As per Intent Market Research, the Anemometer Market was valued at USD 0.4 Billion in 2024-e and will surpass USD 0.8 Billion by 2030; growing at a CAGR of 10.7% during 2025-2030.

The anemometer market has been steadily growing due to its critical applications across various industries, such as industrial manufacturing, power generation, HVAC systems, meteorology, and environmental research. These instruments are designed to measure air velocity or wind speed, which plays a key role in applications such as weather forecasting, industrial ventilation, and wind energy generation. Technological advancements and innovations in sensor technologies have made anemometers more accurate, reliable, and versatile. This, in turn, is driving the market growth globally. The demand for smarter, more efficient anemometers that can integrate with IoT systems and provide real-time data is expected to continue accelerating over the forecast period.

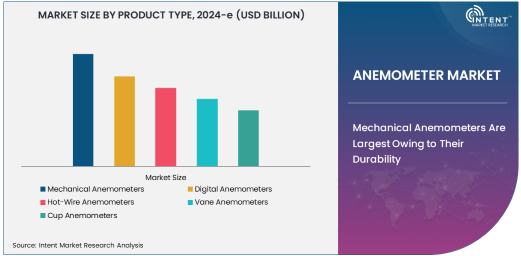

Mechanical Anemometers Are Largest Owing to Their Durability

Mechanical anemometers are the largest product type segment within the market. These traditional instruments, which include designs like cup and vane anemometers, are widely used in various industrial applications. Their mechanical components, such as rotating cups or vanes, detect air movement and convert it into measurable data. The durability and cost-effectiveness of mechanical anemometers make them a popular choice for industrial manufacturing and environmental monitoring. Additionally, these devices are often used in applications where accuracy is less critical, but reliability and ease of use are prioritized.

Despite the growing popularity of digital and hot-wire models, mechanical anemometers continue to dominate due to their robustness in harsh conditions. Industries such as construction and automotive benefit from these models, as they provide essential airflow and wind speed measurements without requiring complex electronics or power sources. The ease of maintenance and longer lifecycle of mechanical anemometers also contribute to their sustained market presence.

Industrial Applications Segment Is Fastest Growing Due to Demand for Accurate Monitoring

The industrial applications segment is the fastest-growing in the anemometer market. This growth can be attributed to the increasing demand for precise airflow measurement and monitoring of ventilation systems in industries like manufacturing and power generation. With heightened attention to workplace safety and air quality, accurate airflow measurement is critical for optimizing production processes and ensuring employee health. Anemometers are used to monitor airspeed, which helps prevent hazardous situations such as the buildup of fumes or gases. Additionally, the rise of automation in industries has led to an increased need for real-time data collection, which digital and hot-wire anemometers can provide efficiently.

Industrial applications also extend to energy efficiency in HVAC systems, where anemometers are used to optimize air distribution for energy savings. Their ability to monitor and regulate airflow, helping to maintain operational efficiency, is driving their growing adoption in various industrial settings. With increasing regulatory requirements around air quality and efficiency, industrial users are investing in anemometers to enhance their environmental control systems.

HVAC Systems Segment Is Largest Application Owing to Sustainability Trends

The HVAC systems segment is the largest application area within the anemometer market. The increasing focus on energy efficiency and sustainability in commercial and residential buildings is a key factor driving the demand for accurate airflow measurements in HVAC systems. Anemometers help in monitoring and regulating the airflow within ventilation systems, ensuring they operate at optimal levels. By maintaining the appropriate air velocity, HVAC systems can improve energy efficiency and indoor air quality. As sustainability becomes a higher priority for buildings, the demand for these instruments continues to rise.

In addition, with urbanization increasing globally, the need for efficient heating, ventilation, and air conditioning systems in both commercial and residential sectors has led to a surge in HVAC system installations. Anemometers play a vital role in commissioning, troubleshooting, and maintaining these systems, making them indispensable in ensuring that HVAC systems meet building standards and regulatory requirements.

Power Generation Industry Is Largest End-User Owing to Environmental Regulations

The power generation industry is the largest end-user of anemometers, particularly in the context of wind energy. With the growing reliance on renewable energy sources, wind power has become an essential part of global energy strategies. Anemometers are crucial for determining wind speed and direction, allowing for the optimal placement and operation of wind turbines. These instruments help measure wind flow to ensure that turbines are positioned in areas with the best wind conditions, which maximizes energy generation.

Additionally, the power generation sector, including both traditional and renewable energy plants, uses anemometers for environmental monitoring and to ensure compliance with emissions regulations. Accurate data on wind speed and air quality is vital for reducing emissions and improving environmental sustainability. As governments continue to push for stricter environmental standards, power generation companies are increasingly investing in anemometer technologies for compliance and operational optimization.

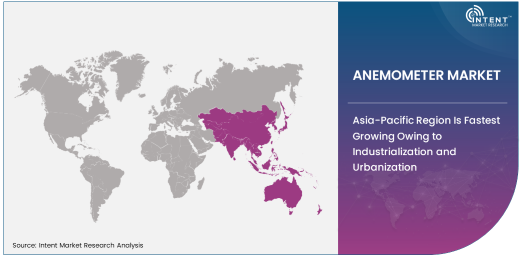

Asia-Pacific Region Is Fastest Growing Owing to Industrialization and Urbanization

The Asia-Pacific (APAC) region is the fastest-growing in the anemometer market. This growth can be attributed to the rapid industrialization and urbanization occurring across countries like China, India, and Southeast Asia. As these regions continue to expand their manufacturing capabilities, the demand for accurate air flow measurement in industrial applications, HVAC systems, and power generation increases. The region is also seeing significant investments in renewable energy projects, particularly in wind energy, which further drives the need for anemometers in both large-scale and local wind farms.

Moreover, the APAC region is experiencing an upsurge in the construction of smart cities and the implementation of sustainability initiatives, which fuels the demand for HVAC systems and environmental monitoring. This combination of factors makes the APAC region a hotbed of market activity for anemometer manufacturers, with an increasing focus on industrial efficiency and regulatory compliance driving demand.

Leading Companies and Competitive Landscape

The anemometer market is highly competitive, with several key players dominating the global landscape. Companies like Honeywell International, Testo SE & Co., and Omega Engineering are at the forefront, offering a wide range of anemometers catering to different applications, including industrial, environmental, and meteorological. These companies leverage their strong R&D capabilities to introduce innovative products, such as digital and hot-wire anemometers, which provide more accurate and efficient measurement capabilities.

In addition, companies such as Fluke Corporation and TSI Incorporated are focusing on expanding their product offerings to serve growing industries like HVAC and wind energy. Strategic mergers, acquisitions, and partnerships are also common, as companies aim to diversify their product portfolios and tap into new geographical markets, especially in emerging regions like Asia-Pacific. The competitive landscape is shaped by ongoing technological advancements and the increasing integration of IoT and smart sensors in anemometer designs to meet the demands of modern industrial operations.

Recent Developments:

- Honeywell International launched a new digital anemometer to enhance airflow measurement in industrial applications.

- Testo SE & Co. acquired a leading environmental monitoring company to expand its product range, including anemometers.

- Fluke Corporation announced the release of a next-generation anemometer with wireless connectivity for smart monitoring.

- Ametek Inc. launched a new line of vane anemometers designed for automotive testing applications.

- Omega Engineering upgraded its hot-wire anemometer line with improved sensor accuracy and expanded functionality for HVAC systems.

List of Leading Companies:

- Honeywell International Inc.

- Omega Engineering Inc.

- Fluke Corporation

- Ametek Inc.

- Testo SE & Co. KGaA

- TSI Incorporated

- Kestrel Meters

- Extech Instruments Corporation

- Lutron Electronics Co., Inc.

- Rika Detech

- Endress+Hauser

- Lufft

- Vaisala Corporation

- Shenzhen PCE Instruments

- Geonica

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.4 Billion |

|

Forecasted Value (2030) |

USD 0.8 Billion |

|

CAGR (2025 – 2030) |

10.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Anemometer Market By Product Type (Mechanical Anemometers, Digital Anemometers, Hot-Wire Anemometers, Vane Anemometers, Cup Anemometers), By Application (Industrial Applications, Meteorological Stations, HVAC Systems, Wind Energy, Environmental Monitoring), By End-User Industry (Industrial Manufacturing, Power Generation, Automotive, Construction, Environmental Research), and By Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Honeywell International Inc., Omega Engineering Inc., Fluke Corporation, Ametek Inc., Testo SE & Co. KGaA, TSI Incorporated, Kestrel Meters, Extech Instruments Corporation, Lutron Electronics Co., Inc., Rika Detech, Endress+Hauser, Lufft, Vaisala Corporation, Shenzhen PCE Instruments, Geonica |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Anemometer Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Mechanical Anemometers |

|

4.2. Digital Anemometers |

|

4.3. Hot-Wire Anemometers |

|

4.4. Vane Anemometers |

|

4.5. Cup Anemometers |

|

5. Anemometer Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Industrial Applications |

|

5.2. Meteorological Stations |

|

5.3. HVAC Systems |

|

5.4. Wind Energy |

|

5.5. Environmental Monitoring |

|

6. Anemometer Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Industrial Manufacturing |

|

6.2. Power Generation |

|

6.3. Automotive |

|

6.4. Construction |

|

6.5. Environmental Research |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Anemometer Market, by Product Type |

|

7.2.7. North America Anemometer Market, by Application |

|

7.2.8. North America Anemometer Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Anemometer Market, by Product Type |

|

7.2.9.1.2. US Anemometer Market, by Application |

|

7.2.9.1.3. US Anemometer Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Honeywell International Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Omega Engineering Inc. |

|

9.3. Fluke Corporation |

|

9.4. Ametek Inc. |

|

9.5. Testo SE & Co. KGaA |

|

9.6. TSI Incorporated |

|

9.7. Kestrel Meters |

|

9.8. Extech Instruments Corporation |

|

9.9. Lutron Electronics Co., Inc. |

|

9.10. Rika Detech |

|

9.11. Endress+Hauser |

|

9.12. Lufft |

|

9.13. Vaisala Corporation |

|

9.14. Shenzhen PCE Instruments |

|

9.15. Geonica |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Anemometer Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Anemometer Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Anemometer Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA