As per Intent Market Research, the Anca Vasculitis Drug Market was valued at USD 0.4 Billion in 2024-e and will surpass USD 0.8 Billion by 2030; growing at a CAGR of 10.7% during 2025-2030.

The ANCA vasculitis drug market is driven by the growing incidence of autoimmune diseases and the need for effective treatments to manage these chronic, often life-threatening conditions. ANCA (Anti-Neutrophil Cytoplasmic Antibody) vasculitis is a group of autoimmune disorders where the body's immune system mistakenly attacks blood vessels, causing inflammation and damage. The market for drugs targeting ANCA vasculitis has seen significant growth as the prevalence of the condition rises globally. Key factors influencing this growth include an increasing number of drug approvals, advances in biologic therapies, and better awareness of the disease. As more effective treatments are being developed, the demand for innovative drugs is expected to continue expanding.

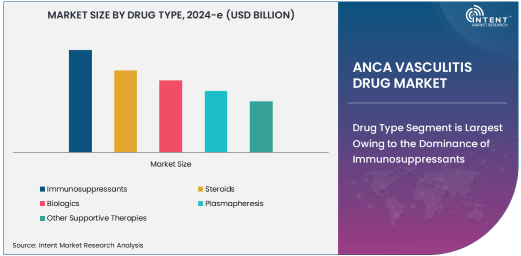

Drug Type Segment is Largest Owing to the Dominance of Immunosuppressants

Immunosuppressants are the largest drug class used in the treatment of ANCA vasculitis, making them a key driver of the market. These drugs are vital in controlling the immune system's overactivity by suppressing the immune response that leads to inflammation and damage to blood vessels. The use of immunosuppressants such as cyclophosphamide, methotrexate, and azathioprine is essential for managing acute episodes of ANCA vasculitis, as well as maintaining long-term remission in patients. Their ability to reduce relapse rates and improve survival outcomes has solidified their place as the first-line treatment.

As the market expands, immunosuppressants will continue to play a central role, particularly in the induction phase of treatment. However, newer therapies, including biologics, are gaining traction due to their targeted approach and ability to reduce side effects often associated with traditional immunosuppressive drugs. The combination of immunosuppressants with biologic therapies is likely to dominate the treatment landscape, contributing to the continued growth of this subsegment.

Mechanism of Action Segment is Fastest Growing Owing to Advancements in Monoclonal Antibodies

The mechanism of action segment in the ANCA vasculitis drug market is witnessing rapid growth, particularly with monoclonal antibodies. These biologic drugs, such as rituximab, are designed to target and inhibit specific components of the immune system involved in the disease process. Monoclonal antibodies work by targeting B-cells, which play a key role in the development of ANCA vasculitis. By selectively targeting B-cells, these drugs help reduce the inflammatory response without affecting the entire immune system, thus minimizing side effects.

Rituximab and similar monoclonal antibodies are becoming the go-to treatment in patients with severe or refractory ANCA vasculitis. Their ability to induce remission and manage relapse rates more effectively than traditional therapies has led to their growing adoption, making monoclonal antibodies the fastest-growing subsegment within this category. As clinical trials continue to validate their efficacy, and as more monoclonal antibody therapies are developed, the demand for these treatments will likely increase, further driving the growth of the segment.

Treatment Phase Segment is Largest Owing to the Importance of Induction Therapy

The treatment phase segment is largely dominated by induction therapy, the initial phase of treatment that aims to control acute disease flare-ups and stabilize the patient’s condition. Induction therapy is critical for patients with ANCA vasculitis as it helps to rapidly reduce inflammation and prevent life-threatening complications, such as organ damage and kidney failure. This phase typically involves the use of powerful immunosuppressants and biologics like rituximab to bring the disease under control as quickly as possible.

Induction therapy remains the most significant phase of treatment in the management of ANCA vasculitis due to the urgency of addressing the severe manifestations of the disease. Once remission is achieved through induction therapy, patients typically transition to maintenance therapy. However, the immediate need for aggressive treatment in the induction phase ensures that this subsegment will remain the largest in the market, even as new therapies and drug combinations emerge.

Route of Administration Segment is Fastest Growing Due to Increased Adoption of Subcutaneous Administration

The route of administration segment is experiencing significant growth in subcutaneous (SC) treatments for ANCA vasculitis. While intravenous (IV) therapies have long been the standard, subcutaneous administration is gaining popularity due to its ease of use and reduced need for hospital visits. SC treatments offer patients the convenience of self-administration at home, which is a critical factor in long-term management of chronic diseases like ANCA vasculitis. Drugs like rituximab and other biologics now come in SC formulations, making it easier for patients to adhere to treatment regimens and reduce hospital visits.

The adoption of SC administration has been fueled by patient preferences for less invasive and more flexible treatment options. The convenience of self-administered injections at home reduces treatment costs and hospital visits, making it an attractive option for many patients and healthcare systems. As more biologic therapies are developed with SC options, this route of administration will likely continue to grow, further driving the segment's expansion.

End-User Segment is Largest Owing to High Adoption in Hospitals

Hospitals are the largest end-user segment in the ANCA vasculitis drug market. Hospitals serve as the primary care setting for patients with severe or acute cases of ANCA vasculitis, requiring intensive treatment protocols and close monitoring. The presence of specialized rheumatologists and nephrologists, along with the necessary infrastructure for administering IV drugs and managing complex cases, makes hospitals the most common healthcare setting for treating ANCA vasculitis.

In addition to providing acute care, hospitals also play a critical role in the long-term management of the disease, especially in the induction therapy phase. As the number of patients diagnosed with ANCA vasculitis continues to grow, hospitals are expected to remain the dominant end-user, although other settings such as specialty clinics and homecare services are also seeing growth due to the increasing availability of oral and subcutaneous therapies.

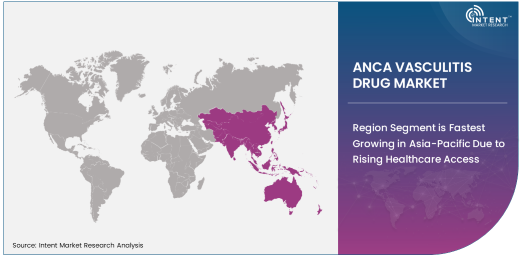

Region Segment is Fastest Growing in Asia-Pacific Due to Rising Healthcare Access

The Asia-Pacific (APAC) region is the fastest growing in the ANCA vasculitis drug market, driven by improving healthcare access and the rising burden of autoimmune diseases. The increasing awareness of ANCA vasculitis, along with government initiatives to enhance healthcare infrastructure, is contributing to the rapid market expansion in countries like China, Japan, and India. Furthermore, APAC’s large population and growing middle class are increasing demand for both advanced and affordable treatment options.

As healthcare systems in APAC continue to improve and more drugs are made available in these regions, the market for ANCA vasculitis drugs is expected to grow exponentially. The region also offers opportunities for global pharmaceutical companies to expand their footprint, especially as the adoption of biologics and immunotherapies increases among healthcare providers and patients. APAC is poised to play a significant role in the future of the ANCA vasculitis drug market, with steady growth in both urban and rural areas.

Leading Companies and Competitive Landscape

The ANCA vasculitis drug market is competitive, with several major pharmaceutical companies leading the charge in drug development and distribution. Companies like GlaxoSmithKline, Bristol-Myers Squibb, Pfizer, and Roche are at the forefront, offering a range of biologic and immunosuppressive therapies. These companies are investing heavily in research and development to bring new, more effective drugs to market, especially as biologic treatments become increasingly popular due to their targeted approach and reduced side effects.

