As per Intent Market Research, the Bioprocess Bags Market was valued at USD 3.1 billion in 2024-e and will surpass USD 5.7 billion by 2030; growing at a CAGR of 10.4% during 2025 - 2030.

The bioprocess bags market is experiencing rapid growth, driven by the increasing demand for single-use technologies in the biopharmaceutical and biotechnology industries. Bioprocess bags, essential for cell culture, biopharmaceutical production, and other critical processes, offer significant advantages over traditional stainless-steel equipment. They reduce the risk of contamination, improve flexibility, and lower operational costs, which makes them highly attractive for biopharmaceutical companies looking to streamline manufacturing and production processes.

With the growing focus on biologics, vaccines, and personalized medicine, the market for bioprocess bags is expected to expand significantly. These bags are used across various stages of biomanufacturing, from cell culture to the final production of therapeutic products. As the demand for high-quality, cost-effective, and scalable solutions increases, bioprocess bags are becoming a vital component in the production of biopharmaceuticals, vaccines, and other biologics, particularly in the rapidly expanding areas of gene therapy and immunotherapy.

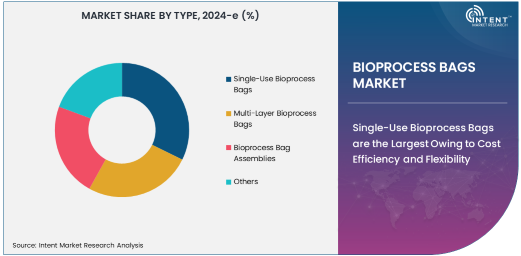

Single-Use Bioprocess Bags are the Largest Owing to Cost Efficiency and Flexibility

Single-use bioprocess bags are the largest subsegment in the market, primarily due to their cost efficiency, ease of use, and scalability. These bags are extensively utilized in cell culture, media preparation, and drug production, offering significant advantages over traditional reusable stainless-steel systems. The ability to discard the bags after each use eliminates the need for cleaning, sterilization, and validation procedures, reducing both time and costs.

The growing trend towards disposable, flexible systems in biomanufacturing has fueled the adoption of single-use bioprocess bags. These bags are integral to the production of biopharmaceuticals, vaccines, and gene therapies, where maintaining sterile conditions and avoiding cross-contamination is crucial. As biopharmaceutical production continues to shift towards single-use solutions for their economic and operational benefits, single-use bioprocess bags are expected to remain the dominant subsegment.

Biopharmaceutical Production is the Largest Owing to the Demand for Biologics

Biopharmaceutical production is the largest application in the bioprocess bags market, driven by the increasing demand for biologic drugs and vaccines. The production of biologics—such as monoclonal antibodies, recombinant proteins, and gene therapies—requires highly controlled environments, where bioprocess bags play a critical role in facilitating sterile, scalable, and flexible manufacturing processes. These bags are used for a variety of purposes, including cell culture, filtration, mixing, and storage.

As the biopharmaceutical industry continues to grow, driven by the expanding pipeline of biologics, bioprocess bags are becoming increasingly essential to ensuring the efficient and cost-effective production of these therapeutic products. The shift toward biologic drugs and the increasing complexity of manufacturing processes make biopharmaceutical production the largest and most significant application in the market.

Pharmaceuticals & Biotechnology is the Largest Owing to Expanding Biologic Production

The pharmaceuticals and biotechnology industry is the largest end-user sector for bioprocess bags, owing to the continuous growth in the production of biologics, vaccines, and therapeutic proteins. The demand for high-quality biopharmaceutical products, including monoclonal antibodies and gene therapies, is driving the need for reliable, sterile, and scalable manufacturing solutions, such as bioprocess bags.

Biopharmaceutical companies are increasingly adopting single-use bioprocessing systems to reduce capital expenditures and enhance operational flexibility. As the global demand for biologic therapies and vaccines continues to rise, pharmaceuticals and biotechnology will remain the largest end-user of bioprocess bags, supporting the market's expansion and innovation in manufacturing processes.

North America is Largest Owing to Strong Biopharmaceutical Industry and R&D Focus

North America is the largest region in the bioprocess bags market, due to the region's dominant position in the biopharmaceutical industry and its focus on research and development (R&D). The U.S., in particular, is home to many leading pharmaceutical and biotechnology companies that drive demand for bioprocessing technologies, including bioprocess bags. The region’s advanced healthcare infrastructure, high levels of investment in biopharmaceuticals, and favorable regulatory environment contribute to North America's leadership in the market.

In addition to biopharmaceutical production, the region’s strong R&D efforts in areas such as gene therapy, immunotherapy, and biologic drug development further propel the adoption of single-use systems like bioprocess bags. As the market continues to expand in North America, it is expected to maintain its dominant position due to continuous innovation, industry growth, and regulatory support.

Leading Companies and Competitive Landscape

The bioprocess bags market is highly competitive, with leading players such as Thermo Fisher Scientific, Sartorius AG, Merck KGaA, and Danaher Corporation providing a wide range of products and solutions for biomanufacturing. These companies offer single-use bioprocess bags, multi-layer bags, and bioprocess bag assemblies that cater to the diverse needs of biopharmaceutical, biotechnology, and healthcare industries.

The competitive landscape is characterized by ongoing innovation and strategic collaborations. Companies are focusing on expanding their product portfolios, improving the functionality of bioprocess bags, and addressing specific market needs, such as enhancing the compatibility of bags with various biopharmaceutical production processes. With the growing demand for biologics, personalized medicine, and gene therapies, companies in the bioprocess bags market are investing heavily in research and development to stay ahead of industry trends and maintain their competitive edge.

Recent Developments:

- In January 2025, Thermo Fisher Scientific expanded its single-use bioprocess bags portfolio to address growing demand in vaccine manufacturing.

- In December 2024, Sartorius Stedim Biotech launched a new multi-layer bioprocess bag system aimed at improving production efficiency in biopharmaceuticals.

- In November 2024, Pall Corporation entered a strategic partnership with a leading biopharmaceutical company to develop customized bioprocessing solutions.

- In October 2024, GE Healthcare announced the acquisition of a bioprocess bag manufacturer to strengthen its position in the bioprocessing market.

- In September 2024, Merck KGaA introduced an innovative bioprocess bag assembly solution designed for large-scale protein purification.

List of Leading Companies:

- Thermo Fisher Scientific

- Sartorius Stedim Biotech

- GE Healthcare

- Merck KGaA

- Lonza Group

- Pall Corporation

- Danaher Corporation

- W. L. Gore & Associates

- Saint-Gobain Performance Plastics

- Entegris, Inc.

- Meissner Filtration Products

- Bio-Rad Laboratories

- 3M

- Becton Dickinson and Company

- Kabbage BioTech

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.1 billion |

|

Forecasted Value (2030) |

USD 5.7 billion |

|

CAGR (2025 – 2030) |

10.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Bioprocess Bags Market By Type (Single-Use Bioprocess Bags, Multi-Layer Bioprocess Bags, Bioprocess Bag Assemblies), By Application (Cell Culture, Biopharmaceutical Production, Drug Discovery & Development, Protein Purification, Vaccine Production), By End-Use Industry (Pharmaceuticals & Biotechnology, Healthcare, Food & Beverages, Chemical & Cosmetics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Thermo Fisher Scientific, Sartorius Stedim Biotech, GE Healthcare, Merck KGaA, Lonza Group, Pall Corporation, Danaher Corporation, W. L. Gore & Associates, Saint-Gobain Performance Plastics, Entegris, Inc., Meissner Filtration Products, Bio-Rad Laboratories, 3M, Becton Dickinson and Company, Kabbage BioTech |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Bioprocess Bags Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Single-Use Bioprocess Bags |

|

4.2. Multi-Layer Bioprocess Bags |

|

4.3. Bioprocess Bag Assemblies |

|

4.4. Others |

|

5. Bioprocess Bags Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Cell Culture |

|

5.2. Biopharmaceutical Production |

|

5.3. Drug Discovery & Development |

|

5.4. Protein Purification |

|

5.5. Vaccine Production |

|

6. Bioprocess Bags Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Pharmaceuticals & Biotechnology |

|

6.2. Healthcare |

|

6.3. Food & Beverages |

|

6.4. Chemical & Cosmetics |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Bioprocess Bags Market, by Type |

|

7.2.7. North America Bioprocess Bags Market, by Application |

|

7.2.8. North America Bioprocess Bags Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Bioprocess Bags Market, by Type |

|

7.2.9.1.2. US Bioprocess Bags Market, by Application |

|

7.2.9.1.3. US Bioprocess Bags Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Thermo Fisher Scientific |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Sartorius Stedim Biotech |

|

9.3. GE Healthcare |

|

9.4. Merck KGaA |

|

9.5. Lonza Group |

|

9.6. Pall Corporation |

|

9.7. Danaher Corporation |

|

9.8. W. L. Gore & Associates |

|

9.9. Saint-Gobain Performance Plastics |

|

9.10. Entegris, Inc. |

|

9.11. Meissner Filtration Products |

|

9.12. Bio-Rad Laboratories |

|

9.13. 3M |

|

9.14. Becton Dickinson and Company |

|

9.15. Kabbage BioTech |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Bioprocess Bags Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Bioprocess Bags Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Bioprocess Bags Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA