As per Intent Market Research, the Attention Deficit Hyperactivity Disorder Treatment Market was valued at USD 20.1 billion in 2024-e and will surpass USD 30.2 billion by 2030; growing at a CAGR of 7.0% during 2025 - 2030.

The Attention Deficit Hyperactivity Disorder (ADHD) treatment market is experiencing significant growth, driven by the increasing awareness and diagnosis of ADHD, particularly in children, and the growing need for effective treatment options. ADHD is a neurodevelopmental disorder characterized by persistent patterns of inattention, hyperactivity, and impulsivity, which can significantly impair an individual's daily functioning. The market for ADHD treatments encompasses a range of pharmaceutical and non-pharmaceutical interventions, including stimulant and non-stimulant medications, as well as behavioral therapies. The rising recognition of ADHD across different age groups and the advancement of treatment modalities are key factors contributing to the expansion of this market.

As the demand for effective ADHD treatment options increases, so does the availability of a variety of therapies. Pharmaceutical options, such as stimulants and non-stimulants, remain widely used for managing symptoms, while non-pharmaceutical approaches, particularly behavioral therapy, are increasingly integrated into treatment regimens. Additionally, digital health solutions, including telemedicine and online therapy platforms, are expanding the accessibility of ADHD treatments, especially in underserved regions. This multifaceted approach to treatment is expected to continue fueling the market's growth.

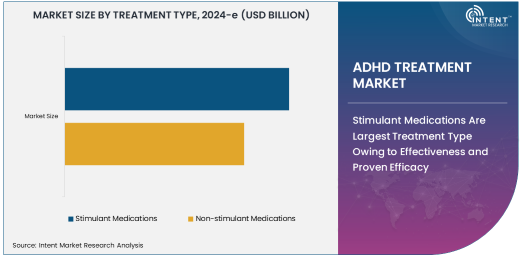

Stimulant Medications Are Largest Treatment Type Owing to Effectiveness and Proven Efficacy

Stimulant medications are the largest treatment type in the ADHD treatment market, owing to their proven efficacy and widespread use. These medications, which include methylphenidate and amphetamines, are considered the first-line treatment for ADHD and are highly effective in reducing symptoms such as inattention, hyperactivity, and impulsivity. Stimulants work by increasing the levels of certain neurotransmitters in the brain, particularly dopamine and norepinephrine, which help regulate attention and behavior. Their effectiveness has been well-documented, making them the preferred choice for healthcare providers treating ADHD.

The dominance of stimulant medications in the market is also supported by their relatively fast-acting nature and their broad availability. Despite potential side effects such as sleep disturbances and appetite changes, stimulant medications remain the most commonly prescribed treatment for both children and adults with ADHD. With ongoing research into improving formulations to minimize side effects and enhance efficacy, the demand for stimulant medications is expected to remain strong in the ADHD treatment market.

Behavioral Therapy Is Fastest Growing Treatment Type Owing to Increasing Focus on Non-Pharmaceutical Approaches

Behavioral therapy is the fastest-growing treatment type in the ADHD treatment market, driven by the increasing focus on non-pharmaceutical interventions. Behavioral therapy, particularly cognitive-behavioral therapy (CBT), helps individuals with ADHD develop strategies for managing symptoms and improving organizational and time management skills. Unlike medications, behavioral therapy does not carry the risk of side effects and can be tailored to address specific challenges faced by individuals with ADHD, including issues related to focus, impulse control, and social interactions.

The growing preference for non-pharmaceutical treatments, particularly among parents of children with ADHD, is fueling the rise in demand for behavioral therapy. Additionally, as more mental health professionals incorporate behavioral therapy into comprehensive treatment plans, this approach is gaining popularity due to its holistic nature and long-term benefits. The integration of digital platforms offering online behavioral therapy sessions further contributes to its rapid growth, making it more accessible to individuals across different age groups.

Children Are Largest End-User Owing to High Prevalence of ADHD in Pediatric Population

Children are the largest end-users in the ADHD treatment market, as ADHD is most commonly diagnosed in childhood. The symptoms of ADHD, which typically appear before the age of 12, can significantly impact a child's academic performance, social relationships, and overall quality of life. As a result, there is a high demand for effective treatments that can help manage symptoms and improve functioning. Stimulant medications and behavioral therapies are commonly used in children, with treatment often starting shortly after diagnosis to help minimize the long-term impact of the disorder.

The large population of children diagnosed with ADHD, coupled with increased awareness among parents and educators, contributes to the continued demand for ADHD treatments in this age group. The availability of a range of treatment options, from medications to behavioral therapies and even digital health solutions, ensures that children with ADHD have access to personalized care that can address their specific needs and challenges.

Hospitals and Clinics Are Largest Distribution Channel Owing to In-Person Diagnosis and Treatment

Hospitals and clinics are the largest distribution channel in the ADHD treatment market, as in-person diagnosis and treatment remain the primary method for managing the disorder. Healthcare providers in these settings play a critical role in diagnosing ADHD and prescribing appropriate treatments, including medications and behavioral therapies. Hospitals and clinics are also key sites for providing comprehensive treatment plans that involve ongoing monitoring of symptoms, adjustments to medication, and coordination with other healthcare professionals such as psychologists and therapists.

The role of hospitals and clinics in the ADHD treatment process is essential, especially for children, as early diagnosis and intervention are critical for successful treatment outcomes. These healthcare settings offer the necessary infrastructure and expertise to deliver a wide range of treatment options, making them the preferred distribution channel for individuals seeking ADHD care. However, the growing availability of online platforms and telehealth services is beginning to complement traditional in-person treatment, expanding access to care for individuals in remote or underserved areas.

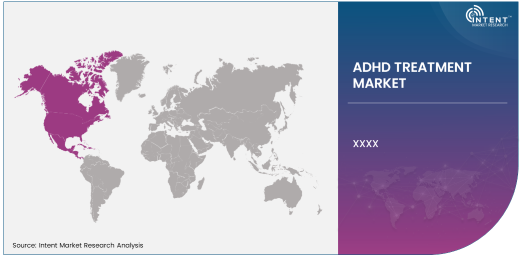

North America Is Largest Region Owing to High Awareness and Advanced Healthcare Infrastructure

North America is the largest region in the ADHD treatment market, driven by high awareness of ADHD, advanced healthcare infrastructure, and widespread access to treatment options. The United States and Canada have well-established healthcare systems and significant resources devoted to the diagnosis and treatment of ADHD, contributing to the region's dominance in the market. The high prevalence of ADHD in children and adults, coupled with strong support for mental health initiatives, has created a favorable environment for the growth of the ADHD treatment market.

In North America, the combination of stimulant medications, behavioral therapy, and digital health solutions provides a comprehensive approach to managing ADHD. Additionally, the availability of healthcare providers specializing in ADHD care ensures that individuals have access to personalized treatment plans. As awareness of ADHD continues to increase, North America is expected to maintain its leading position in the global market for ADHD treatments.

Leading Companies and Competitive Landscape

The ADHD treatment market is highly competitive, with several leading pharmaceutical companies, digital health platforms, and therapy providers vying for market share. Key players include major pharmaceutical companies such as Novartis, Johnson & Johnson, and Eli Lilly, which produce a range of stimulant and non-stimulant medications for ADHD. These companies are focused on innovation, particularly in the development of extended-release formulations and combination therapies that aim to improve treatment adherence and minimize side effects.

In addition to pharmaceutical companies, digital health companies like CogniFit and EndeavorRx are gaining traction in the ADHD treatment space by offering engaging, interactive apps designed to improve attention and cognitive function in individuals with ADHD. These companies leverage advances in gaming technology and behavioral science to provide personalized, user-friendly treatment options. As the market evolves, the competitive landscape will continue to be shaped by ongoing research, technological innovation, and a growing focus on integrated, holistic treatment approaches.

Recent Developments:

- In December 2024, Johnson & Johnson launched a new ADHD medication designed to reduce side effects and improve patient compliance.

- In November 2024, Eli Lilly announced the approval of a new ADHD treatment for children aged 6-12.

- In October 2024, Shire Pharmaceuticals expanded its ADHD medication portfolio with a new extended-release formulation of amphetamines.

- In September 2024, Novartis AG conducted a study on the long-term effects of its ADHD medications in adults, showing positive results.

- In August 2024, Takeda Pharmaceutical Company acquired a startup specializing in ADHD digital therapeutics to enhance its treatment offerings.

List of Leading Companies:

- Johnson & Johnson

- Eli Lilly and Company

- Shire Pharmaceuticals

- Novartis AG

- Takeda Pharmaceutical Company

- Otsuka Pharmaceutical Co. Ltd.

- Neos Therapeutics

- Purdue Pharma

- Amgen Inc.

- Mylan N.V.

- Mallinckrodt Pharmaceuticals

- Sunovion Pharmaceuticals

- Supernus Pharmaceuticals

- Lundbeck A/S

- Medice Arzneimittel Pütter GmbH & Co. KG

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 20.1 billion |

|

Forecasted Value (2030) |

USD 30.2 billion |

|

CAGR (2025 – 2030) |

7.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Attention Deficit Hyperactivity Disorder Treatment Market By Treatment Type (Stimulant Medications, Non-stimulant Medications, Behavioral Therapy), By End-User (Children, Adults), By Distribution Channel (Hospitals and Clinics, Online Platforms, Pharmacies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Johnson & Johnson, Eli Lilly and Company, Shire Pharmaceuticals, Novartis AG, Takeda Pharmaceutical Company, Otsuka Pharmaceutical Co. Ltd., Neos Therapeutics, Purdue Pharma, Amgen Inc., Mylan N.V., Mallinckrodt Pharmaceuticals, Sunovion Pharmaceuticals, Supernus Pharmaceuticals, Lundbeck A/S, Medice Arzneimittel Pütter GmbH & Co. KG |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Attention Deficit Hyperactivity Disorder Treatment Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Stimulant Medications |

|

4.1.1. Methylphenidate |

|

4.1.2. Amphetamines |

|

4.2. Non-stimulant Medications |

|

4.2.1. Atomoxetine |

|

4.2.2. Guanfacine |

|

4.3. Behavioral Therapy |

|

4.3.1. Cognitive Behavioral Therapy (CBT) |

|

4.3.2. Parent Training Programs |

|

4.4. Others |

|

4.4.1. Social Skills Training |

|

5. Attention Deficit Hyperactivity Disorder Treatment Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Children |

|

5.2. Adults |

|

6. Attention Deficit Hyperactivity Disorder Treatment Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals and Clinics |

|

6.2. Online Platforms |

|

6.3. Pharmacies |

|

6.4. Direct-to-Consumer (DTC) |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Attention Deficit Hyperactivity Disorder Treatment Market, by Treatment Type |

|

7.2.7. North America Attention Deficit Hyperactivity Disorder Treatment Market, by End-User |

|

7.2.8. North America Attention Deficit Hyperactivity Disorder Treatment Market, by Distribution Channel |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Attention Deficit Hyperactivity Disorder Treatment Market, by Treatment Type |

|

7.2.9.1.2. US Attention Deficit Hyperactivity Disorder Treatment Market, by End-User |

|

7.2.9.1.3. US Attention Deficit Hyperactivity Disorder Treatment Market, by Distribution Channel |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Johnson & Johnson |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Eli Lilly and Company |

|

9.3. Shire Pharmaceuticals |

|

9.4. Novartis AG |

|

9.5. Takeda Pharmaceutical Company |

|

9.6. Otsuka Pharmaceutical Co. Ltd. |

|

9.7. Neos Therapeutics |

|

9.8. Purdue Pharma |

|

9.9. Amgen Inc. |

|

9.10. Mylan N.V. |

|

9.11. Mallinckrodt Pharmaceuticals |

|

9.12. Sunovion Pharmaceuticals |

|

9.13. Supernus Pharmaceuticals |

|

9.14. Lundbeck A/S |

|

9.15. Medice Arzneimittel Pütter GmbH & Co. KG |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Attention Deficit Hyperactivity Disorder Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Attention Deficit Hyperactivity Disorder Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Attention Deficit Hyperactivity Disorder Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA