As per Intent Market Research, the Automotive Tappet Market was valued at USD 3.2 billion in 2023 and will surpass USD 4.6 billion by 2030; growing at a CAGR of 5.2% during 2024 - 2030.

The automotive tappet market is integral to the performance of internal combustion engines, primarily by ensuring precise control of the engine’s valve timing. Tappets, also known as cam followers, are critical components in engine valve mechanisms, responsible for transferring motion from the camshaft to the engine valves. These components help in managing the opening and closing of the engine valves at the correct times, which optimizes engine performance, fuel efficiency, and emissions. As engine technologies evolve, the demand for high-performance tappets is also rising, driven by stricter emissions standards and the need for improved fuel efficiency.

The automotive tappet market is influenced by factors such as the rise in vehicle production, especially in emerging markets, and the growing demand for fuel-efficient engines. As the automotive industry shifts towards hybrid and electric vehicles, there is also a growing focus on reducing engine weight and improving durability. This has prompted manufacturers to develop tappets with enhanced materials and innovative designs to meet the specific needs of modern engine technologies, which include more compact and efficient designs in both gasoline and diesel engines.

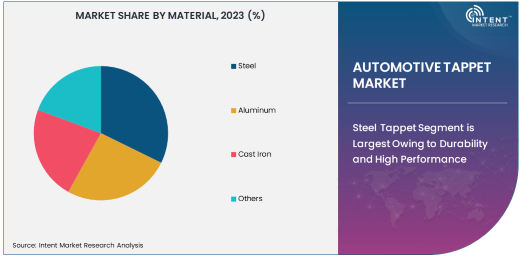

Steel Tappet Segment is Largest Owing to Durability and High Performance

The steel tappet segment is the largest in the automotive tappet market, owing to its durability, high performance, and cost-effectiveness. Steel tappets are widely used in both gasoline and diesel engines because of their superior strength and resistance to wear, which ensures long-lasting performance even under high temperatures and extreme pressure conditions. This makes steel tappets the preferred choice for a wide range of engine types, particularly in OEM applications.

Steel is also highly customizable in terms of manufacturing and design, enabling engineers to optimize tappet designs for specific engine configurations. Additionally, the material is suitable for high-load applications, such as in diesel engines, which typically experience more stress than gasoline engines. The durability of steel tappets contributes to the overall reliability of the engine, making them a key component in both performance and standard vehicle engines. The high demand for steel tappets is expected to continue as automakers focus on improving engine longevity and efficiency.

Hydraulic Tappet Segment is Fastest Growing Due to Enhanced Engine Efficiency and Performance

The hydraulic tappet segment is the fastest growing in the automotive tappet market, driven by the increasing demand for enhanced engine efficiency and performance. Hydraulic tappets, unlike mechanical tappets, use hydraulic pressure to automatically adjust the valve clearances, offering a more refined and efficient operation. This technology reduces the need for manual adjustments and minimizes the noise typically associated with valve mechanisms, contributing to quieter and smoother engine performance.

The growing popularity of hydraulic tappets is linked to their ability to improve engine efficiency by reducing friction and wear, which is particularly important in modern engines designed for lower emissions and better fuel economy. As vehicle manufacturers adopt advanced engine designs to meet stricter emissions standards, hydraulic tappets are gaining traction due to their superior adjustability and precision. Their widespread use in both gasoline and diesel engines, especially in newer, high-performance models, makes this segment one of the fastest-growing in the market.

OEMs Sales Channel is Largest Due to Integration in New Vehicle Production

The OEMs (Original Equipment Manufacturers) sales channel is the largest in the automotive tappet market, driven by the need for tappets as integral components in new vehicle engines. OEMs play a crucial role in the market as they incorporate tappets into the design and production of engines for a wide variety of vehicles. The demand for tappets from OEMs is driven by the continuous advancement of engine technologies, with automakers looking to meet performance, fuel efficiency, and emission standards.

OEMs benefit from designing and manufacturing tappets that align with specific engine types and performance requirements, ensuring that these components meet the necessary durability and efficiency standards. The ongoing production of gasoline, diesel, and hybrid vehicles continues to drive the demand for tappets from OEMs, positioning this sales channel as the primary contributor to the market's growth.

Gasoline Engine Segment is Largest Due to Widespread Use in Passenger Vehicles

The gasoline engine segment is the largest in the automotive tappet market, owing to the widespread use of gasoline-powered engines in passenger vehicles. Gasoline engines are the most commonly used engine type across global markets, particularly in developed regions, where they power the majority of light-duty vehicles. The popularity of gasoline engines is fueled by their reliability, performance, and relatively lower cost compared to diesel engines.

As the automotive industry focuses on improving the fuel efficiency and performance of gasoline engines, the demand for tappets designed to optimize valve timing and reduce wear is increasing. The adoption of technologies such as turbocharging and variable valve timing (VVT) also contributes to the growing need for advanced tappet designs. The gasoline engine segment is expected to remain the largest in the automotive tappet market as it continues to dominate the passenger vehicle market.

Asia-Pacific Region is Fastest Growing Due to Growing Automotive Production and Vehicle Demand

The Asia-Pacific region is the fastest-growing market for automotive tappets, driven by the rapid expansion of automotive production and increasing vehicle demand, particularly in emerging economies like China and India. This region is home to some of the largest automotive manufacturing hubs, with both global automakers and local manufacturers increasing their production capabilities to meet the growing demand for vehicles.

As vehicle production in Asia-Pacific continues to rise, so does the need for components such as tappets, which are essential in optimizing engine performance and efficiency. The region's focus on manufacturing fuel-efficient and high-performance engines, coupled with the increasing adoption of hybrid vehicles, further fuels the growth of the tappet market. The demand for both gasoline and diesel engines in this region, along with the growing automotive industry, positions Asia-Pacific as a key growth area for the automotive tappet market.

Competitive Landscape and Leading Companies

The automotive tappet market is highly competitive, with several leading players focusing on innovation and product development to meet the evolving needs of the automotive industry. Companies such as Federal-Mogul (a part of Tenneco), Schaeffler, and NSK are key players in the market, offering a wide range of tappet products designed to enhance engine performance and durability. These companies are focused on improving tappet technology, developing products that optimize fuel efficiency, reduce emissions, and meet stricter environmental regulations.

The competitive landscape is characterized by ongoing research and development efforts to create more efficient and reliable tappets that can withstand the demands of modern engines. As the automotive industry increasingly shifts towards hybrid and electric powertrains, leading companies are also exploring new technologies and materials to maintain the performance and reliability of tappets in these evolving engine types. This focus on innovation ensures that the automotive tappet market will remain dynamic and responsive to the needs of the automotive sector.

Recent Developments:

- In November 2024, Mahle GmbH introduced a new line of hydraulic tappets designed for enhanced engine efficiency and reduced noise levels.

- In October 2024, Federal-Mogul LLC (Tenneco) launched a new roller tappet series that improves fuel efficiency in gasoline engines.

- In September 2024, Schaeffler Technologies AG & Co. KG developed a new line of tappets for hybrid engine applications, optimizing fuel efficiency and emissions.

- In August 2024, Eaton Corporation expanded its tappet manufacturing capabilities with the introduction of a new high-performance hydraulic tappet for diesel engines.

- In July 2024, Aisin Seiki Co., Ltd. announced the release of a lightweight tappet for commercial vehicles, reducing overall engine weight and improving performance.

List of Leading Companies:

- Mahle GmbH

- Federal-Mogul LLC (Tenneco)

- Eaton Corporation

- Schaeffler Technologies AG & Co. KG

- Aisin Seiki Co., Ltd.

- Rocker Arms LLC

- NSK Ltd.

- BorgWarner Inc.

- Delphi Technologies (BorgWarner)

- Rheinmetall Automotive AG

- Hitachi Automotive Systems

- WABCO Vehicle Control Systems

- Metaldyne Performance Group

- Sodecar Components

- GKN Automotive

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.2 billion |

|

Forecasted Value (2030) |

USD 4.6 billion |

|

CAGR (2024 – 2030) |

5.2% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Automotive Tappet Market By Material (Steel, Aluminum, Cast Iron), By Type (Roller Tappet, Flat Tappet, Hydraulic Tappet, Mechanical Tappet), By Engine Type (Gasoline Engines, Diesel Engines, Hybrid Engines), By End-Use (OEMs (Original Equipment Manufacturers), Aftermarket) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Mahle GmbH, Federal-Mogul LLC (Tenneco), Eaton Corporation, Schaeffler Technologies AG & Co. KG, Aisin Seiki Co., Ltd., Rocker Arms LLC, NSK Ltd., BorgWarner Inc., Delphi Technologies (BorgWarner), Rheinmetall Automotive AG, Hitachi Automotive Systems, WABCO Vehicle Control Systems, Metaldyne Performance Group, Sodecar Components, GKN Automotive |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Automotive Tappet Market, by Material (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Steel |

|

4.2. Aluminum |

|

4.3. Cast Iron |

|

4.4. Others |

|

5. Automotive Tappet Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Roller Tappet |

|

5.2. Flat Tappet |

|

5.3. Hydraulic Tappet |

|

5.4. Mechanical Tappet |

|

6. Automotive Tappet Market, by Engine Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Gasoline Engines |

|

6.2. Diesel Engines |

|

6.3. Hybrid Engines |

|

7. Automotive Tappet Market, by End-Use (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. OEMs (Original Equipment Manufacturers) |

|

7.2. Aftermarket |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Automotive Tappet Market, by Material |

|

8.2.7. North America Automotive Tappet Market, by Type |

|

8.2.8. North America Automotive Tappet Market, by Engine Type |

|

8.2.9. North America Automotive Tappet Market, by End-Use |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Automotive Tappet Market, by Material |

|

8.2.10.1.2. US Automotive Tappet Market, by Type |

|

8.2.10.1.3. US Automotive Tappet Market, by Engine Type |

|

8.2.10.1.4. US Automotive Tappet Market, by End-Use |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Mahle GmbH |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Federal-Mogul LLC (Tenneco) |

|

10.3. Eaton Corporation |

|

10.4. Schaeffler Technologies AG & Co. KG |

|

10.5. Aisin Seiki Co., Ltd. |

|

10.6. Rocker Arms LLC |

|

10.7. NSK Ltd. |

|

10.8. BorgWarner Inc. |

|

10.9. Delphi Technologies (BorgWarner) |

|

10.10. Rheinmetall Automotive AG |

|

10.11. Hitachi Automotive Systems |

|

10.12. WABCO Vehicle Control Systems |

|

10.13. Metaldyne Performance Group |

|

10.14. Sodecar Components |

|

10.15. GKN Automotive |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Automotive Tappet Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Automotive Tappet Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Automotive Tappet Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA