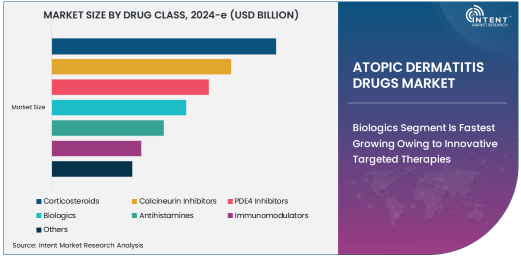

As per Intent Market Research, the Atopic Dermatitis Drugs Market was valued at USD 18.1 billion in 2024-e and will surpass USD 25.1 billion by 2030; growing at a CAGR of 5.7% during 2025 - 2030.

The atopic dermatitis (AD) drugs market is witnessing significant growth, fueled by the increasing prevalence of atopic dermatitis, rising awareness of treatment options, and the availability of advanced therapies. Atopic dermatitis, a chronic inflammatory skin condition, affects millions globally, particularly among children, which has prompted an accelerated demand for novel and effective therapeutic solutions. The market is diverse, encompassing a variety of drug classes such as corticosteroids, biologics, and newer classes like PDE4 inhibitors, each catering to different stages and severities of the disease. Advances in drug development, particularly in biologics, have revolutionized treatment for moderate-to-severe cases of AD, which were previously challenging to manage with traditional therapies.

In addition to the growing drug options, the market's expansion is also driven by evolving treatment preferences and an increased focus on personalized medicine. The market dynamics are strongly influenced by healthcare infrastructure improvements, particularly in emerging markets, where access to advanced therapies is improving. This global trend indicates a promising growth trajectory for both established and new entrants in the AD drugs market, with notable investments being directed towards research and development for innovative treatment options.

Biologics Segment Is Fastest Growing Owing to Innovative Targeted Therapies

The biologics segment within the atopic dermatitis drugs market is the fastest-growing, driven by the development of highly targeted therapies aimed at addressing the root causes of inflammation in the skin. Biologic drugs, such as dupilumab, have gained considerable attention due to their efficacy in treating moderate-to-severe cases of atopic dermatitis that do not respond to traditional treatments. The introduction of biologics has significantly transformed the management of AD by offering patients a more effective and long-term solution with fewer side effects compared to corticosteroids and immunomodulators.

The growth of the biologics segment is also bolstered by the increasing number of clinical trials and the success of biologics in both adult and pediatric populations. The ability to target specific molecules involved in the inflammatory process, such as IL-4 and IL-13, has demonstrated substantial improvement in patients' quality of life. Additionally, regulatory bodies' accelerated approval processes for these drugs have further contributed to their market success. As research into biologics continues, more treatments are expected to emerge, expanding the therapeutic options for AD patients.

Oral Route of Administration Is Largest Owing to Patient Convenience

The oral route of administration remains the largest subsegment within the atopic dermatitis drugs market, primarily due to its ease of use and convenience for patients. Oral therapies, such as systemic corticosteroids and PDE4 inhibitors, are widely prescribed because they offer a non-invasive treatment option for patients, especially those with moderate to severe forms of atopic dermatitis. The growing preference for oral drugs is attributed to the simplicity of administration and the ability to manage treatment regimens at home without the need for healthcare professional visits.

Oral medications are also increasingly favored due to advancements in formulations that enhance efficacy while minimizing side effects. For instance, PDE4 inhibitors, which offer a novel mechanism of action, provide patients with a reliable oral option that targets specific inflammatory pathways. The convenience factor of oral drugs has made them a dominant choice for both patients and healthcare providers, contributing to their continued growth within the AD treatment landscape.

Retail Pharmacies Are Largest Distribution Channel Owing to Easy Accessibility

Retail pharmacies are the largest distribution channel for atopic dermatitis drugs, owing to their widespread availability and ease of access for patients. These pharmacies provide both prescription and over-the-counter (OTC) treatments, making them a one-stop solution for individuals seeking relief from atopic dermatitis. With the increasing number of retail pharmacies globally, patients can easily obtain medications without the need for specialized healthcare settings. This accessibility has made retail pharmacies the most utilized distribution channel, particularly in regions where healthcare infrastructure is still developing.

The retail pharmacy sector benefits from strong consumer demand, especially in countries with established healthcare systems. Moreover, the growing trend of self-medication for mild to moderate cases of atopic dermatitis has further boosted the prominence of retail pharmacies in the drug distribution network. With the rise of e-commerce, online retail pharmacies are also expanding, providing patients with an alternative means of acquiring their medications, further solidifying the dominance of this distribution channel.

Dermatology Clinics Are Largest End-User Owing to Specialized Care

Dermatology clinics are the largest end-user of atopic dermatitis drugs, owing to their specialized care for skin conditions. These clinics offer expert diagnosis and tailored treatment plans, which are crucial for managing a chronic condition like atopic dermatitis. Dermatologists are more likely to prescribe advanced therapies, including biologics and immunomodulators, that require careful monitoring and follow-up care. The personalized approach of dermatology clinics ensures that patients receive optimal treatment for their specific condition, contributing to the high demand for AD drugs in this setting.

As the prevalence of atopic dermatitis continues to rise, the number of dermatology clinics is also increasing, particularly in urban areas. This growth is supported by the increasing availability of dermatological services and the expansion of specialized care for chronic skin conditions. Dermatology clinics are integral to the proper management of atopic dermatitis, making them the leading end-user segment in the market.

North America Is Largest Region Owing to Advanced Healthcare Systems

North America stands as the largest region for atopic dermatitis drugs, owing to its advanced healthcare infrastructure, high awareness levels, and extensive access to a wide range of treatment options. The United States, in particular, holds a dominant share of the market, driven by a large patient population and the availability of both traditional and advanced therapies. The region also benefits from significant research and development activities, which contribute to the continuous innovation of new treatments for atopic dermatitis.

In addition to the high healthcare standards, North America boasts a robust reimbursement system that ensures patients have access to the latest treatments. The regulatory environment is also conducive to the rapid approval of new drugs, particularly biologics, which are gaining traction in the AD market. With an increasing number of dermatologists and healthcare professionals offering specialized care for atopic dermatitis, North America is expected to maintain its leading position in the market for the foreseeable future.

Leading Companies and Competitive Landscape

The atopic dermatitis drugs market is characterized by the presence of several leading pharmaceutical companies that are driving innovation and shaping market dynamics. Prominent players in this space include AbbVie, Sanofi, Regeneron Pharmaceuticals, and Eli Lilly, among others. These companies have made significant investments in research and development to introduce novel therapies, particularly biologics, that address unmet needs in the treatment of atopic dermatitis.

The competitive landscape is evolving rapidly, with companies increasingly focusing on the development of targeted therapies that offer more effective and less invasive treatment options. There is also a growing trend of partnerships and collaborations between pharmaceutical companies and biotechnology firms to accelerate the development and commercialization of new AD treatments. This competitive environment is expected to foster continuous innovation, offering more choices and better outcomes for patients while driving market growth.

Recent Developments:

- In December 2024, Sanofi and Regeneron announced FDA approval for an expanded indication of Dupixent in pediatric atopic dermatitis.

- In November 2024, Pfizer launched a new oral PDE4 inhibitor for mild-to-moderate atopic dermatitis in key markets.

- In October 2024, AbbVie reported successful Phase III trial results for its biologic Rinvoq in severe atopic dermatitis patients.

- In September 2024, Eli Lilly and Company introduced an innovative topical JAK inhibitor for atopic dermatitis treatment.

- In August 2024, LEO Pharma A/S collaborated with a biotechnology firm to co-develop a next-generation biologic for eczema.

List of Leading Companies:

- Sanofi

- Regeneron Pharmaceuticals, Inc.

- Pfizer Inc.

- AbbVie Inc.

- Eli Lilly and Company

- Novartis AG

- Amgen Inc.

- LEO Pharma A/S

- Bayer AG

- GlaxoSmithKline plc

- AstraZeneca

- Johnson & Johnson

- Takeda Pharmaceutical Company Limited

- Almirall, S.A.

- Dermavant Sciences

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 18.1 billion |

|

Forecasted Value (2030) |

USD 25.1 billion |

|

CAGR (2025 – 2030) |

5.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Atopic Dermatitis Drugs Market By Drug Class (Corticosteroids, Calcineurin Inhibitors, PDE4 Inhibitors, Biologics, Antihistamines, Immunomodulators), By Route of Administration (Oral, Topical, Injectable), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Dermatology Clinics, Homecare Settings) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Sanofi, Regeneron Pharmaceuticals, Inc., Pfizer Inc., AbbVie Inc., Eli Lilly and Company, Novartis AG, Amgen Inc., LEO Pharma A/S, Bayer AG, GlaxoSmithKline plc, AstraZeneca, Johnson & Johnson, Takeda Pharmaceutical Company Limited, Almirall, S.A., Dermavant Sciences |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Atopic Dermatitis Drugs Market, by Drug Class (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Corticosteroids |

|

4.2. Calcineurin Inhibitors |

|

4.3. PDE4 Inhibitors |

|

4.4. Biologics |

|

4.5. Antihistamines |

|

4.6. Immunomodulators |

|

4.7. Others |

|

5. Atopic Dermatitis Drugs Market, by Route of Administration (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Oral |

|

5.2. Topical |

|

5.3. Injectable |

|

6. Atopic Dermatitis Drugs Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospital Pharmacies |

|

6.2. Retail Pharmacies |

|

6.3. Online Pharmacies |

|

7. Atopic Dermatitis Drugs Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospitals |

|

7.2. Dermatology Clinics |

|

7.3. Homecare Settings |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Atopic Dermatitis Drugs Market, by Drug Class |

|

8.2.7. North America Atopic Dermatitis Drugs Market, by Route of Administration |

|

8.2.8. North America Atopic Dermatitis Drugs Market, by Distribution Channel |

|

8.2.9. North America Atopic Dermatitis Drugs Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Atopic Dermatitis Drugs Market, by Drug Class |

|

8.2.10.1.2. US Atopic Dermatitis Drugs Market, by Route of Administration |

|

8.2.10.1.3. US Atopic Dermatitis Drugs Market, by Distribution Channel |

|

8.2.10.1.4. US Atopic Dermatitis Drugs Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Sanofi |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Regeneron Pharmaceuticals, Inc. |

|

10.3. Pfizer Inc. |

|

10.4. AbbVie Inc. |

|

10.5. Eli Lilly and Company |

|

10.6. Novartis AG |

|

10.7. Amgen Inc. |

|

10.8. LEO Pharma A/S |

|

10.9. Bayer AG |

|

10.10. GlaxoSmithKline plc |

|

10.11. AstraZeneca |

|

10.12. Johnson & Johnson |

|

10.13. Takeda Pharmaceutical Company Limited |

|

10.14. Almirall, S.A. |

|

10.15. Dermavant Sciences |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Atopic Dermatitis Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Atopic Dermatitis Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Atopic Dermatitis Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA