As per Intent Market Research, the Artificial Intelligence Based Security Market was valued at USD 7.6 Billion in 2024-e and will surpass USD 43.2 Billion by 2030; growing at a CAGR of 28.2% during 2025-2030.

The Artificial Intelligence (AI) Based Security market has witnessed unprecedented growth in recent years, driven by the increasing sophistication of cyber threats and the growing reliance on digital operations across industries. Organizations are actively seeking advanced security solutions to protect their critical assets, sensitive data, and customer information from evolving cyber risks. AI technologies, particularly machine learning (ML), deep learning (DL), and natural language processing (NLP), are playing a pivotal role in transforming traditional security frameworks into intelligent, automated systems capable of real-time threat detection, predictive analytics, and adaptive responses. As businesses strive to stay ahead of malicious actors, the adoption of AI-based security solutions is becoming a necessity to ensure operational resilience and compliance with stringent data protection regulations.

The integration of AI into security systems has significantly improved organizations’ ability to manage cybersecurity challenges effectively. By leveraging the power of machine learning algorithms, businesses can automate routine security tasks, such as threat identification and mitigation, while reducing the burden on human analysts. Additionally, AI’s ability to continuously learn and adapt ensures that security protocols remain current and effective in countering emerging threats. The market’s rapid expansion is driven not only by technological advancements but also by the growing awareness of the importance of cybersecurity at a global level. Enterprises across various sectors, including government, commercial, and residential, are adopting AI-based security solutions to safeguard their digital environments, which is further fueling market growth.

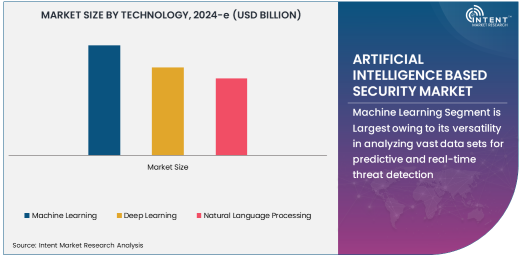

Machine Learning Segment is Largest owing to its versatility in analyzing vast data sets for predictive and real-time threat detection

Machine Learning (ML) stands as the cornerstone of AI-based security solutions, offering unparalleled capabilities to analyze massive volumes of structured and unstructured data. Organizations are increasingly relying on ML to automate the detection of anomalies, predict potential threats, and enhance the accuracy of security responses. By continuously learning from past data, ML models improve their performance, allowing businesses to preemptively address potential risks. Furthermore, ML’s adaptability allows security systems to evolve with new cyber threats, ensuring sustained protection. The scalability of ML solutions also supports its widespread adoption, as enterprises across various industries can integrate these solutions into existing infrastructures with minimal disruption.

In addition to its technical advantages, ML’s ability to process real-time data efficiently is driving its adoption. Companies are leveraging ML algorithms to manage and analyze logs, perform intrusion detection, and assess vulnerabilities at an unprecedented pace. With the increasing reliance on digital transformation and IoT devices, the demand for ML-driven security solutions is poised to grow further. Moreover, regulatory requirements for data protection, such as GDPR and CCPA, necessitate robust security measures, making ML an essential component for maintaining compliance. As enterprises become more sophisticated in their security strategies, machine learning remains at the forefront, ensuring they stay agile and resilient in the face of dynamic cybersecurity challenges.

Threat Detection Segment is Fastest Growing due to increasing sophisticated cyberattacks demanding real-time solutions

The Threat Detection segment has emerged as the fastest-growing application within the AI-based security market, driven by the urgent need for real-time identification and mitigation of cyber threats. Organizations are facing a surge in sophisticated cyberattacks, including ransomware, phishing, and insider threats, which require swift and precise intervention. AI-powered threat detection systems utilize machine learning and advanced analytics to identify patterns and behaviors indicative of malicious activity, allowing for proactive security measures. The ability to detect threats early minimizes the potential impact on business operations and customer trust.

The adoption of AI in threat detection is not limited to enterprises but is expanding into critical infrastructure, healthcare, and financial services where data security is paramount. Real-time threat detection ensures that security teams can respond effectively to incidents as they occur, reducing response times and enhancing incident resolution rates. Furthermore, AI systems continuously update their models to adapt to new attack vectors, keeping pace with the evolving cybersecurity landscape. As threats grow more complex, the need for intelligent, AI-driven threat detection systems becomes more apparent, driving the rapid growth of this segment across industries.

Cloud-Based Segment is Largest due to the flexibility and scalability it offers to enterprises for managing security needs

The Cloud-Based deployment model has established itself as the dominant segment in the AI-based security market due to its flexibility and scalability. Organizations are increasingly migrating to cloud environments for managing data and security operations, driven by the need for cost-efficient solutions and real-time accessibility. Cloud-based AI security solutions enable enterprises to quickly deploy and scale security services without the constraints of physical infrastructure. Additionally, the model offers seamless integration with other cloud services, allowing businesses to customize their security measures according to evolving needs.

The flexibility of cloud-based deployment extends to remote workforces and digital collaboration environments, where securing data across distributed networks is critical. With the rise of remote work and hybrid models, businesses rely on cloud security solutions to provide consistent protection and secure access to sensitive data. Moreover, cloud-based solutions offer enhanced disaster recovery capabilities and reduce the burden of managing on-premises infrastructure. As organizations prioritize agility and efficiency, the demand for scalable, cloud-based AI security services continues to soar, positioning it as the largest deployment segment in the market.

Commercial Segment is Fastest Growing as enterprises require comprehensive security solutions for business continuity and customer trust

The Commercial sector is experiencing rapid growth within the AI-based security market, driven by the increasing complexity of business operations and the need to safeguard critical assets. Enterprises, particularly in sectors like retail, finance, and e-commerce, are adopting AI-driven security solutions to protect customer data and prevent financial fraud. The ability to customize security measures to address specific business challenges makes AI solutions highly appealing in the commercial space.

As businesses expand their digital footprints, the demand for advanced security tools grows in parallel. AI technologies help commercial organizations streamline operations, automate compliance processes, and ensure secure data exchange across platforms. Furthermore, evolving regulatory landscapes necessitate sophisticated security frameworks that can adapt to changing standards. The commercial sector’s emphasis on growth, customer satisfaction, and regulatory adherence drives the rapid adoption of AI-based security solutions to meet these multifaceted demands.

North America is Largest Region owing to its advanced technological infrastructure and early adoption of AI security solutions

North America continues to lead the AI-based security market due to its advanced technological landscape and proactive stance on cybersecurity. Enterprises in this region are at the forefront of implementing cutting-edge AI solutions to combat complex security threats. North America’s emphasis on innovation and research has fostered the development of sophisticated AI-driven security systems, which are being integrated into industries ranging from finance and healthcare to government and retail. The region benefits from a highly competitive market, with companies like IBM, Cisco, and Palo Alto Networks investing heavily in AI capabilities to maintain a competitive edge.

The region’s robust cybersecurity regulations further accelerate the adoption of AI solutions, ensuring businesses meet stringent compliance requirements. North America’s commitment to cybersecurity, paired with the increasing sophistication of cyber threats, positions it as a key driver of innovation and growth in the AI-based security market. The continuous evolution of AI technologies, combined with a supportive regulatory environment, guarantees that North America remains at the forefront of the industry.

Competitive Landscape

The competitive landscape in the AI-based security market is dynamic, with leading companies such as IBM, Cisco, Palo Alto Networks, and Fortinet consistently expanding their capabilities through research and strategic partnerships. These firms are focused on enhancing their AI-driven solutions by integrating advanced machine learning, deep learning, and natural language processing technologies to meet evolving cybersecurity challenges. Additionally, startups and innovative players are entering the market, offering niche solutions tailored to specific sectors like healthcare, finance, and retail, driving a wave of competition and diversity in the market. As the cybersecurity landscape becomes increasingly complex, companies are adopting a collaborative approach, engaging in partnerships, acquisitions, and joint ventures to expand their offerings and enhance their market presence.

Recent Developments:

- Fortinet's Growth Amid Rising Demand for Secure Data Centers: Fortinet has experienced significant growth due to the increasing demand for secure data centers and cloud applications, with its stock reaching an all-time high.

- Google’s Acquisition of Mandiant Enhances Cybersecurity Offerings: Google acquired Mandiant to bolster its cybersecurity services, integrating Mandiant’s incident response and managed services with Google’s data capabilities.

- CrowdStrike CEO Highlights AI's Impact on Cybersecurity: CrowdStrike’s CEO emphasized how generative AI is enhancing hackers' capabilities, making cyberattacks more sophisticated and widespread.

- Mastercard’s $2.65 Billion Acquisition of Recorded Future: Mastercard plans to acquire Recorded Future to enhance its fraud prevention and cybersecurity services with AI-driven threat intelligence.

- Movistar Prosegur Integrates AI into Alarm Systems: Movistar Prosegur introduced AI-powered alarm systems that learn user routines and detect anomalies, enhancing home security.

List of Leading Companies:

- IBM Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- FireEye, Inc.

- CrowdStrike Holdings, Inc.

- Darktrace Ltd.

- Symantec Corporation

- McAfee, LLC

- Trend Micro Incorporated

- Sophos Group plc

- RSA Security LLC

- Juniper Networks, Inc.

- Splunk Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 7.6 Billion |

|

Forecasted Value (2030) |

USD 43.2 Billion |

|

CAGR (2025 – 2030) |

28.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Artificial Intelligence-Based Security Market By Technology (Machine Learning, Deep Learning, Natural Language Processing), By Application (Threat Detection, Video Surveillance, Incident Response), By Deployment Type (On-Premises, Cloud-Based, Hybrid), and By End-User (Government, Commercial, Residential) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

IBM Corporation, Cisco Systems, Inc., Palo Alto Networks, Inc., Fortinet, Inc., Check Point Software Technologies Ltd., FireEye, Inc., CrowdStrike Holdings, Inc., Darktrace Ltd., Symantec Corporation, McAfee, LLC, Trend Micro Incorporated, Sophos Group plc, RSA Security LLC, Juniper Networks, Inc., Splunk Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Artificial Intelligence Based Security Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Machine Learning |

|

4.2. Deep Learning |

|

4.3. Natural Language Processing |

|

5. Artificial Intelligence Based Security Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Threat Detection |

|

5.2. Video Surveillance |

|

5.3. Incident Response |

|

6. Artificial Intelligence Based Security Market, by Deployment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. On-Premises |

|

6.2. Cloud-Based |

|

6.3. Hybrid |

|

7. Artificial Intelligence Based Security Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Government |

|

7.2. Commercial |

|

7.3. Residential |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Artificial Intelligence Based Security Market, by Technology |

|

8.2.7. North America Artificial Intelligence Based Security Market, by Application |

|

8.2.8. North America Artificial Intelligence Based Security Market, by Deployment Type |

|

8.2.9. By Country |

|

8.2.9.1. US |

|

8.2.9.1.1. US Artificial Intelligence Based Security Market, by Technology |

|

8.2.9.1.2. US Artificial Intelligence Based Security Market, by Application |

|

8.2.9.1.3. US Artificial Intelligence Based Security Market, by Deployment Type |

|

8.2.9.2. Canada |

|

8.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. IBM Corporation |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Cisco Systems, Inc. |

|

10.3. Palo Alto Networks, Inc. |

|

10.4. Fortinet, Inc. |

|

10.5. Check Point Software Technologies Ltd. |

|

10.6. FireEye, Inc. |

|

10.7. CrowdStrike Holdings, Inc. |

|

10.8. Darktrace Ltd. |

|

10.9. Symantec Corporation |

|

10.10. McAfee, LLC |

|

10.11. Trend Micro Incorporated |

|

10.12. Sophos Group plc |

|

10.13. RSA Security LLC |

|

10.14. Juniper Networks, Inc. |

|

10.15. Splunk Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Artificial Intelligence-Based Security Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Artificial Intelligence-Based Security Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Artificial Intelligence-Based Security Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA