As per Intent Market Research, the Aspartame Market was valued at USD 2.3 Billion in 2024-e and will surpass USD 3.9 Billion by 2030; growing at a CAGR of 9.0% during 2025 - 2030.

The aspartame market is witnessing steady growth, driven by increasing consumer demand for low-calorie and sugar-free food and beverage products. Aspartame is an artificial sweetener widely used as a sugar substitute, valued for its ability to provide the sweetness of sugar without the associated calories. It is commonly used in a wide variety of products, from diet sodas and sugar-free confectionery to pharmaceuticals and personal care products. The rising prevalence of lifestyle-related diseases such as obesity and diabetes is accelerating the adoption of aspartame in various industries, particularly in the food and beverage sector.

As consumer preferences shift towards healthier alternatives to sugar, the demand for low-calorie sweeteners like aspartame is expected to increase, further solidifying its position in the market. Additionally, as regulations on artificial sweeteners evolve, aspartame continues to be a key ingredient for manufacturers aiming to cater to health-conscious consumers without compromising on taste.

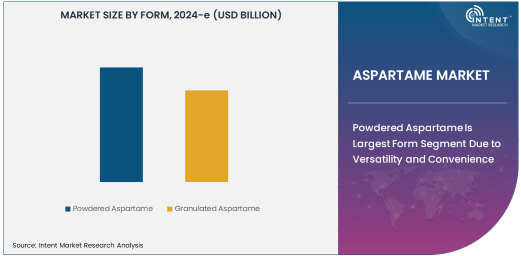

Powdered Aspartame Is Largest Form Segment Due to Versatility and Convenience

Powdered aspartame is the largest form segment in the market, owing to its versatility and convenience in various applications. As a fine powder, it is easy to incorporate into a wide range of food, beverage, and pharmaceutical products. Powdered aspartame is commonly used in the production of soft drinks, baked goods, confectioneries, and even table-top sweeteners, where precise measurements and a uniform texture are crucial. Its ease of use and ability to dissolve seamlessly in liquids further contribute to its popularity in both food and beverage manufacturing as well as pharmaceuticals.

The powdered form also allows for accurate dosage control, ensuring consistent sweetness in products while maintaining low calorie content. As more consumers demand sugar alternatives that offer taste without the health risks of sugar, powdered aspartame continues to be the preferred choice for manufacturers looking to meet this demand.

Food & Beverages Is Largest Application Segment Due to Rising Demand for Sugar Substitutes

The food and beverage industry represents the largest application segment for aspartame, driven by the increasing demand for sugar-free, low-calorie, and reduced-sugar products. With rising concerns about sugar consumption and its link to various health conditions such as obesity and diabetes, food and beverage manufacturers are increasingly turning to aspartame to provide sweetness without the added calories. Aspartame is particularly popular in products like diet sodas, sugar-free gum, and low-calorie snacks, allowing consumers to enjoy their favorite foods and drinks without guilt.

The growing health and wellness trend is propelling the demand for sugar substitutes like aspartame, as consumers seek healthier alternatives in their diets. This shift is further amplified by the increasing availability of sugar-free products across retail channels, making aspartame an essential ingredient for food and beverage manufacturers aiming to cater to the changing dietary preferences of consumers.

Food & Beverage Manufacturers Are Largest End-Use Industry Due to Widespread Adoption of Low-Calorie Products

Food and beverage manufacturers are the largest end-use industry for aspartame, as the demand for low-calorie and sugar-free products continues to rise. Aspartame's ability to provide a sweet taste with fewer calories has made it a key ingredient in a wide array of products, including beverages, baked goods, confectioneries, dairy products, and more. As consumers become more health-conscious, food and beverage manufacturers are increasingly adopting aspartame as a sweetening agent in their products to meet the growing preference for reduced-calorie and sugar-free alternatives.

The widespread use of aspartame in mass-market products such as diet sodas and sugar-free candies has solidified the dominance of food and beverage manufacturers in driving the growth of the aspartame market. As the demand for healthy, sugar-free options grows, these manufacturers continue to be the largest end-users of aspartame, contributing significantly to market expansion.

North America Is Fastest Growing Region Due to Health Trends and Demand for Sugar Alternatives

North America is the fastest-growing region in the aspartame market, primarily driven by the increasing demand for sugar substitutes amid growing health concerns. The region has seen a surge in consumer preference for low-calorie, sugar-free, and diabetic-friendly products, which has led to a rise in the use of artificial sweeteners like aspartame. The prevalence of obesity and diabetes in North America has spurred the need for healthier food and beverage options, further boosting the demand for products containing aspartame.

Additionally, North America has a well-established food and beverage manufacturing sector that is constantly innovating to meet the evolving consumer demand for sugar-free products. The region's growing emphasis on health and wellness is expected to continue driving the adoption of aspartame, making it the fastest-growing market for this sweetener.

Competitive Landscape and Key Players

The aspartame market is competitive, with key players such as NutraSweet, Ajinomoto Co., Inc., and Ingredion Incorporated leading the charge. These companies dominate the market by offering a range of aspartame products that cater to various sectors, including food and beverages, pharmaceuticals, and personal care.

Competitive strategies in the aspartame market include product innovation, capacity expansion, and strategic partnerships with food and beverage manufacturers to meet the growing demand for low-calorie and sugar-free products. Companies are also focusing on research and development to explore new applications of aspartame in emerging industries such as nutraceuticals and personal care products. As consumer preferences shift towards healthier alternatives, key players are expected to continue innovating to remain competitive in this evolving market.

Recent Developments:

- Ajinomoto Co., Inc. announced a new production facility for aspartame in Southeast Asia to meet rising demand in the region.

- NutraSweet Company launched a new line of high-purity aspartame products, catering to the pharmaceutical and food industries.

- Cargill, Inc. expanded its aspartame supply chain with a new partnership aimed at improving distribution efficiency in North America.

- Merisant Company revealed plans to increase production capacity for aspartame to support growing demand for sugar-free products globally.

- Sweeteners Plus, Inc. launched a sustainably sourced aspartame product line to cater to the growing demand for eco-friendly ingredients.

List of Leading Companies:

- NutraSweet Company

- Ajinomoto Co., Inc.

- Cargill, Inc.

- Merisant Company

- Sweeteners Plus, Inc.

- Hangzhou Sweetenjoy Biotechnology Co., Ltd.

- Zhejiang Medicine Co., Ltd.

- Jiangsu Lvyang Biotechnology Co., Ltd.

- Shanghai Sumar Chemtech Co., Ltd.

- Tate & Lyle PLC

- DSM Nutritional Products

- Novozymes

- SinoSweet Co., Ltd.

- Sucralose Inc.

- PureCircle Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.3 Billion |

|

Forecasted Value (2030) |

USD 3.9 Billion |

|

CAGR (2025 – 2030) |

9.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Aspartame Market by Form (Powdered Aspartame, Granulated Aspartame), by Application (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics), by End-Use Industry (Food & Beverage Manufacturers, Nutraceutical Companies, Pharmaceutical Companies); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

NutraSweet Company, Ajinomoto Co., Inc., Cargill, Inc., Merisant Company, Sweeteners Plus, Inc., Hangzhou Sweetenjoy Biotechnology Co., Ltd., Jiangsu Lvyang Biotechnology Co., Ltd., Shanghai Sumar Chemtech Co., Ltd., Tate & Lyle PLC, DSM Nutritional Products, Novozymes, SinoSweet Co., Ltd., PureCircle Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Aspartame Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Powdered Aspartame |

|

4.2. Granulated Aspartame |

|

5. Aspartame Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Food & Beverages |

|

5.2. Pharmaceuticals |

|

5.3. Personal Care & Cosmetics |

|

6. Aspartame Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverage Manufacturers |

|

6.2. Nutraceutical Companies |

|

6.3. Pharmaceutical Companies |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Aspartame Market, by Form |

|

7.2.7. North America Aspartame Market, by Application |

|

7.2.8. North America Aspartame Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Aspartame Market, by Form |

|

7.2.9.1.2. US Aspartame Market, by Application |

|

7.2.9.1.3. US Aspartame Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. NutraSweet Company |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Ajinomoto Co., Inc. |

|

9.3. Cargill, Inc. |

|

9.4. Merisant Company |

|

9.5. Sweeteners Plus, Inc. |

|

9.6. Hangzhou Sweetenjoy Biotechnology Co., Ltd. |

|

9.7. Zhejiang Medicine Co., Ltd. |

|

9.8. Jiangsu Lvyang Biotechnology Co., Ltd. |

|

9.9. Shanghai Sumar Chemtech Co., Ltd. |

|

9.10. Tate & Lyle PLC |

|

9.11. DSM Nutritional Products |

|

9.12. Novozymes |

|

9.13. SinoSweet Co., Ltd. |

|

9.14. Sucralose Inc. |

|

9.15. PureCircle Ltd. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Aspartame Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Aspartame Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Aspartame Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA