As per Intent Market Research, the Audiology Devices Market was valued at USD 10.1 billion in 2024-e and will surpass USD 15.1 billion by 2030; growing at a CAGR of 7.0% during 2025 - 2030.

The audiology devices market is expanding rapidly, driven by the increasing prevalence of hearing impairments and the growing aging population worldwide. Hearing loss, which affects millions globally, has led to an increasing demand for advanced audiology devices that improve the quality of life for individuals with hearing disabilities. Audiology devices, including hearing aids, cochlear implants, and diagnostic devices, play a critical role in diagnosing and treating various forms of hearing loss, ranging from mild to profound. With continuous advancements in technology, these devices are becoming more sophisticated, offering better sound quality, improved user comfort, and more seamless integration with modern digital environments.

As the awareness of hearing-related health issues increases and technology continues to evolve, the market is witnessing a shift towards more personalized and effective solutions. The demand for both preventive and therapeutic audiology devices has been spurred by healthcare initiatives focused on hearing health, along with the rise in government support and insurance coverage for hearing aids and related treatments. This trend is expected to continue as the global population ages, and innovations in hearing technology provide more efficient solutions for those affected by hearing impairments.

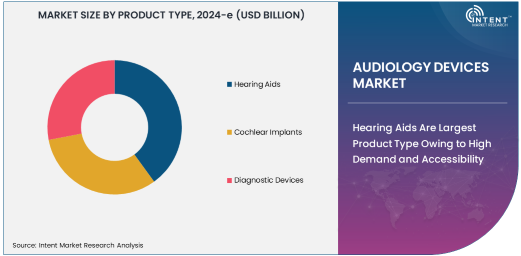

Hearing Aids Are Largest Product Type Owing to High Demand and Accessibility

Hearing aids are the largest product type in the audiology devices market, owing to their widespread usage and affordability compared to other advanced hearing solutions like cochlear implants. As the most common treatment for hearing loss, hearing aids help individuals with mild to severe hearing impairments by amplifying sounds to improve auditory perception. The adoption of digital hearing aids, which offer enhanced sound quality, smaller sizes, and customizable settings, has further boosted the demand for these devices.

Hearing aids remain the go-to solution for the majority of individuals with hearing impairments due to their accessibility, effectiveness, and range of options tailored to various degrees of hearing loss. With ongoing advancements in hearing aid technology, such as Bluetooth connectivity, noise reduction, and rechargeable batteries, the devices have become even more user-friendly. The growing awareness about hearing health, coupled with government subsidies and private insurance coverage for hearing aids, has made these devices more accessible to a broader population, further driving their dominance in the market.

Cochlear Implants Are Fastest Growing Product Type Owing to Advanced Treatment Options

Cochlear implants are the fastest-growing product type in the audiology devices market, owing to their ability to provide a solution for individuals with severe to profound hearing loss who do not benefit from traditional hearing aids. Unlike hearing aids, which amplify sound, cochlear implants work by directly stimulating the auditory nerve, offering a more effective treatment option for those with significant hearing impairments. The growing recognition of cochlear implants as a long-term solution for individuals with severe hearing loss is driving their increased adoption.

The rapid growth of the cochlear implant market is also fueled by advancements in technology, such as improved sound processing capabilities, enhanced speech recognition, and smaller, more discreet designs. As the affordability and availability of cochlear implants increase, the market is seeing greater uptake, particularly in regions with higher healthcare access. With the rise in awareness and acceptance of cochlear implants, especially among the aging population and those affected by congenital hearing loss, this segment is expected to continue growing at a faster pace than other audiology devices.

Hospitals and Clinics Are Largest End-User Owing to Professional Diagnosis and Treatment

Hospitals and clinics are the largest end-users in the audiology devices market, owing to their role in providing professional diagnosis and treatment for hearing loss. These healthcare settings offer a comprehensive range of audiology services, from hearing tests and consultations to the fitting of hearing aids and the implantation of cochlear devices. Hospitals and clinics are equipped with the necessary infrastructure, expertise, and medical staff to provide personalized care for individuals with hearing impairments.

The critical role of hospitals and clinics in diagnosing and managing hearing loss contributes to their dominance in the audiology devices market. In these settings, healthcare providers use advanced diagnostic devices to assess the severity of hearing loss and recommend appropriate treatment options, including hearing aids, cochlear implants, and rehabilitation therapies. Additionally, the presence of rehabilitation centers and audiology specialists in hospitals further supports the demand for audiology devices, making these facilities key players in the market.

North America Is Largest Region Owing to High Healthcare Standards and Adoption Rates

North America is the largest region in the audiology devices market, driven by high healthcare standards, widespread awareness, and significant adoption rates of hearing aids and cochlear implants. The United States, in particular, is a major contributor to the market, with a large population suffering from hearing loss and a robust healthcare system that supports the diagnosis, treatment, and reimbursement of audiology devices. The availability of advanced medical technology, coupled with government initiatives to increase hearing healthcare accessibility, contributes to the region's leadership in the market.

The growing elderly population in North America, which is more susceptible to age-related hearing loss, is also a significant factor in the increasing demand for audiology devices. With continuous advancements in hearing technology and ongoing research into improving the effectiveness and affordability of audiology devices, North America is expected to maintain its dominant position in the global audiology devices market.

Leading Companies and Competitive Landscape

The audiology devices market is highly competitive, with several major companies leading the way in product innovation and market share. Key players in the market include Sonova Holding AG, Cochlear Limited, Starkey Hearing Technologies, Demant A/S, and Amplifon S.p.A., which offer a range of hearing aids, cochlear implants, and diagnostic devices. These companies invest heavily in research and development to improve the performance, design, and user-friendliness of their products, focusing on advancements such as digital processing, wireless connectivity, and improved battery life.

The competitive landscape is also shaped by the increasing availability of over-the-counter hearing aids and direct-to-consumer sales models, which have introduced new dynamics into the market. Companies are focusing on expanding their product portfolios and distribution channels to capture a larger market share, with strategic acquisitions and partnerships being common tactics for growth. As the demand for audiology devices continues to rise, the market will remain highly competitive, with companies striving to differentiate themselves through technological advancements, pricing strategies, and customer service offerings.

Recent Developments:

- In December 2024, Demant A/S launched a new hearing aid with improved speech enhancement technology, aimed at helping users in noisy environments.

- In November 2024, Cochlear Limited introduced an upgraded cochlear implant system that offers improved sound quality and greater ease of use for patients.

- In October 2024, Sonova Holding AG announced a partnership with a leading health tech company to integrate smart hearing aids with digital health monitoring features.

- In September 2024, Starkey Hearing Technologies launched a new line of wireless hearing aids with advanced Bluetooth connectivity and longer battery life.

- In August 2024, GN Store Nord A/S unveiled an innovative rechargeable hearing aid model, providing a more sustainable and cost-effective solution for hearing loss management.

List of Leading Companies:

- Demant A/S

- Cochlear Limited

- Sonova Holding AG

- Starkey Hearing Technologies

- Eargo, Inc.

- GN Store Nord A/S

- Amplifon S.p.A.

- Hoya Corporation

- MED-EL Medical Electronics

- Arphi Electronics

- Knowles Electronics LLC

- Sivantos (now known as Signia)

- Widex A/S

- Rexton, Inc.

- Audina Hearing Instruments, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 10.1 billion |

|

Forecasted Value (2030) |

USD 15.1 billion |

|

CAGR (2025 – 2030) |

7.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Audiology Devices Market By Product Type (Hearing Aids, Cochlear Implants, Diagnostic Devices), By Technology (Digital, Analog), By End-User (Hospitals and Clinics, Homecare, Rehabilitation Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Demant A/S, Cochlear Limited, Sonova Holding AG, Starkey Hearing Technologies, Eargo, Inc., GN Store Nord A/S, Amplifon S.p.A., Hoya Corporation, MED-EL Medical Electronics, Arphi Electronics, Knowles Electronics LLC, Sivantos (now known as Signia), Widex A/S, Rexton, Inc., Audina Hearing Instruments, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Audiology Devices Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Hearing Aids |

|

4.1.1. Behind-the-Ear (BTE) |

|

4.1.2. In-the-Ear (ITE) |

|

4.1.3. Completely-in-Canal (CIC) |

|

4.2. Cochlear Implants |

|

4.3. Diagnostic Devices |

|

4.3.1. Audiometers |

|

4.3.2. Tympanometers |

|

4.4. Others |

|

5. Audiology Devices Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Digital |

|

5.2. Analog |

|

6. Audiology Devices Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals and Clinics |

|

6.2. Homecare |

|

6.3. Rehabilitation Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Audiology Devices Market, by Product Type |

|

7.2.7. North America Audiology Devices Market, by Technology |

|

7.2.8. North America Audiology Devices Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Audiology Devices Market, by Product Type |

|

7.2.9.1.2. US Audiology Devices Market, by Technology |

|

7.2.9.1.3. US Audiology Devices Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Demant A/S |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Cochlear Limited |

|

9.3. Sonova Holding AG |

|

9.4. Starkey Hearing Technologies |

|

9.5. Eargo, Inc. |

|

9.6. GN Store Nord A/S |

|

9.7. Amplifon S.p.A. |

|

9.8. Hoya Corporation |

|

9.9. MED-EL Medical Electronics |

|

9.10. Arphi Electronics |

|

9.11. Knowles Electronics LLC |

|

9.12. Sivantos (now known as Signia) |

|

9.13. Widex A/S |

|

9.14. Rexton, Inc. |

|

9.15. Audina Hearing Instruments, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Audiology Devices Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Audiology Devices Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Audiology Devices Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA