As per Intent Market Research, the Assistive Technology Market was valued at USD 23.3 Billion in 2024-e and will surpass USD 41.8 Billion by 2030; growing at a CAGR of 10.2% during 2025 - 2030.

The assistive technology market is expanding rapidly, driven by technological innovations and the growing emphasis on enhancing the quality of life for individuals with disabilities. Assistive technologies enable people with various physical, sensory, cognitive, or learning disabilities to perform tasks and engage in activities they might otherwise find challenging. These technologies are crucial in fostering independence, improving functionality, and ensuring inclusivity in different sectors, including healthcare, education, and consumer electronics. With increasing awareness and advancements in design, the assistive technology market is poised for significant growth, addressing the diverse needs of users across various age groups and conditions.

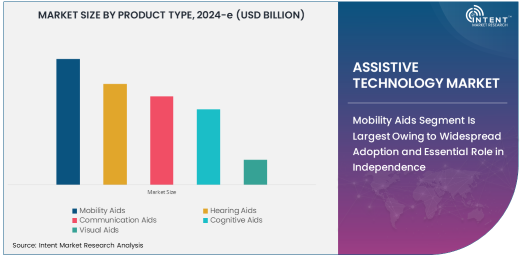

Mobility Aids Segment Is Largest Owing to Widespread Adoption and Essential Role in Independence

The mobility aids segment is the largest in the assistive technology market, primarily due to its essential role in enabling individuals with mobility impairments to maintain independence. Products such as wheelchairs, walkers, prosthetics, and crutches help people with mobility challenges navigate their environment and perform daily tasks.

The demand for mobility aids continues to rise as the global population ages and the prevalence of mobility-related conditions such as arthritis, spinal cord injuries, and neurological disorders increases. As mobility aids become more advanced, incorporating features like enhanced comfort, portability, and technological integration, their adoption remains widespread across healthcare facilities, rehabilitation centers, and in-home settings. This segment is expected to continue its dominance, supported by ongoing innovations and an increasing focus on accessibility.

Hearing Aids Segment Is Fastest Growing Owing to Technological Advancements and Aging Population

The hearing aids segment is the fastest-growing product type in the assistive technology market, driven by advancements in hearing aid technology and the increasing prevalence of hearing loss, especially among the aging population. Hearing aids, including traditional devices and more advanced digital models, help individuals with hearing impairments communicate effectively and engage with their surroundings.

The global rise in the number of people experiencing age-related hearing loss has contributed to the growing demand for hearing aids. Moreover, the adoption of advanced features such as Bluetooth connectivity, rechargeable batteries, and enhanced sound processing has made hearing aids more appealing to consumers. With a focus on improving user experience and increasing accessibility, the hearing aids segment is expected to see rapid growth, driven by technological innovations and an expanding consumer base.

Daily Living Assistance Segment Is Largest Application Owing to Widespread Need

The daily living assistance segment is the largest application within the assistive technology market, as these devices are designed to help individuals with disabilities perform everyday tasks such as eating, dressing, cooking, and personal care. This application includes a wide range of products, from mobility aids and hearing aids to cognitive and visual aids.

As the need for independence increases, especially among the elderly and individuals with chronic conditions, assistive devices for daily living have become essential. These products not only promote autonomy but also improve the overall quality of life for users. The growing demand for personalized solutions to assist with routine activities, coupled with the increasing global population of people with disabilities, ensures that this application remains dominant in the market.

Healthcare Segment Is Largest End-Use Industry Owing to Critical Role in Rehabilitation and Patient Care

The healthcare sector is the largest end-use industry for assistive technology, as it plays a critical role in rehabilitation, therapy, and supporting patients with disabilities. Healthcare providers utilize assistive devices to aid in recovery, promote mobility, and enhance communication for patients with physical, sensory, or cognitive impairments. Hospitals, rehabilitation centers, and healthcare facilities are key contributors to the demand for assistive technologies.

As healthcare services become more personalized and patient-centric, the role of assistive devices in improving outcomes for individuals with disabilities has become more significant. The healthcare sector’s focus on rehabilitation, post-surgery recovery, and long-term care further supports the sustained growth of assistive technology in this industry.

North America Is Largest Region Owing to Advanced Healthcare Systems and High Adoption Rates

North America is the largest region in the assistive technology market, primarily driven by the region’s advanced healthcare infrastructure, high levels of accessibility, and growing adoption of assistive devices. The United States, in particular, has established policies that promote inclusivity and provide extensive coverage for assistive technologies, making them more accessible to people with disabilities.

Moreover, the aging population in North America continues to drive demand for assistive technologies, particularly mobility aids, hearing aids, and cognitive aids. The region’s focus on innovation, coupled with supportive government initiatives and funding for assistive technology development, positions North America as the dominant market for these products.

Competitive Landscape and Key Players

The assistive technology market is competitive, with key players such as Philips, GN Hearing, Siemens Healthineers, Medtronic, and Tobii Group leading the way in the development of innovative solutions. These companies offer a wide range of products, including mobility aids, hearing aids, communication aids, and cognitive devices, catering to diverse needs across different industries.

The competitive landscape is driven by continuous innovation, with companies focusing on enhancing the functionality, affordability, and ease of use of their products. Research and development are key to ensuring that assistive technologies remain effective in improving users’ lives, and strategic partnerships are common to expand product offerings and reach new markets. With growing investment in personalized assistive devices, the market is expected to remain dynamic and responsive to the evolving needs of consumers.

Recent Developments:

- Philips Healthcare announced the launch of new smart mobility devices designed to improve the daily lives of people with disabilities.

- Cochlear Limited introduced a next-generation hearing implant offering improved sound quality for individuals with severe hearing loss.

- Sonova Holding AG acquired AudioNova, expanding its portfolio of hearing aids and services.

- Drive DeVilbiss Healthcare introduced advanced mobility solutions, including motorized wheelchairs and scooters.

- ReSound launched hearing aids with AI-driven sound processing, enhancing user experience in various environments.

List of Leading Companies:

- Philips Healthcare

- Medtronic PLC

- Cochlear Limited

- GN Store Nord A/S

- Drive DeVilbiss Healthcare

- Invacare Corporation

- Hollister Incorporated

- ReSound

- Oticon A/S

- Sonova Holding AG

- Bose Corporation

- American Hearing Systems, Inc.

- Teva Pharmaceuticals

- Starkey Hearing Technologies

- Kistler Group

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 23.3 Billion |

|

Forecasted Value (2030) |

USD 41.8 Billion |

|

CAGR (2025 – 2030) |

10.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Assistive Technology Market by Product Type (Mobility Aids, Hearing Aids, Communication Aids, Cognitive Aids, Visual Aids), by End-Use Industry (Healthcare, Education, Consumer Electronics), by Application (Daily Living Assistance, Educational Support, Medical Rehabilitation); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Philips Healthcare, Medtronic PLC, Cochlear Limited, GN Store Nord A/S, Drive DeVilbiss Healthcare, Invacare Corporation, ReSound, Oticon A/S, Sonova Holding AG, Bose Corporation, American Hearing Systems, Inc., Teva Pharmaceuticals, Kistler Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Assistive Technology Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Mobility Aids |

|

4.2. Hearing Aids |

|

4.3. Communication Aids |

|

4.4. Cognitive Aids |

|

4.5. Visual Aids |

|

5. Assistive Technology Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Healthcare |

|

5.2. Education |

|

5.3. Consumer Electronics |

|

6. Assistive Technology Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Daily Living Assistance |

|

6.2. Educational Support |

|

6.3. Medical Rehabilitation |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Assistive Technology Market, by Product Type |

|

7.2.7. North America Assistive Technology Market, by End-Use Industry |

|

7.2.8. North America Assistive Technology Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Assistive Technology Market, by Product Type |

|

7.2.9.1.2. US Assistive Technology Market, by End-Use Industry |

|

7.2.9.1.3. US Assistive Technology Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Philips Healthcare |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Medtronic PLC |

|

9.3. Cochlear Limited |

|

9.4. GN Store Nord A/S |

|

9.5. Drive DeVilbiss Healthcare |

|

9.6. Invacare Corporation |

|

9.7. Hollister Incorporated |

|

9.8. ReSound |

|

9.9. Oticon A/S |

|

9.10. Sonova Holding AG |

|

9.11. Bose Corporation |

|

9.12. American Hearing Systems, Inc. |

|

9.13. Teva Pharmaceuticals |

|

9.14. Starkey Hearing Technologies |

|

9.15. Kistler Group |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Assistive Technology Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Assistive Technology Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Assistive Technology Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA