As per Intent Market Research, the Automated External Defibrillator Market was valued at USD 1.5 billion in 2024-e and will surpass USD 2.5 billion by 2030; growing at a CAGR of 8.8% during 2025 - 2030.

The automated external defibrillator (AED) market is experiencing robust growth as the demand for life-saving medical devices continues to rise across various sectors. AEDs are portable devices designed to deliver electric shocks to individuals suffering from sudden cardiac arrest (SCA), thereby restoring normal heart rhythm. As the incidence of cardiovascular diseases (CVD) rises globally, the demand for AEDs, especially in public and emergency settings, has surged. The increasing awareness about the importance of immediate treatment for SCA and the growing prevalence of heart conditions are key factors propelling market expansion.

The adoption of AEDs is gaining momentum, not only in hospitals and healthcare facilities but also in public spaces, sports venues, and fitness centers, where prompt access to defibrillation can significantly improve survival rates. The ease of use, quick accessibility, and effective life-saving capabilities of AEDs make them a crucial component of modern emergency response protocols. Technological advancements and regulatory support further contribute to the growth of the AED market, with manufacturers focusing on creating user-friendly, reliable, and cost-effective solutions.

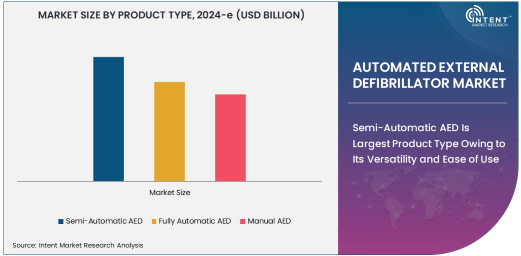

Semi-Automatic AED Is Largest Product Type Owing to Its Versatility and Ease of Use

The semi-automatic AED is the largest product type in the AED market, owing to its versatility and ease of use, particularly in non-medical environments. Semi-automatic AEDs are designed to analyze the heart's rhythm and advise the user when a shock is needed, providing instructions to guide the operator through the defibrillation process. These devices do not deliver a shock automatically; instead, they prompt the user to press a button to administer the shock, allowing for a controlled response in emergency situations.

The semi-automatic AED's widespread adoption can be attributed to its ease of use by laypersons, making it ideal for public access defibrillation (PAD) programs in locations such as schools, shopping malls, and airports. Additionally, semi-automatic AEDs provide a balance between automation and user involvement, offering both effectiveness and safety in situations where professional medical assistance may not be immediately available. As public awareness and initiatives around PAD continue to grow, the semi-automatic AED remains the dominant product type in the market.

Fully Automatic AED Is Fastest Growing Product Type Owing to Its Increased Use in High-Risk Locations

The fully automatic AED is the fastest-growing product type in the market, driven by its ability to deliver shocks without requiring user intervention. These devices are capable of automatically analyzing the patient's heart rhythm and determining the need for a shock, delivering it with no need for the operator to press a button. This automatic feature makes fully automatic AEDs particularly valuable in high-risk environments where immediate action is critical, such as in healthcare settings, sports arenas, and public spaces with high foot traffic.

The fully automatic AED’s ease of use, particularly in high-stress emergency situations, contributes to its growing adoption, especially in locations where a quick, hands-free response is crucial. As the demand for AEDs in public access defibrillation programs and emergency medical services (EMS) grows, the market for fully automatic AEDs is expected to expand rapidly. The increasing focus on minimizing response times and maximizing survival rates in sudden cardiac arrest cases has further fueled the demand for fully automatic devices.

Sudden Cardiac Arrest (SCA) Is Largest Application Owing to High Incidence of Cardiac Arrest Cases

Sudden cardiac arrest (SCA) is the largest application segment in the automated external defibrillator market, driven by the high incidence of cardiac arrest cases globally. SCA occurs when the heart abruptly stops beating, often due to arrhythmia, and is fatal without immediate intervention. AEDs are specifically designed to treat SCA by delivering an electric shock that can restore the heart’s normal rhythm. The effectiveness of defibrillation in the first few minutes of an SCA event is critical to survival, which has led to the widespread adoption of AEDs in emergency medical settings.

The prevalence of cardiovascular diseases, which are a major risk factor for SCA, continues to rise globally, further driving the demand for AEDs. Public health initiatives, such as the placement of AEDs in schools, airports, and other public places, aim to improve survival rates by ensuring that defibrillation is available immediately after an SCA event. As awareness around SCA and the importance of rapid response grows, the market for AEDs in this application is expected to expand significantly.

Cardiovascular Disease Is Fastest Growing Application Owing to Rising Cardiovascular Risk Factors

Cardiovascular disease (CVD) is the fastest-growing application segment in the AED market, fueled by the increasing global prevalence of heart conditions such as heart attacks, arrhythmias, and coronary artery disease. AEDs are increasingly being used as part of the emergency response in healthcare settings to treat patients suffering from acute cardiovascular events, including cardiac arrest due to CVD. The growing risk factors for CVD, including sedentary lifestyles, poor diet, smoking, and diabetes, are contributing to the rise in heart disease and, consequently, the need for AEDs in healthcare facilities.

The increasing incidence of cardiovascular disease, coupled with advancements in cardiac care and emergency response protocols, has driven the demand for AEDs designed to address CVD-related incidents. As healthcare systems prioritize improving emergency response capabilities and patient outcomes, AEDs are becoming an essential tool in treating CVD-related cardiac arrest, particularly in hospitals, cardiac clinics, and ambulatory care centers.

Public Access Defibrillation (PAD) Is Fastest Growing End-User Industry Owing to Increased Awareness and Training Programs

Public Access Defibrillation (PAD) is the fastest growing end-user industry in the AED market, fueled by increased awareness of sudden cardiac arrest and the growing implementation of PAD programs in public spaces. PAD programs aim to equip public areas such as schools, airports, shopping malls, and sports facilities with AEDs, allowing for rapid response in the event of an SCA. Public health campaigns and training programs have raised awareness about the importance of immediate defibrillation, encouraging the installation of AEDs in public areas and promoting bystander intervention.

The growing adoption of PAD programs is also supported by the increased availability of semi-automatic and fully automatic AEDs, which are user-friendly and designed for use by non-medical personnel. The ease of use, combined with initiatives to train the public in CPR and defibrillation techniques, has driven the growth of AED usage in public spaces, contributing to improved survival rates from SCA. This trend is expected to continue as governments, healthcare organizations, and non-profit organizations collaborate to expand the reach of PAD programs worldwide.

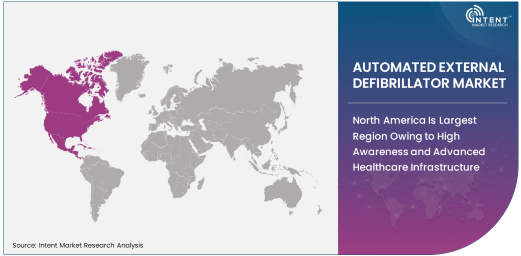

North America Is Largest Region Owing to High Awareness and Advanced Healthcare Infrastructure

North America is the largest region in the AED market, driven by high awareness levels regarding the importance of early defibrillation and the region’s advanced healthcare infrastructure. The United States, in particular, has been a leader in the adoption of AEDs, with widespread placement of these devices in public spaces, hospitals, and emergency medical services (EMS). Public health initiatives, along with legislation requiring the availability of AEDs in public access locations, have contributed to the region’s dominance in the market.

The well-established healthcare systems in North America, combined with government support for initiatives aimed at improving survival rates from sudden cardiac arrest, further bolster the demand for AEDs. As more public spaces and private institutions install AEDs and train personnel in their use, North America remains a key market for AEDs, and this trend is expected to continue.

Leading Companies and Competitive Landscape

The automated external defibrillator market is highly competitive, with several key players leading the way in product innovation and market expansion. Leading companies in the market include Zoll Medical Corporation, Physio-Control, Medtronic, Cardiac Science Corporation, and Defibtech, LLC. These companies offer a wide range of AED products, including semi-automatic, fully automatic, and manual devices, catering to different healthcare and emergency needs.

The competitive landscape is characterized by ongoing technological advancements, with manufacturers focusing on improving the ease of use, reliability, and portability of AED devices. Innovations such as voice prompts, real-time feedback, and extended battery life are common features in newer models. Furthermore, the increasing emphasis on public access defibrillation programs and the integration of AEDs into emergency response systems has intensified competition, with companies vying to expand their market presence and improve survival outcomes in sudden cardiac arrest cases.

Recent Developments:

- In December 2024, Philips Healthcare launched an upgraded semi-automatic AED with advanced ECG analysis and faster shock delivery for quicker response times.

- In November 2024, Zoll Medical Corporation announced a new AED model designed for emergency medical services with cloud-based data sharing capabilities.

- In October 2024, Medtronic introduced a new fully automatic AED with improved shock delivery and enhanced portability for public access use.

- In September 2024, Defibtech LLC unveiled a new line of affordable AEDs aimed at increasing adoption in small businesses and non-healthcare settings.

- In August 2024, Physio-Control (Stryker Corporation) launched a comprehensive AED training program aimed at increasing public awareness and improving user confidence in using AED devices.

List of Leading Companies:

- Philips Healthcare

- Zoll Medical Corporation

- Medtronic

- Cardiac Science Corporation

- Physio-Control (Stryker Corporation)

- Schiller AG

- AIVIA Inc.

- Heartsine Technologies

- Defibtech LLC

- Nihon Kohden Corporation

- Opto Circuits India Ltd.

- Spacelabs Healthcare

- GE Healthcare

- Mindray Medical International Limited

- Shenzhen BTL Medical Equipment Co. Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.5 billion |

|

Forecasted Value (2030) |

USD 2.5 billion |

|

CAGR (2025 – 2030) |

8.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Automated External Defibrillator Market By Product Type (Semi-Automatic AED, Fully Automatic AED, Manual AED), By Application (Sudden Cardiac Arrest, Cardiovascular Disease), By End-User Industry (Hospitals, Public Access Defibrillation (PAD), Emergency Medical Services (EMS), Sports & Fitness Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Philips Healthcare, Zoll Medical Corporation, Medtronic, Cardiac Science Corporation, Physio-Control (Stryker Corporation), Schiller AG, AIVIA Inc., Heartsine Technologies, Defibtech LLC, Nihon Kohden Corporation, Opto Circuits India Ltd., Spacelabs Healthcare, GE Healthcare, Mindray Medical International Limited, Shenzhen BTL Medical Equipment Co. Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Automated External Defibrillator Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Semi-Automatic AED |

|

4.2. Fully Automatic AED |

|

4.3. Manual AED |

|

5. Automated External Defibrillator Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Sudden Cardiac Arrest |

|

5.2. Cardiovascular Disease |

|

6. Automated External Defibrillator Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Public Access Defibrillation (PAD) |

|

6.3. Emergency Medical Services (EMS) |

|

6.4. Sports & Fitness Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Automated External Defibrillator Market, by Product Type |

|

7.2.7. North America Automated External Defibrillator Market, by Application |

|

7.2.8. North America Automated External Defibrillator Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Automated External Defibrillator Market, by Product Type |

|

7.2.9.1.2. US Automated External Defibrillator Market, by Application |

|

7.2.9.1.3. US Automated External Defibrillator Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Philips Healthcare |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Zoll Medical Corporation |

|

9.3. Medtronic |

|

9.4. Cardiac Science Corporation |

|

9.5. Physio-Control (Stryker Corporation) |

|

9.6. Schiller AG |

|

9.7. AIVIA Inc. |

|

9.8. Heartsine Technologies |

|

9.9. Defibtech LLC |

|

9.10. Nihon Kohden Corporation |

|

9.11. Opto Circuits India Ltd. |

|

9.12. Spacelabs Healthcare |

|

9.13. GE Healthcare |

|

9.14. Mindray Medical International Limited |

|

9.15. Shenzhen BTL Medical Equipment Co. Ltd. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Automated External Defibrillator Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Automated External Defibrillator Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Automated External Defibrillator Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA