As per Intent Market Research, the Beverage Packaging Market was valued at USD 145.2 billion in 2023 and will surpass USD 209.6 billion by 2030; growing at a CAGR of 5.4% during 2024 - 2030.

The beverage packaging market is a dynamic and rapidly evolving sector that plays a crucial role in the global food and beverage industry. With increasing consumer demand for convenient, sustainable, and innovative packaging solutions, the market is projected to grow significantly in the coming years. Factors such as changing lifestyles, urbanization, and the rising popularity of ready-to-drink beverages are driving the demand for effective packaging solutions that not only preserve product quality but also enhance brand visibility.

As environmental concerns continue to rise, the beverage packaging market is increasingly shifting towards sustainable practices. Companies are focusing on developing eco-friendly materials, reducing packaging waste, and improving recyclability. Innovations such as biodegradable plastics, lightweight materials, and smart packaging technologies are gaining traction. As the industry adapts to these trends, manufacturers are also exploring new avenues for product differentiation, leveraging packaging as a key marketing tool to attract environmentally conscious consumers.

PET Bottles Segment is Largest Owing to Versatility and Cost-effectiveness

The PET (Polyethylene Terephthalate) bottles segment is the largest within the beverage packaging market, owing to their versatility, lightweight nature, and cost-effectiveness. PET bottles are widely used for packaging various beverages, including soft drinks, water, juices, and alcoholic beverages. Their superior barrier properties help preserve the freshness and quality of the contents, making them a preferred choice for manufacturers and consumers alike. Additionally, PET bottles are fully recyclable, aligning with the growing emphasis on sustainability in the beverage industry.

The ability of PET bottles to be molded into various shapes and sizes further enhances their appeal, allowing brands to create visually striking packaging that stands out on the shelves. With the rise of health-conscious consumers seeking bottled water and functional beverages, the demand for PET bottles is expected to continue to grow. As manufacturers invest in advanced recycling technologies and promote circular economy initiatives, the PET bottles segment is set to maintain its dominance in the beverage packaging market.

Aluminum Cans Segment is Fastest Growing Owing to Lightweight and Recyclability

The aluminum cans segment is the fastest growing in the beverage packaging market, driven by their lightweight nature, recyclability, and ability to maintain product quality. Aluminum cans are increasingly favored for packaging beverages such as soft drinks, energy drinks, and craft beers. Their excellent barrier properties protect against light and oxygen, ensuring the integrity of the beverage inside. Moreover, the global trend toward sustainability is propelling the demand for aluminum cans, as they can be recycled indefinitely without losing quality.

The rapid growth of the craft beer market has also contributed to the rise of aluminum cans, as many small breweries prefer them for their branding opportunities and ease of transportation. The shift from glass bottles to aluminum cans is further supported by changing consumer preferences for convenience and portability. As the beverage industry continues to embrace sustainability, the aluminum cans segment is expected to witness significant growth, contributing to the overall expansion of the beverage packaging market.

Glass Bottles Segment is Largest Owing to Premium Appeal and Sustainability

The glass bottles segment is the largest in the beverage packaging market when it comes to premium beverages, particularly in the wine and spirits categories. Glass bottles are renowned for their ability to preserve the flavor and aroma of beverages, making them the packaging of choice for high-end products. The inert nature of glass ensures that no chemicals leach into the beverage, thus maintaining its quality and safety. Additionally, glass bottles offer an aesthetic appeal that enhances brand image, attracting discerning consumers.

Moreover, the sustainability factor associated with glass packaging cannot be overlooked. Glass is 100% recyclable, and many consumers prefer products packaged in glass due to its eco-friendly reputation. As brands increasingly focus on sustainability, the glass bottles segment is expected to grow steadily, particularly in markets where premium beverages are in high demand. This trend reinforces the significance of glass packaging in the beverage industry, providing both functional and marketing advantages.

Pouches Segment is Fastest Growing Owing to Convenience and Portability

The pouches segment is the fastest growing in the beverage packaging market, primarily due to their convenience and portability. Pouches are increasingly used for packaging ready-to-drink beverages such as smoothies, juices, and alcoholic beverages. Their lightweight and flexible design makes them easy to transport, store, and consume, appealing to the on-the-go lifestyle of modern consumers. Additionally, pouches can be designed with spouts, making them user-friendly for both children and adults.

The rise of the health and wellness trend has also fueled the demand for pouches, as many consumers are looking for convenient ways to enjoy nutritious beverages. Brands are capitalizing on this trend by introducing innovative pouch designs that enhance product visibility and branding. As the consumer preference for convenience continues to grow, the pouches segment is expected to witness robust growth, further shaping the landscape of the beverage packaging market.

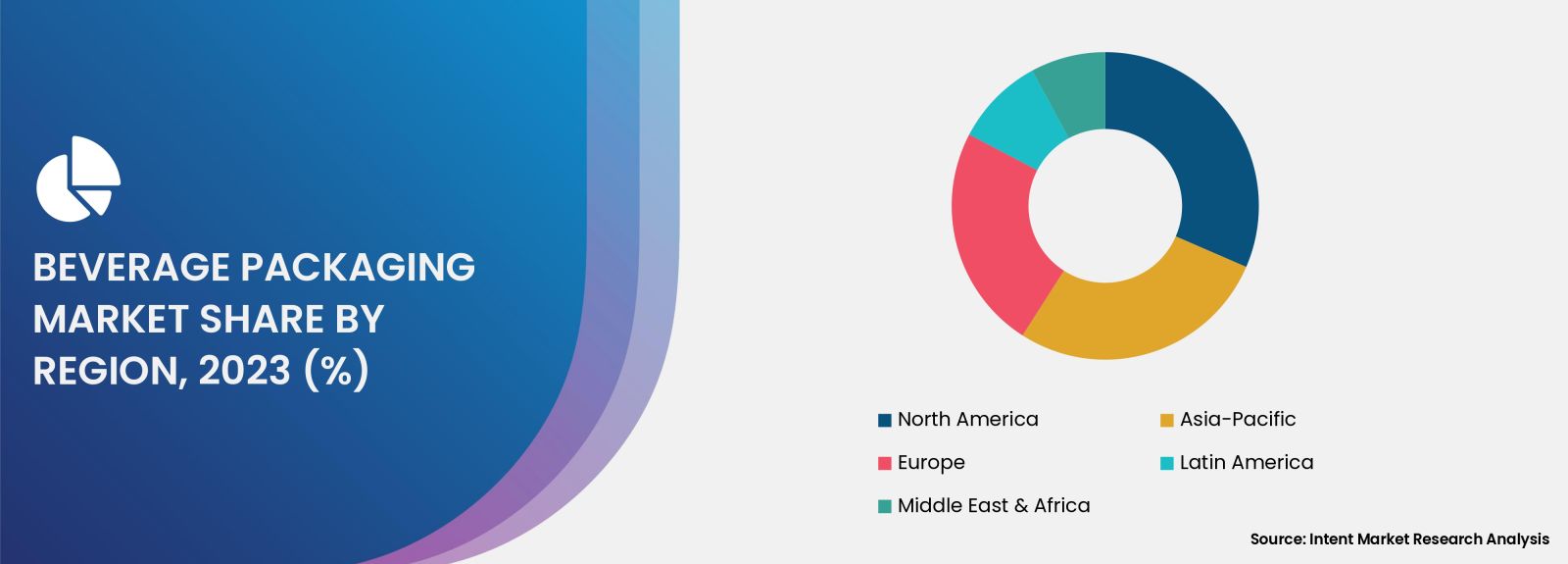

Largest Region: North America is Largest Owing to Strong Demand for Beverage Products

North America is the largest region in the beverage packaging market, driven by strong demand for beverage products and a well-established distribution network. The region is home to several major beverage manufacturers and a diverse consumer base that values innovation and quality. The growth of the ready-to-drink beverage segment, including soft drinks, bottled water, and energy drinks, has significantly contributed to the expansion of the packaging market in this region.

Additionally, the increasing focus on sustainability and environmentally friendly packaging solutions has prompted manufacturers in North America to invest in advanced packaging technologies. With a growing number of consumers seeking eco-conscious products, companies are adapting their packaging strategies to meet these demands. The North American beverage packaging market is expected to continue its growth trajectory, supported by trends such as health consciousness, convenience, and sustainability.

Competitive Landscape of Leading Companies

The competitive landscape of the beverage packaging market is marked by the presence of several key players that are actively driving innovation and expanding their product offerings. Some of the top companies in this market include:

- Amcor plc: A global leader in packaging solutions, Amcor offers a wide range of sustainable packaging products for the beverage industry, including flexible and rigid packaging options.

- Ball Corporation: Known for its aluminum can manufacturing, Ball Corporation provides innovative packaging solutions and is committed to sustainability through its recycling initiatives.

- Crown Holdings, Inc.: A prominent player in metal packaging, Crown Holdings specializes in aluminum and steel cans for beverages, focusing on quality and design.

- Tetra Pak: Renowned for its aseptic packaging solutions, Tetra Pak provides sustainable packaging options for liquid foods and beverages, promoting environmental responsibility.

- Owens-Illinois, Inc.: A leading manufacturer of glass containers, Owens-Illinois produces glass bottles for various beverage segments, emphasizing quality and sustainability.

- Sealed Air Corporation: Specializing in protective and food packaging, Sealed Air offers innovative solutions for the beverage industry, focusing on sustainability and efficiency.

- Berry Global Group, Inc.: A major player in flexible and rigid packaging, Berry Global provides sustainable packaging solutions for beverages, including pouches and bottles.

- Alpha Packaging: A manufacturer of plastic containers and bottles, Alpha Packaging focuses on delivering customized packaging solutions for the beverage sector.

- Graham Packaging Company: Known for its sustainable plastic packaging, Graham Packaging produces containers for various beverages, emphasizing eco-friendly practices.

- Kraft Heinz Company: While primarily known as a food and beverage company, Kraft Heinz is also involved in innovative packaging solutions, contributing to the beverage packaging market.

The competitive landscape in the beverage packaging market is characterized by ongoing innovation, mergers, and acquisitions as companies strive to enhance their market presence. With a growing emphasis on sustainability and consumer preferences for convenience, leading manufacturers are investing in research and development to create packaging solutions that align with current trends. The dynamic nature of this market positions these companies to capitalize on emerging opportunities and drive future growth in the beverage packaging sector.

Report Objectives:

The report will help you answer some of the most critical questions in the Beverage Packaging Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the Beverage Packaging Market?

- What is the size of the Beverage Packaging Market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 145.2 billion |

|

Forecasted Value (2030) |

USD 209.6 billion |

|

CAGR (2024 – 2030) |

5.4% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Beverage Packaging Market By Packaging Type (Bottle, Can, Carton, Pouch), By Material Type (Metal, Plastic, Glass, Paper & Paperboard), By Product Type (Non-Alcoholic Beverages, Alcoholic Beverages, Dairy Beverages) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3.Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Beverage Packaging Market, by Packaging Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Bottle |

|

4.2. Can |

|

4.3. Carton |

|

4.4. Pouch |

|

4.5. Others |

|

5. Beverage Packaging Market, by Material Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Metal |

|

5.2. Plastic |

|

5.3. Glass |

|

5.4. Paper & Paperboard |

|

5.5. Others |

|

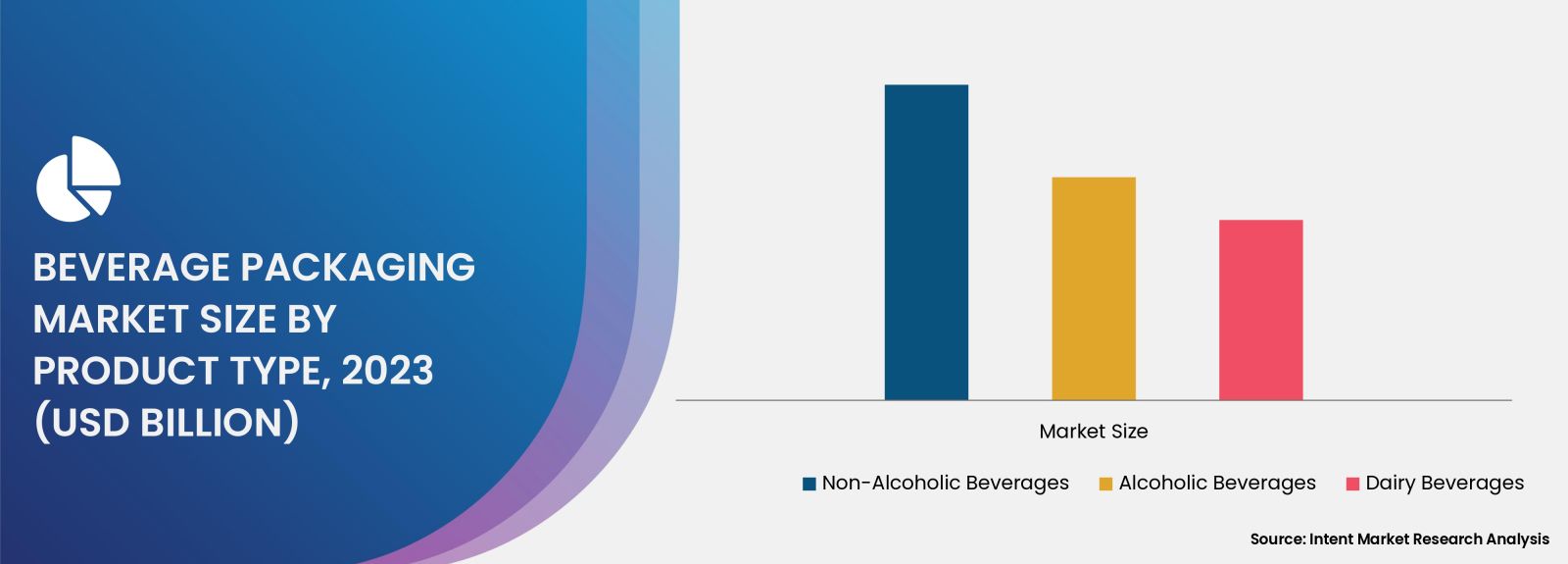

6. Beverage Packaging Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Non-Alcoholic Beverages |

|

6.2. Alcoholic Beverages |

|

6.3. Dairy Beverages |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Beverage Packaging Market, by Packaging Type |

|

7.2.7. North America Beverage Packaging Market, by Material Type |

|

7.2.8. North America Beverage Packaging Market, by Product Type |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Beverage Packaging Market, by Packaging Type |

|

7.2.9.1.2. US Beverage Packaging Market, by Material Type |

|

7.2.9.1.3. US Beverage Packaging Market, by Product Type |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Amcor plc |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. O-I Glass |

|

9.3. Crown Holdings, Inc. |

|

9.4. Ardagh Group S.A. |

|

9.5. Verallia |

|

9.6. Tetra Pak Group |

|

9.7. Ball Corporation |

|

9.8. Vidrala |

|

9.9. Toyo Seikan Group Holdings, Ltd. |

|

9.10. CPMC Holdings Limited |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Beverage Packaging Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Beverage Packaging Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the Beverage Packaging ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Beverage Packaging Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA