As per Intent Market Research, the Ataxia Market was valued at USD 3.1 Billion in 2024-e and will surpass USD 6.3 Billion by 2030; growing at a CAGR of 12.4% during 2025 - 2030.

The ataxia market is focused on the treatment and management of various forms of ataxia, a group of neurological disorders that affect coordination, balance, and motor skills. Ataxia can be caused by genetic mutations, neurodegeneration, or other health conditions, leading to challenges in mobility and daily activities. As there is currently no definitive cure for many types of ataxia, the market is primarily driven by treatment options aimed at improving the quality of life for patients. These treatments range from gene therapy and pharmacological solutions to physical, occupational, and speech therapy. The growing understanding of ataxia's genetic basis and advances in therapeutic approaches are shaping the future of this market. The demand for effective therapies, particularly in rare and orphan disease segments, is fueling investment in research and development and expanding the treatment landscape.

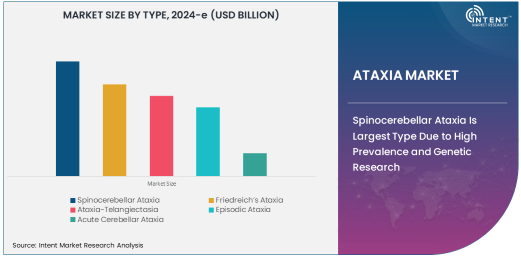

Spinocerebellar Ataxia Is Largest Type Due to High Prevalence and Genetic Research

Spinocerebellar ataxia (SCA) is the largest segment in the ataxia market due to its higher prevalence and extensive genetic research. SCA refers to a group of inherited ataxias characterized by progressive cerebellar degeneration, which leads to motor coordination issues and speech problems. Various subtypes of SCA are caused by mutations in different genes, making it a focus of genetic research and therapeutic development.

With advancements in genetic sequencing, researchers are gaining a deeper understanding of the specific mutations that cause SCA, which is crucial for developing targeted treatments. The high prevalence of SCA compared to other forms of ataxia and the growing emphasis on genetic research have made it the largest segment in the ataxia market, driving the development of gene therapies and more personalized pharmacological treatments.

Gene Therapy Is Fastest Growing Treatment Type Due to Potential for Cure

Gene therapy is the fastest-growing treatment type in the ataxia market, driven by its potential to address the root causes of genetic ataxias. Unlike traditional treatments that focus on symptom management, gene therapy aims to correct the underlying genetic defects responsible for the condition. In conditions like Friedreich's ataxia and spinocerebellar ataxia, where specific genetic mutations impair motor functions, gene therapy offers the promise of halting or even reversing disease progression.

The rapid advancements in gene-editing technologies, such as CRISPR, have accelerated the development of gene therapies for ataxia. Clinical trials are underway for several gene therapy candidates, and while the field is still evolving, the potential to cure or significantly alleviate symptoms of genetic ataxias is fueling strong investor interest and growth in this segment. As these therapies progress through clinical development, gene therapy is expected to become a dominant force in the ataxia market.

Hospitals Are Largest End-Use Industry Due to Specialized Care and Monitoring

Hospitals represent the largest end-use industry in the ataxia market, primarily due to their role in providing specialized care for individuals with severe forms of ataxia. Ataxia patients often require continuous monitoring and specialized interventions, including physical therapy, occupational therapy, and pharmacological treatments, all of which are available in hospital settings. Hospitals are also the primary location for advanced diagnostics, where genetic testing and imaging techniques are used to identify and monitor the progression of ataxia.

In addition, hospitals often serve as the site for clinical trials, especially in the case of gene therapies and new pharmacological treatments. The extensive resources available in hospitals, such as specialized neurological care teams, rehabilitation programs, and state-of-the-art diagnostic equipment, make them the leading end-use industry for ataxia treatment and care.

North America Is Largest Region Due to Advanced Healthcare and Research

North America is the largest region in the ataxia market, driven by advanced healthcare infrastructure, high levels of awareness, and significant research investments in rare diseases. The U.S. and Canada have established themselves as hubs for clinical trials, gene therapy development, and research into genetic disorders like ataxia. The region benefits from well-funded healthcare systems, access to cutting-edge treatments, and strong patient advocacy groups, which together drive market growth.

Additionally, North America has a high number of individuals affected by genetic ataxias, contributing to a robust demand for both symptom management and novel therapies. The region's focus on rare disease research, along with its large biotechnology and pharmaceutical industries, ensures that North America will remain the dominant region in the global ataxia market.

Competitive Landscape and Key Players

The ataxia market is competitive, with key players such as Pfizer, Novartis, and Biogen leading the way in research and development of treatments for ataxia. These companies are involved in clinical trials for gene therapies, as well as in the development of innovative pharmacological treatments and therapies aimed at improving the quality of life for ataxia patients.

In addition, smaller biotech companies focused on rare and orphan diseases are also contributing to the competitive landscape, developing novel therapies for specific forms of ataxia. The market is expected to continue seeing significant investment, as the development of gene therapies and other advanced treatments presents opportunities for market expansion. With ongoing research and breakthroughs in genetic medicine, the competitive landscape will likely continue to evolve, fostering innovation and increasing treatment options for patients worldwide.

Recent Developments:

- Sanofi initiated a clinical trial for a gene therapy targeting Friedreich’s ataxia, with the potential to address the underlying genetic cause of the disease.

- Biogen Idec announced a partnership with AveXis, Inc. to develop innovative gene therapies for spinocerebellar ataxia, aiming to provide more effective treatment options.

- Novartis expanded its portfolio with a new drug candidate for the treatment of ataxia-telangiectasia, currently undergoing Phase III clinical trials.

- Merck & Co., Inc. launched a new drug treatment for managing ataxia symptoms, which focuses on improving balance and motor coordination in patients.

- Bayer AG entered into an agreement with Regeneron Pharmaceuticals to collaborate on developing a biologic therapy for cerebellar ataxia related to neurodegenerative diseases.

List of Leading Companies:

- Sanofi

- Novartis AG

- Pfizer Inc.

- Merck & Co., Inc.

- Bayer AG

- Genzyme Corporation

- Amgen Inc.

- Biogen Idec

- AveXis, Inc.

- Novartis Gene Therapies

- AstraZeneca

- Eisai Co., Ltd.

- Regeneron Pharmaceuticals, Inc.

- Roche Holding AG

- Takeda Pharmaceutical Company Limited

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.1 Billion |

|

Forecasted Value (2030) |

USD 6.3 Billion |

|

CAGR (2025 – 2030) |

12.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Ataxia Market by Type (Spinocerebellar Ataxia, Friedreich’s Ataxia, Ataxia-Telangiectasia, Episodic Ataxia, Acute Cerebellar Ataxia), by Treatment Type (Gene Therapy, Pharmacological Treatment, Physical Therapy, Occupational Therapy, Speech Therapy), by End-Use Industry (Hospitals, Clinics, Research and Development Institutes); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Sanofi, Novartis AG, Pfizer Inc., Merck & Co., Inc., Bayer AG, Genzyme Corporation, Biogen Idec, AveXis, Inc., Novartis Gene Therapies, AstraZeneca, Eisai Co., Ltd., Regeneron Pharmaceuticals, Inc., Takeda Pharmaceutical Company Limited |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Ataxia Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Spinocerebellar Ataxia |

|

4.2. Friedreich’s Ataxia |

|

4.3. Ataxia-Telangiectasia |

|

4.4. Episodic Ataxia |

|

4.5. Acute Cerebellar Ataxia |

|

5. Ataxia Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Gene Therapy |

|

5.2. Pharmacological Treatment |

|

5.3. Physical Therapy |

|

5.4. Occupational Therapy |

|

5.5. Speech Therapy |

|

6. Ataxia Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Research and Development Institutes |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Ataxia Market, by Type |

|

7.2.7. North America Ataxia Market, by Treatment Type |

|

7.2.8. North America Ataxia Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Ataxia Market, by Type |

|

7.2.9.1.2. US Ataxia Market, by Treatment Type |

|

7.2.9.1.3. US Ataxia Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Sanofi |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Novartis AG |

|

9.3. Pfizer Inc. |

|

9.4. Merck & Co., Inc. |

|

9.5. Bayer AG |

|

9.6. Genzyme Corporation |

|

9.7. Amgen Inc. |

|

9.8. Biogen Idec |

|

9.9. AveXis, Inc. |

|

9.10. Novartis Gene Therapies |

|

9.11. AstraZeneca |

|

9.12. Eisai Co., Ltd. |

|

9.13. Regeneron Pharmaceuticals, Inc. |

|

9.14. Roche Holding AG |

|

9.15. Takeda Pharmaceutical Company Limited |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Ataxia Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Ataxia Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Ataxia Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA