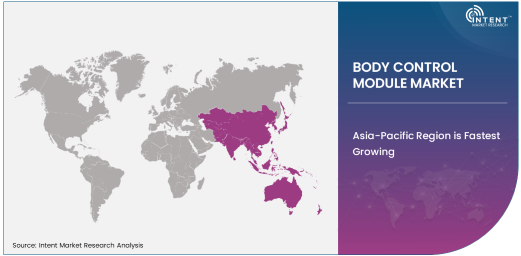

Asia-Pacific Region is Fastest Growing

The Asia-Pacific region is the fastest-growing market for body control modules, driven by the increasing production and adoption of vehicles, particularly electric vehicles, in countries like China, Japan, and South Korea. The rapid growth of the automotive industry in this region, along with significant investments in the electric vehicle market, is propelling the demand for body control modules. Moreover, the region's strong automotive manufacturing base, including major automakers such as Toyota, Hyundai, and Honda, further contributes to the demand for BCMs. As the Asia-Pacific region continues to lead in automotive production and sales, it is expected to remain a key driver of the BCM market's growth.

In addition to vehicle production, Asia-Pacific is also a hub for semiconductor and electronics manufacturing, which directly impacts the supply of critical components like microcontrollers and sensors used in BCMs. As the region continues to innovate and expand its automotive sector, the demand for advanced BCM systems that integrate seamlessly with new vehicle technologies is expected to rise, making it a critical area for market growth.

Competitive Landscape

The body control module market is highly competitive, with several global players vying for market share. Leading companies such as Bosch, Continental AG, and Denso Corporation dominate the market, driving innovation and developing advanced BCM systems tailored to the evolving needs of the automotive industry. These companies focus on integrating cutting-edge technologies such as artificial intelligence, advanced sensors, and communication protocols into their BCM solutions to meet the growing demand for connected, autonomous, and electric vehicles.

As the market becomes more technology-driven, the competitive landscape is also shifting towards strategic partnerships and collaborations between automotive manufacturers, semiconductor suppliers, and electronics firms. Companies are increasingly working together to develop next-generation body control modules that can manage complex vehicle systems. This trend is expected to intensify as automakers push the boundaries of vehicle connectivity, automation, and electrification.

Recent Developments:

- Bosch announced the launch of its new integrated body control module designed to support electric vehicles (EVs) with improved energy efficiency and communication capabilities.

- Continental AG revealed a partnership with an EV manufacturer to deliver next-generation body control modules that will enhance in-vehicle connectivity and advanced driver assistance features.

- Denso Corporation introduced an innovative BCM for electric vehicles, focusing on seamless integration with vehicle battery systems to optimize energy consumption.

- Aptiv PLC signed an agreement with a major automaker to supply advanced body control modules for an upcoming line of autonomous and electric vehicles, enhancing their functionality.

- Valeo launched a new range of body control modules, focusing on smart lighting and safety systems, aimed at providing a more connected and safe driving experience for both traditional and electric vehicles.

List of Leading Companies:

- Bosch

- Continental AG

- Denso Corporation

- Delphi Technologies

- Magneti Marelli

- Harman International

- Lear Corporation

- Aptiv PLC

- ZF Friedrichshafen AG

- Valeo

- Visteon Corporation

- Hyundai Mobis

- Toshiba Corporation

- Autoliv Inc.

- NXP Semiconductors

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 17.2 Billion |

|

Forecasted Value (2030) |

USD 29.7 Billion |

|

CAGR (2025 – 2030) |

8.1% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Body Control Module Market By Component (Microcontroller, Power Supply, Memory, Communication Interface, Sensors), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles), By Application (Lighting Control, Climate Control, Power Windows, Infotainment Systems, Advanced Driver Assistance Systems, Door Control), By End-User (OEMs, Aftermarket), and By Region; Global Insights & Forecast (2023 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Bosch, Continental AG, Denso Corporation, Delphi Technologies, Magneti Marelli, Harman International, Lear Corporation, Aptiv PLC, ZF Friedrichshafen AG, Valeo, Visteon Corporation, Hyundai Mobis, Toshiba Corporation, Autoliv Inc., NXP Semiconductors |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Body Control Module Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Microcontroller |

|

4.2. Power Supply |

|

4.3. Memory |

|

4.4. Communication Interface |

|

4.5. Sensors |

|

4.6. Others |

|

5. Body Control Module Market, by Vehicle Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Passenger Cars |

|

5.2. Commercial Vehicles |

|

5.3. Electric Vehicles (EVs) |

|

6. Body Control Module Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Lighting Control |

|

6.2. Climate Control |

|

6.3. Power Windows |

|

6.4. Infotainment Systems |

|

6.5. Advanced Driver Assistance Systems (ADAS) |

|

6.6. Door Control |

|

6.7. Others |

|

7. Body Control Module Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. OEMs (Original Equipment Manufacturers) |

|

7.2. Aftermarket |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Body Control Module Market, by Component |

|

8.2.7. North America Body Control Module Market, by Vehicle Type |

|

8.2.8. North America Body Control Module Market, by Application |

|

8.2.9. North America Body Control Module Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Body Control Module Market, by Component |

|

8.2.10.1.2. US Body Control Module Market, by Vehicle Type |

|

8.2.10.1.3. US Body Control Module Market, by Application |

|

8.2.10.1.4. US Body Control Module Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Bosch |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Continental AG |

|

10.3. Denso Corporation |

|

10.4. Delphi Technologies |

|

10.5. Magneti Marelli |

|

10.6. Harman International |

|

10.7. Lear Corporation |

|

10.8. Aptiv PLC |

|

10.9. ZF Friedrichshafen AG |

|

10.10. Valeo |

|

10.11. Visteon Corporation |

|

10.12. Hyundai Mobis |

|

10.13. Toshiba Corporation |

|

10.14. Autoliv Inc. |

|

10.15. NXP Semiconductors |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Body Control Module Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Body Control Module Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Body Control Module Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA