As per Intent Market Research, the Autoimmune Disease Treatment Market was valued at USD 110.2 billion in 2024-e and will surpass USD 150.3 billion by 2030; growing at a CAGR of 5.3% during 2025 - 2030.

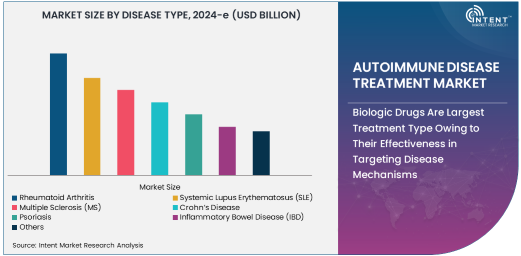

The autoimmune disease treatment market is experiencing significant growth as the prevalence of autoimmune diseases continues to rise globally. Autoimmune diseases, where the body’s immune system mistakenly attacks its own tissues, encompass a wide range of conditions such as rheumatoid arthritis (RA), systemic lupus erythematosus (SLE), multiple sclerosis (MS), and inflammatory bowel disease (IBD). The market for autoimmune disease treatments is driven by advancements in biologic therapies, growing awareness of these conditions, and the increasing availability of targeted treatment options. As research continues to reveal more about the underlying mechanisms of autoimmune diseases, the demand for innovative and effective treatments is rising.

The market is also influenced by the rising aging population and lifestyle factors that contribute to autoimmune conditions. Treatment options for these diseases vary based on disease type and severity, with biologic drugs, disease-modifying anti-rheumatic drugs (DMARDs), and nonsteroidal anti-inflammatory drugs (NSAIDs) being commonly used to manage symptoms and slow disease progression. As the market evolves, there is a growing emphasis on personalized therapies and more effective long-term treatment regimens that can offer improved quality of life for individuals affected by autoimmune diseases.

Biologic Drugs Are Largest Treatment Type Owing to Their Effectiveness in Targeting Disease Mechanisms

Biologic drugs are the largest treatment type in the autoimmune disease treatment market, owing to their ability to specifically target the underlying disease mechanisms. Biologics are a class of drugs derived from living organisms and work by targeting specific components of the immune system that cause inflammation and tissue damage. In diseases such as rheumatoid arthritis, lupus, and multiple sclerosis, biologic drugs have shown significant efficacy in reducing symptoms, slowing disease progression, and improving patient outcomes.

The use of biologics has revolutionized the treatment landscape for autoimmune diseases, offering targeted therapies that are more effective and better tolerated than traditional drugs. These treatments are typically used when other medications fail or when patients experience severe symptoms. With the approval of numerous biologic drugs for different autoimmune diseases, this segment continues to dominate the market, driven by ongoing innovation and the development of new biologics with improved safety profiles and higher efficacy.

Disease-Modifying Anti-Rheumatic Drugs (DMARDs) Are Fastest Growing Treatment Type Owing to Their Role in Disease Control

Disease-modifying anti-rheumatic drugs (DMARDs) are the fastest-growing treatment type in the autoimmune disease treatment market, owing to their critical role in controlling the progression of diseases such as rheumatoid arthritis and lupus. DMARDs work by targeting the immune system to slow the damage caused by autoimmune attacks, preventing further joint damage and improving long-term outcomes. These drugs are considered the cornerstone of treatment for conditions like rheumatoid arthritis, as they can significantly reduce inflammation and preserve joint function over time.

The increasing adoption of DMARDs is driven by their ability to control symptoms and slow disease progression, reducing the need for more invasive treatments such as biologic drugs or corticosteroids. As more DMARDs are developed and approved for various autoimmune diseases, their use is expected to grow, especially as newer formulations with improved safety and efficacy profiles emerge. DMARDs are often prescribed in combination with other medications, enhancing their role in the comprehensive treatment of autoimmune conditions.

Hospitals and Clinics Are Largest End-User Owing to Comprehensive Care and Specialized Treatments

Hospitals and clinics are the largest end-users in the autoimmune disease treatment market, owing to their role in providing comprehensive care and specialized treatments. These healthcare facilities are equipped with medical professionals, including rheumatologists, immunologists, and neurologists, who specialize in diagnosing and treating autoimmune diseases. Hospitals and clinics offer a range of treatment options, including biologic therapies, DMARDs, corticosteroids, and NSAIDs, and provide the necessary monitoring and follow-up care to ensure the effectiveness of treatments.

The centralized nature of care in hospitals and clinics allows for more specialized management of autoimmune diseases, which often require long-term monitoring and tailored treatment regimens. Additionally, hospitals and clinics are the primary locations for patients to receive biologic infusions, which are often required for severe autoimmune conditions. As the demand for personalized and high-quality care increases, hospitals and clinics remain the dominant end-user segment in the autoimmune disease treatment market, providing critical services for managing these chronic conditions.

North America Is Largest Region Owing to Advanced Healthcare Infrastructure and High Adoption of Biologic Drugs

North America is the largest region in the autoimmune disease treatment market, owing to its advanced healthcare infrastructure, high adoption rates of biologic drugs, and strong research capabilities. The United States, in particular, plays a dominant role in the market, with a well-established healthcare system that offers broad access to cutting-edge treatments for autoimmune diseases. The approval and widespread use of biologic drugs in North America have driven the market’s growth, as these treatments are considered the gold standard for managing many autoimmune conditions.

In addition to access to innovative therapies, North America benefits from a high level of awareness and diagnosis of autoimmune diseases, leading to early intervention and better management of these conditions. The region also benefits from extensive government and private sector investment in medical research, leading to the continuous development of new treatments. As the prevalence of autoimmune diseases continues to rise, North America is expected to remain the largest market for autoimmune disease treatments, with ongoing advancements in both biologic therapies and disease management approaches.

Leading Companies and Competitive Landscape

The autoimmune disease treatment market is highly competitive, with several key players dominating the development and distribution of medications for various autoimmune conditions. Leading companies in this market include AbbVie, Johnson & Johnson, Amgen, Roche, and Merck & Co., which have developed a range of biologic drugs, DMARDs, and other treatments for diseases such as rheumatoid arthritis, lupus, and psoriasis. These companies are at the forefront of innovation, with ongoing research and development aimed at improving treatment efficacy and expanding therapeutic options for autoimmune diseases.

The competitive landscape is shaped by the ongoing development of new biologic drugs and DMARDs, as well as the exploration of alternative therapies. As the market for autoimmune disease treatments grows, companies are focusing on improving the safety and efficacy of their products while also addressing issues such as treatment costs and patient access. Strategic collaborations, mergers, and acquisitions are common in this market, as companies seek to expand their product portfolios and enhance their competitive positions. With a strong emphasis on research and development, the autoimmune disease treatment market is expected to continue evolving, with leading companies playing a key role in shaping the future of autoimmune disease management.

Recent Developments:

- In December 2024, AbbVie Inc. received FDA approval for a new biologic drug aimed at treating moderate-to-severe rheumatoid arthritis.

- In November 2024, Johnson & Johnson launched a new immunotherapy treatment for systemic lupus erythematosus, showing promising clinical results.

- In October 2024, Pfizer Inc. announced the acquisition of a biotech company focused on developing next-generation DMARDs for autoimmune diseases.

- In September 2024, Roche Holding AG expanded its biologics portfolio with the release of an advanced monoclonal antibody treatment for Crohn’s disease.

- In August 2024, Amgen Inc. introduced a novel treatment for psoriasis, targeting specific immune cells involved in the disease's pathogenesis.

List of Leading Companies:

- AbbVie Inc.

- Johnson & Johnson

- Roche Holding AG

- Novartis AG

- Pfizer Inc.

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- Eli Lilly and Co.

- Sanofi S.A.

- Amgen Inc.

- AstraZeneca plc

- Gilead Sciences Inc.

- Takeda Pharmaceutical Company

- Celgene Corporation

- Biogen Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 110.2 billion |

|

Forecasted Value (2030) |

USD 150.3 billion |

|

CAGR (2025 – 2030) |

5.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Autoimmune Disease Treatment Market By Disease Type (Rheumatoid Arthritis, Systemic Lupus Erythematosus (SLE), Multiple Sclerosis (MS), Crohn’s Disease, Psoriasis, Inflammatory Bowel Disease (IBD), Hashimoto’s Thyroiditis), By Treatment Type (Biologic Drugs, Disease-Modifying Anti-Rheumatic Drugs (DMARDs), Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Corticosteroids), By End-User (Hospitals and Clinics, Home Care, Specialty Pharmacies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

AbbVie Inc., Johnson & Johnson, Roche Holding AG, Novartis AG, Pfizer Inc., Merck & Co., Inc., Bristol-Myers Squibb Company, Eli Lilly and Co., Sanofi S.A., Amgen Inc., AstraZeneca plc, Gilead Sciences Inc., Takeda Pharmaceutical Company, Celgene Corporation, Biogen Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Autoimmune Disease Treatment Market, by Disease Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Rheumatoid Arthritis |

|

4.2. Systemic Lupus Erythematosus (SLE) |

|

4.3. Multiple Sclerosis (MS) |

|

4.4. Crohn’s Disease |

|

4.5. Psoriasis |

|

4.6. Inflammatory Bowel Disease (IBD) |

|

4.7. Others |

|

5. Autoimmune Disease Treatment Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Biologic Drugs |

|

5.1.1. Monoclonal Antibodies |

|

5.1.2. Tumor Necrosis Factor (TNF) Inhibitors |

|

5.1.3. Interleukin Inhibitors |

|

5.2. Disease-Modifying Anti-Rheumatic Drugs (DMARDs) |

|

5.2.1. Conventional DMARDs |

|

5.2.2. Targeted Synthetic DMARDs |

|

5.3. Nonsteroidal Anti-Inflammatory Drugs (NSAIDs) |

|

5.4. Corticosteroids |

|

5.5. Others |

|

6. Autoimmune Disease Treatment Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals and Clinics |

|

6.2. Home Care |

|

6.3. Specialty Pharmacies |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Autoimmune Disease Treatment Market, by Disease Type |

|

7.2.7. North America Autoimmune Disease Treatment Market, by Treatment Type |

|

7.2.8. North America Autoimmune Disease Treatment Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Autoimmune Disease Treatment Market, by Disease Type |

|

7.2.9.1.2. US Autoimmune Disease Treatment Market, by Treatment Type |

|

7.2.9.1.3. US Autoimmune Disease Treatment Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. AbbVie Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Johnson & Johnson |

|

9.3. Roche Holding AG |

|

9.4. Novartis AG |

|

9.5. Pfizer Inc. |

|

9.6. Merck & Co., Inc. |

|

9.7. Bristol-Myers Squibb Company |

|

9.8. Eli Lilly and Co. |

|

9.9. Sanofi S.A. |

|

9.10. Amgen Inc. |

|

9.11. AstraZeneca plc |

|

9.12. Gilead Sciences Inc. |

|

9.13. Takeda Pharmaceutical Company |

|

9.14. Celgene Corporation |

|

9.15. Biogen Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Autoimmune Disease Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Autoimmune Disease Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Autoimmune Disease Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA