As per Intent Market Research, the Automotive Transmission Systems Market was valued at USD 36.1 billion in 2023 and will surpass USD 51.8 billion by 2030; growing at a CAGR of 5.3% during 2024 - 2030.

The automotive transmission systems market plays a pivotal role in the overall performance and efficiency of vehicles. Transmission systems, which include key components such as gearboxes, clutch systems, and torque converters, are essential for the smooth transfer of power from the engine to the wheels. As vehicles evolve to meet consumer demands for enhanced driving experiences, fuel efficiency, and performance, the transmission systems market continues to advance. Technological innovations such as dual-clutch and continuously variable transmissions (CVT) are becoming more prevalent, further shaping the direction of the market.

The demand for advanced transmission systems is also driven by the increasing popularity of electric vehicles (EVs), where unique transmission requirements necessitate the development of specialized systems. As automakers look to improve vehicle efficiency, reduce emissions, and provide better driving comfort, the transmission systems market is witnessing significant growth. The need for improved performance, combined with ongoing advancements in automation, further propels market growth, particularly in regions with high automotive production and adoption of electric mobility.

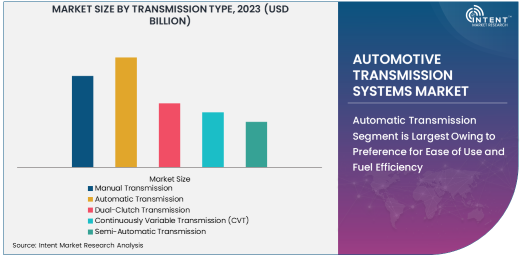

Automatic Transmission Segment is Largest Owing to Preference for Ease of Use and Fuel Efficiency

The automatic transmission segment dominates the automotive transmission systems market due to its widespread adoption in both passenger and commercial vehicles. Automatic transmissions are increasingly preferred for their ease of use, providing drivers with a more comfortable and convenient driving experience. Unlike manual transmissions, automatic systems shift gears without driver input, reducing the need for constant gear changes. This ease of use has made automatic transmissions a standard feature in modern vehicles, particularly in regions like North America and Europe.

In addition to convenience, automatic transmissions also offer improved fuel efficiency, especially with the introduction of more advanced systems such as continuously variable transmissions (CVTs) and dual-clutch transmissions (DCT). These systems provide smoother transitions between gears, reducing fuel consumption and enhancing performance. The dominance of automatic transmissions in the market is expected to continue, as consumers increasingly prioritize comfort and efficiency in their vehicles.

Electric Vehicles Segment is Fastest Growing Due to the Shift Toward Sustainable Mobility

The electric vehicle (EV) segment is the fastest-growing in the automotive transmission systems market, driven by the global transition towards sustainable mobility. While traditional vehicles rely on complex multi-speed transmissions, electric vehicles typically use simpler transmission systems. However, as the EV market expands, there is a growing demand for specialized transmission systems tailored to electric drivetrains. These systems, often single-speed or optimized for electric power delivery, are designed to enhance the performance and efficiency of electric vehicles.

The rapid growth of the electric vehicle market is supported by government incentives, stricter emissions regulations, and increasing consumer demand for environmentally friendly transportation options. As automakers continue to invest in electric mobility and improve EV performance, the need for advanced transmission systems, including those designed specifically for EVs, is expected to drive the segment's growth. This trend makes the electric vehicle segment a key area of opportunity within the automotive transmission systems market.

Gearbox Segment is Largest Due to Core Role in Power Transmission and Performance

The gearbox segment is the largest in the automotive transmission systems market, as gearboxes are critical components in virtually all types of transmission systems. Whether manual, automatic, or semi-automatic, gearboxes are responsible for managing the gear ratios that transfer power from the engine to the wheels. The versatility of gearboxes, which can be tailored to meet the requirements of different vehicle types and transmission systems, has solidified their position as the largest segment in the market.

Gearboxes are designed to handle various loads and power demands, ensuring that vehicles operate efficiently across a range of driving conditions. The increasing demand for high-performance vehicles, along with the adoption of advanced transmission technologies such as dual-clutch and continuously variable transmissions, has further bolstered the need for specialized gearboxes. As automakers continue to innovate and enhance vehicle performance, the gearbox segment will remain at the forefront of the automotive transmission systems market.

OEMs Sales Channel is Largest Due to High Production Volumes and Integration with New Vehicles

The OEMs (Original Equipment Manufacturers) sales channel is the largest in the automotive transmission systems market, driven by the high volumes of transmission systems required for new vehicle production. OEMs provide transmission systems as integral components in the design and assembly of vehicles, ensuring that the systems are tailored to meet the performance and durability standards of the automaker. This channel benefits from the continuous production of new vehicles, including the increasing adoption of electric vehicles and advanced transmission systems.

OEMs also have a significant advantage in terms of product integration, as transmission systems must be customized to fit the specific requirements of different vehicle types and models. The dominance of OEMs in the market is expected to continue, supported by the growing demand for both traditional and advanced transmission systems. With the automotive industry increasingly focusing on performance, fuel efficiency, and comfort, the OEMs sales channel will remain the leading segment in the automotive transmission systems market.

Passenger Vehicles Segment is Largest Due to Demand for Advanced Transmission Systems

The passenger vehicles segment is the largest in the automotive transmission systems market, driven by the increasing demand for advanced transmission systems in personal vehicles. As consumers prioritize comfort, performance, and fuel efficiency, the need for automatic and semi-automatic transmission systems in passenger vehicles has grown. These systems, which offer smoother shifting and better fuel economy, have become standard in many modern vehicles, contributing to the growth of the passenger vehicles segment.

The shift towards electric and hybrid vehicles, which often require unique transmission systems to optimize power delivery and efficiency, is also boosting demand in this segment. As automakers continue to innovate and improve the driving experience, passenger vehicles will remain the dominant sector in the automotive transmission systems market, with an ongoing emphasis on the development of advanced transmission technologies.

Asia-Pacific Region is Fastest Growing Due to Rising Automotive Production and EV Adoption

The Asia-Pacific region is the fastest-growing market for automotive transmission systems, driven by the rapid growth of automotive production and the increasing adoption of electric vehicles (EVs). Countries like China, Japan, and India are major automotive manufacturing hubs, with significant investments in both traditional and electric vehicle production. The demand for advanced transmission systems in this region is rising as automakers focus on improving vehicle efficiency and performance to meet consumer preferences.

The Asia-Pacific region is also at the forefront of the global transition to electric mobility, with China leading the way in EV adoption. As the demand for electric vehicles continues to grow, the need for specialized transmission systems that optimize power delivery and improve overall vehicle performance is increasing. With a burgeoning automotive industry and a strong push for EVs, the Asia-Pacific region is poised for significant growth in the automotive transmission systems market.

Competitive Landscape and Leading Companies

The automotive transmission systems market is highly competitive, with several major players leading the industry. Prominent companies include ZF Friedrichshafen AG, BorgWarner Inc., Aisin Seiki Co., Ltd., and Eaton Corporation, which are focused on developing cutting-edge transmission technologies that enhance vehicle performance, fuel efficiency, and sustainability. These companies are investing heavily in R&D to introduce innovative solutions, such as dual-clutch transmissions (DCT), continuously variable transmissions (CVT), and electric vehicle-specific transmissions.

The competitive landscape is characterized by ongoing technological advancements, strategic partnerships, and acquisitions, as companies seek to strengthen their product portfolios and expand their market presence. As the automotive industry shifts towards electric mobility and more efficient transmission systems, the market will continue to evolve, with companies aiming to meet the demands of both traditional vehicles and the growing EV market. This dynamic environment ensures that the competitive landscape in the automotive transmission systems market will remain vibrant and innovative.

Recent Developments:

- In November 2024, ZF Friedrichshafen AG launched a new generation of transmission systems optimized for hybrid vehicles, enhancing fuel efficiency.

- In October 2024, Aisin Seiki Co., Ltd. introduced an advanced dual-clutch transmission system for high-performance passenger vehicles.

- In September 2024, BorgWarner Inc. announced a new transmission system for electric vehicles, offering a more compact design with improved energy efficiency.

- In August 2024, Jatco Ltd. unveiled its next-gen continuously variable transmission (CVT) system, designed for both passenger and electric vehicles.

- In July 2024, Eaton Corporation expanded its transmission systems portfolio with an automated manual transmission system for commercial vehicles.

List of Leading Companies:

- ZF Friedrichshafen AG

- Aisin Seiki Co., Ltd.

- BorgWarner Inc.

- Jatco Ltd.

- Hyundai Dymos Inc.

- Eaton Corporation

- Getrag Transmission GmbH (Magna International)

- Allison Transmission Inc.

- Schaeffler Technologies AG & Co. KG

- Valeo S.A.

- Delphi Technologies (BorgWarner)

- GKN Automotive

- Ricardo plc

- TREMEC S.A.

- Meritor, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 36.1 billion |

|

Forecasted Value (2030) |

USD 51.8 billion |

|

CAGR (2024 – 2030) |

5.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Automotive Transmission Systems Market By Transmission Type (Manual Transmission, Automatic Transmission, Dual-Clutch Transmission, Continuously Variable Transmission (CVT), Semi-Automatic Transmission), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Heavy-Duty Vehicles), By Transmission Components (Gearbox, Transmission Pump, Clutch System, Torque Converter), By End-Use (OEMs (Original Equipment Manufacturers), Aftermarket), By Sales Channel (Direct Sales, Distributors and Dealers, Online Sales) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ZF Friedrichshafen AG, Aisin Seiki Co., Ltd., BorgWarner Inc., Jatco Ltd., Hyundai Dymos Inc., Eaton Corporation, Getrag Transmission GmbH (Magna International), Allison Transmission Inc., Schaeffler Technologies AG & Co. KG, Valeo S.A., Delphi Technologies (BorgWarner), GKN Automotive, Ricardo plc, TREMEC S.A., Meritor, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Automotive Transmission Systems Market, by Transmission Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Manual Transmission |

|

4.2. Automatic Transmission |

|

4.3. Dual-Clutch Transmission |

|

4.4. Continuously Variable Transmission (CVT) |

|

4.5. Semi-Automatic Transmission |

|

5. Automotive Transmission Systems Market, by Vehicle Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Passenger Vehicles |

|

5.2. Commercial Vehicles |

|

5.3. Electric Vehicles |

|

5.4. Heavy-Duty Vehicles |

|

6. Automotive Transmission Systems Market, by Transmission Components (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Gearbox |

|

6.2. Transmission Pump |

|

6.3. Clutch System |

|

6.4. Torque Converter |

|

6.5. Others |

|

7. Automotive Transmission Systems Market, by End-Use (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. OEMs (Original Equipment Manufacturers) |

|

7.2. Aftermarket |

|

7.3. Others |

|

8. Automotive Transmission Systems Market, by Sales Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Direct Sales |

|

8.2. Distributors and Dealers |

|

8.3. Online Sales |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Automotive Transmission Systems Market, by Transmission Type |

|

9.2.7. North America Automotive Transmission Systems Market, by Vehicle Type |

|

9.2.8. North America Automotive Transmission Systems Market, by Transmission Components |

|

9.2.9. North America Automotive Transmission Systems Market, by End-Use |

|

9.2.10. North America Automotive Transmission Systems Market, by Sales Channel |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Automotive Transmission Systems Market, by Transmission Type |

|

9.2.11.1.2. US Automotive Transmission Systems Market, by Vehicle Type |

|

9.2.11.1.3. US Automotive Transmission Systems Market, by Transmission Components |

|

9.2.11.1.4. US Automotive Transmission Systems Market, by End-Use |

|

9.2.11.1.5. US Automotive Transmission Systems Market, by Sales Channel |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. ZF Friedrichshafen AG |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Aisin Seiki Co., Ltd. |

|

11.3. BorgWarner Inc. |

|

11.4. Jatco Ltd. |

|

11.5. Hyundai Dymos Inc. |

|

11.6. Eaton Corporation |

|

11.7. Getrag Transmission GmbH (Magna International) |

|

11.8. Allison Transmission Inc. |

|

11.9. Schaeffler Technologies AG & Co. KG |

|

11.10. Valeo S.A. |

|

11.11. Delphi Technologies (BorgWarner) |

|

11.12. GKN Automotive |

|

11.13. Ricardo plc |

|

11.14. TREMEC S.A. |

|

11.15. Meritor, Inc. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Automotive Transmission Systems Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Automotive Transmission Systems Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Automotive Transmission Systems Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA