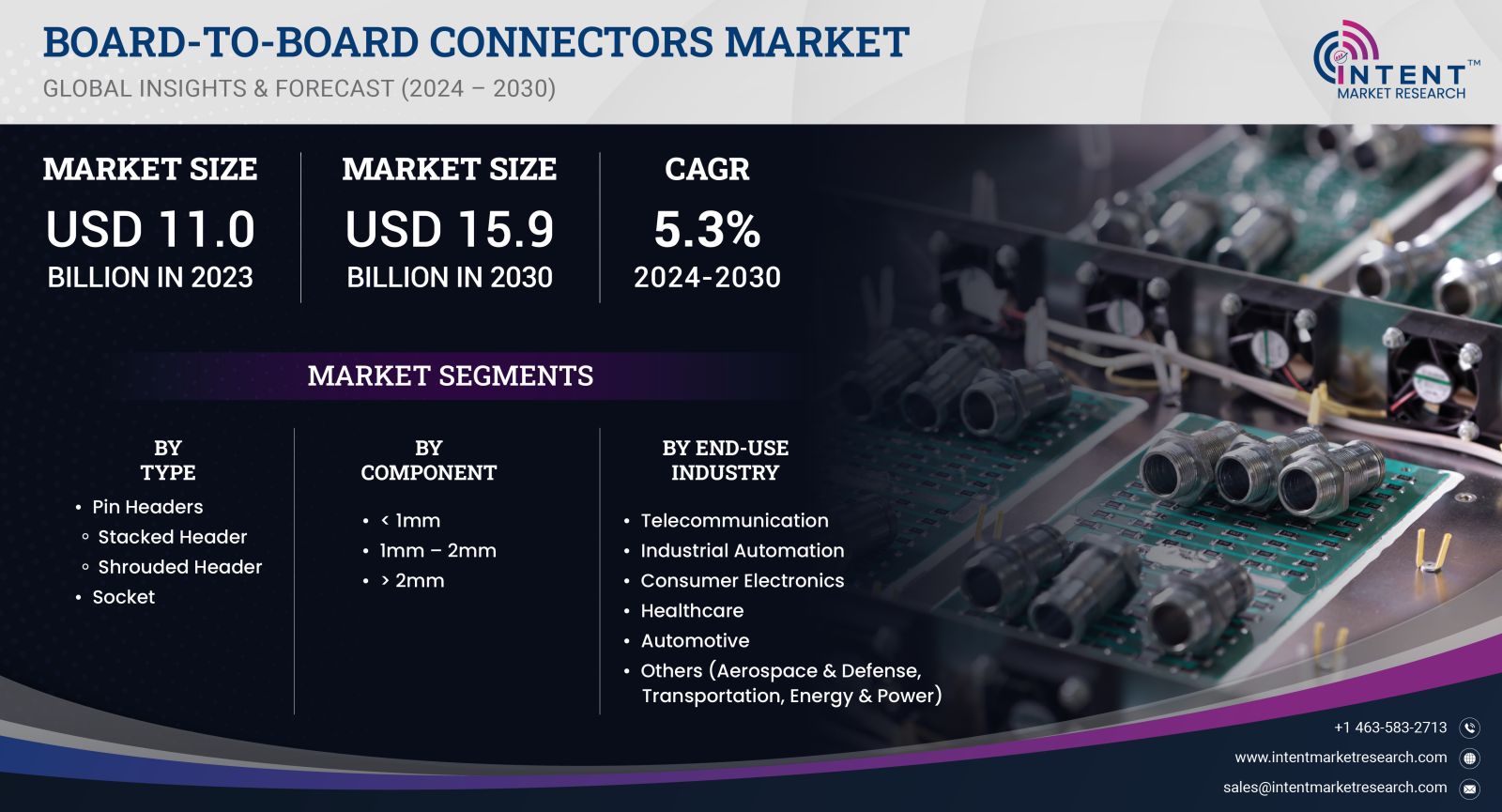

As per Intent Market Research, the Board-To-Board Connectors Market was valued at USD 11.0 billion in 2023-e and will surpass USD 15.9 billion by 2030; growing at a CAGR of 5.3% during 2024 - 2030.

The Board-to-Board Connectors Market is set to witness robust growth over the forecast period of 2024 to 2030, driven by increasing demand from sectors such as telecommunications, automotive, industrial automation, and consumer electronics. These connectors are essential for enabling communication between two printed circuit boards (PCBs) in various devices, offering versatility and high performance in densely packed electronics. Technological advancements in miniaturization and the increasing need for efficient, high-speed data transmission are significant growth drivers.

Automotive Segment is Fastest Growing Owing to Electric Vehicle (EV) Adoption

The automotive segment is anticipated to be the fastest-growing sector in the board-to-board connectors market, driven largely by the rapid expansion of the electric vehicle (EV) industry. EVs require high-reliability connectors to manage electrical systems, power management, and advanced safety features, all of which have boosted the demand for board-to-board connectors. The increasing shift toward autonomous driving and connected vehicles is also accelerating growth in this subsegment.

Within this segment, high-power connectors are expected to exhibit the highest growth rate due to their importance in managing the energy needs of electric and hybrid vehicles. These connectors ensure robust power transmission in harsh environments, which is essential for battery management systems (BMS) and other power-sensitive areas in EVs. As global automotive manufacturers invest in the electrification of their fleets, the demand for these connectors is projected to surge.

Consumer Electronics Segment is Largest Owing to Smartphone and Wearable Technology

The consumer electronics segment is the largest contributor to the board-to-board connectors market, owing to the continued global demand for smartphones, tablets, and wearable devices. The miniaturization trend in consumer electronics, along with increasing performance requirements, has made board-to-board connectors indispensable in this segment. With an ever-growing emphasis on thin, lightweight devices that deliver high performance, connectors must be compact while providing high-speed, reliable connections.

Within the consumer electronics sector, the smartphone subsegment remains the largest in terms of revenue. Smartphones require connectors to ensure proper communication between internal components, such as cameras, displays, and memory modules. As 5G technology proliferates, and smartphones become more complex with multi-camera systems and foldable designs, the demand for innovative connector solutions is expected to remain robust, solidifying this subsegment's dominance in the market.

Industrial Automation Segment is Fastest Growing Owing to IIoT Integration

In the industrial automation sector, board-to-board connectors are becoming increasingly critical as more industries adopt Industrial Internet of Things (IIoT) technologies. The integration of IIoT systems in manufacturing plants, supply chain operations, and monitoring systems is driving the need for robust, high-performance connectors that can handle large data transfers and operate in demanding environments.

The robotics and automation subsegment is poised to experience the fastest growth within this category, as more industries turn to automated systems to improve efficiency and reduce operational costs. Advanced manufacturing systems, which rely on real-time data exchange between machines, sensors, and control units, are creating a significant demand for durable, high-speed connectors that can ensure uninterrupted communication between electronic components.

Telecommunication Segment is Largest Owing to 5G Infrastructure Development

The telecommunication segment is another major revenue generator for the board-to-board connectors market, especially with the rapid global deployment of 5G infrastructure. Telecom companies are heavily investing in next-generation network equipment that requires reliable and fast connectors to ensure high-speed data transmission across long distances.

The largest subsegment in this category is 5G base stations, which are critical for enabling high-speed internet and network services. These base stations use a wide range of connectors to manage high-frequency signals and data transmission, both of which are critical for maintaining the ultra-low latency and high-speed performance of 5G networks. As more countries roll out their 5G networks, the demand for board-to-board connectors in telecom infrastructure is expected to remain strong throughout the forecast period.

Data Centers Segment is Fastest Growing Owing to Cloud Computing and Edge Data Growth

The data centers segment is projected to grow at a significant rate, driven by the explosion of data traffic from cloud computing, edge computing, and artificial intelligence (AI) applications. Data centers rely on board-to-board connectors for their servers, storage systems, and networking equipment, all of which require fast, reliable data transfer capabilities to manage large volumes of information.

Within this segment, the server and storage subsegment is expected to be the fastest-growing due to the increasing need for scalable and high-performance computing solutions. The rise of AI-driven applications and real-time data analytics has led to a surge in demand for advanced data center solutions, further propelling the need for reliable connectors that can handle large data flows and prevent downtime.

Fastest Growing Region: Asia-Pacific Owing to Consumer Electronics and Industrial Growth

The Asia-Pacific region is forecast to be the fastest-growing region in the board-to-board connectors market, with a projected CAGR of 7.1% from 2024 to 2030. This rapid growth is primarily driven by the booming consumer electronics and industrial automation sectors in countries such as China, Japan, and South Korea. The region's strong manufacturing base, coupled with increasing investments in 5G infrastructure and electric vehicle production, is further bolstering the demand for board-to-board connectors.

China is expected to dominate the regional market, owing to its position as a global leader in electronics manufacturing and the ongoing push toward industrial digitization and automation. Additionally, the increasing adoption of smart home technologies and wearable devices in the region is expected to drive sustained growth in the consumer electronics segment.

Competitive Landscape: Leading Players and Market Positioning

The board-to-board connectors market is highly competitive, with several global and regional players vying for market share. Leading companies are focusing on product innovations, partnerships, and acquisitions to strengthen their market presence. Top players are also investing heavily in research and development to cater to the growing demand for miniaturized, high-performance connectors across various industries.

Some of the top companies in this market include:

- TE Connectivity – A leader in the automotive and industrial sectors, offering a wide range of connectors for harsh environments.

- Amphenol Corporation – Known for its diverse product portfolio in telecommunications, data centers, and aerospace.

- Molex LLC – Specializes in connectors for consumer electronics, automotive, and industrial automation applications.

- Hirose Electric Co., Ltd. – A Japanese company renowned for its high-quality connectors in consumer electronics and automotive industries.

- JST Mfg. Co., Ltd. – Focuses on automotive and telecommunications connectors.

- Samtec, Inc. – Strong presence in the high-performance computing and telecom sectors.

- Foxconn Interconnect Technology – A major player in consumer electronics and data centers.

- Kyocera Corporation – Specializes in connectors for telecommunication and automotive sectors.

- 3M – Offers a broad range of connectors for industrial and consumer electronics.

- Yazaki Corporation – A key player in the automotive industry with a focus on high-power connectors for electric vehicles.

The competitive landscape is characterized by constant innovation, with companies focusing on miniaturization, durability, and high data-transfer capabilities to meet the evolving demands of various end-use industries. Partnerships with OEMs (Original Equipment Manufacturers) are also becoming a key strategy to secure long-term contracts and enhance market presence.

Report Objectives:

The report will help you answer some of the most critical questions in the Board-To-Board Connectors Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the board-to-board connectors market?

- What is the size of the board-to-board connectors market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023-e) |

USD 11.0 billion |

|

Forecasted Value (2030) |

USD 15.9 billion |

|

CAGR (2024-2030) |

5.3% |

|

Base Year for Estimation |

2023-e |

|

Historic Year |

2022 |

|

Forecast Period |

2024-2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Board-to-Board Connectors Market By Type (Sockets, Pin Headers), By Component (< 1mm, 1mm - 2mm, >2mm), By End-use (Consumer Electronics, Industrial Automation, Healthcare, Telecommunication) |

|

Regional Analysis |

North America (US, Canada), Europe (Germany, France, UK, Spain, Italy & Rest of Europe), Asia Pacific (China, Japan, South Korea, India, and rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, & Rest of Latin America), Middle East & Africa (Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1.Introduction |

|

1.1.Market Definition |

|

1.2.Scope of the Study |

|

1.3.Research Assumptions |

|

1.4.Study Limitations |

|

2.Research Methodology |

|

2.1.Research Approach |

|

2.1.1.Top-Down Method |

|

2.1.2.Bottom-Up Method |

|

2.1.3.Factor Impact Analysis |

|

2.2.Insights & Data Collection Process |

|

2.2.1.Secondary Research |

|

2.2.2.Primary Research |

|

2.3.Data Mining Process |

|

2.3.1.Data Analysis |

|

2.3.2.Data Validation and Revalidation |

|

2.3.3.Data Triangulation |

|

3.Executive Summary |

|

3.1.Major Markets & Segments |

|

3.2.Highest Growing Regions and Respective Countries |

|

3.3.Impact of Growth Drivers & Inhibitors |

|

3.4.Regulatory Overview by Country |

|

4.Board-to-Board Connectors Market, by Type (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

4.1.Pin Headers |

|

4.1.1.Stacked Header |

|

4.1.2.Shrouded Header |

|

4.2.Socket |

|

5.Board-to-Board Connectors Market, by Component (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

5.1.< 1mm |

|

5.2.1mm – 2mm |

|

5.3.> 2mm |

|

6.Board-to-Board Connectors Market, by End-use Industry (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.Telecommunication |

|

6.2.Industrial Automation |

|

6.3.Consumer Electronics |

|

6.4.Healthcare |

|

6.5.Automotive |

|

6.6.Others (Aerospace & Defense, Transportation, Energy & Power) |

|

7.Regional Analysis (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

7.1.Regional Overview |

|

7.2.North America |

|

7.2.1.Regional Trends & Growth Drivers |

|

7.2.2.Barriers & Challenges |

|

7.2.3.Opportunities |

|

7.2.4.Factor Impact Analysis |

|

7.2.5.Technology Trends |

|

7.2.6.North America Board-to-Board Connectors Market, by Type |

|

7.2.7.North America Board-to-Board Connectors Market, by Component |

|

7.2.8.North America Board-to-Board Connectors Market, by End-use |

|

*Similar segmentation will be provided at each regional level |

|

7.3.By Country |

|

7.3.1.US |

|

7.3.1.1.US Board-to-Board Connectors Market, by Type |

|

7.3.1.2.US Board-to-Board Connectors Market, by Component |

|

7.3.1.3.US Board-to-Board Connectors Market, by End-use |

|

7.3.2.Canada |

|

*Similar segmentation will be provided at each country level |

|

7.4.Europe |

|

7.5.APAC |

|

7.6.Latin America |

|

7.7.Middle East & Africa |

|

8.Competitive Landscape |

|

8.1.Overview of the Key Players |

|

8.2.Competitive Ecosystem |

|

8.2.1.Platform Manufacturers |

|

8.2.2.Subsystem Manufacturers |

|

8.2.3.Service Providers |

|

8.2.4.Software Providers |

|

8.3.Company Share Analysis |

|

8.4.Company Benchmarking Matrix |

|

8.4.1.Strategic Overview |

|

8.4.2.Product Innovations |

|

8.5.Start-up Ecosystem |

|

8.6.Strategic Competitive Insights/ Customer Imperatives |

|

8.7.ESG Matrix/ Sustainability Matrix |

|

8.8.Manufacturing Network |

|

8.8.1.Locations |

|

8.8.2.Supply Chain and Logistics |

|

8.8.3.Product Flexibility/Customization |

|

8.8.4.Digital Transformation and Connectivity |

|

8.8.5.Environmental and Regulatory Compliance |

|

8.9.Technology Readiness Level Matrix |

|

8.10.Technology Maturity Curve |

|

8.11.Buying Criteria |

|

9.Company Profiles |

|

9.1.Amphenol Corporation |

|

9.1.1.Company Overview |

|

9.1.2.Company Financials |

|

9.1.3.Product/Service Portfolio |

|

9.1.4.Recent Developments |

|

9.1.5.IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2.TE Connectivity |

|

9.3.Japan Aviation Electronics |

|

9.4.Hirose Electric |

|

9.5.Molex, LLC |

|

10.6.Omron Corporation |

|

10.7.Kyocera |

|

10.8.Harting Technology |

|

10.9.CSConn |

|

10.10.Samtec |

|

10.Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Board-to-Board Connectors Market. In the process, the analysis was also done to estimate the parent market and relevant adjacencies to major the impact of them on the board-to-board connectors Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the board-to-board connectors ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Estimation

A combination of top-down and bottom-up approaches was utilized to estimate the overall size of the board-to-board connectors market. These methods were also employed to estimate the size of various subsegments within the market. The market size estimation methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size estimates, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size estimates.

NA