The competitive landscape is marked by strategic mergers and acquisitions, partnerships, and collaborations to strengthen portfolios in the autoimmune and rare disease spaces. Additionally, the growing focus on personalized medicine and the development of combination therapies is changing the way ANCA vasculitis is treated. The market is expected to become more fragmented with the entry of smaller biotech firms and generic drug manufacturers, which will drive further innovation and competition in the space.

Recent Developments:

- GlaxoSmithKline announced the successful completion of Phase 3 clinical trials for its new biologic drug, which targets immune system modulation for ANCA vasculitis treatment.

- Bristol-Myers Squibb received FDA approval for its innovative biologic therapy to treat ANCA-associated vasculitis, significantly enhancing its position in the market.

- Pfizer entered into a strategic partnership with a leading biotech company to co-develop a monoclonal antibody therapy aimed at treating ANCA vasculitis more effectively.

- AbbVie secured regulatory approval for its immunosuppressive drug as a maintenance therapy for ANCA vasculitis, expanding its portfolio in autoimmune disease treatment.

- Amgen launched a new biologic drug designed to reduce relapses in patients with ANCA vasculitis, marking a significant milestone in the treatment of the disease.

List of Leading Companies:

- GlaxoSmithKline

- Bristol-Myers Squibb

- Pfizer

- Novartis

- Roche

- AbbVie

- Johnson & Johnson

- Merck & Co.

- Amgen

- Sanofi

- Takeda Pharmaceuticals

- AstraZeneca

- Eli Lilly and Co.

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.4 Billion |

|

Forecasted Value (2030) |

USD 0.8 Billion |

|

CAGR (2025 – 2030) |

10.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

ANCA Vasculitis Drug Market By Drug Type (Immunosuppressants, Steroids, Biologics, Plasmapheresis), By Mechanism of Action (T-Cell Inhibitors, B-Cell Inhibitors, Monoclonal Antibodies, Corticosteroids), By Treatment Phase (Induction Therapy, Maintenance Therapy, Refractory Treatment), By Route of Administration (Oral, Intravenous, Subcutaneous), By End-User (Hospitals, Specialty Clinics, Homecare), and By Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

GlaxoSmithKline, Bristol-Myers Squibb, Pfizer, Novartis, Roche, AbbVie, Johnson & Johnson, Merck & Co., Amgen, Sanofi, Takeda Pharmaceuticals, AstraZeneca, Eli Lilly and Co., Teva Pharmaceutical Industries, Boehringer Ingelheim |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Anca Vasculitis Drug Market, by Drug Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Immunosuppressants |

|

4.2. Steroids |

|

4.3. Biologics |

|

4.4. Plasmapheresis |

|

4.5. Other Supportive Therapies |

|

5. Anca Vasculitis Drug Market, by Mechanism of Action (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. T-Cell Inhibitors |

|

5.2. B-Cell Inhibitors |

|

5.3. Monoclonal Antibodies |

|

5.4. Corticosteroids |

|

5.5. Plasmapheresis |

|

6. Anca Vasculitis Drug Market, by Treatment Phase (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Induction Therapy |

|

6.2. Maintenance Therapy |

|

6.3. Refractory Treatment |

|

7. Anca Vasculitis Drug Market, by Route of Administration (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Oral |

|

7.2. Intravenous |

|

7.3. Subcutaneous |

|

8. Anca Vasculitis Drug Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Hospitals |

|

8.2. Specialty Clinics |

|

8.3. Homecare |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Anca Vasculitis Drug Market, by Drug Type |

|

9.2.7. North America Anca Vasculitis Drug Market, by Mechanism of Action |

|

9.2.8. North America Anca Vasculitis Drug Market, by Treatment Phase |

|

9.2.9. North America Anca Vasculitis Drug Market, by Route of Administration |

|

9.2.10. North America Anca Vasculitis Drug Market, by End-User |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Anca Vasculitis Drug Market, by Drug Type |

|

9.2.11.1.2. US Anca Vasculitis Drug Market, by Mechanism of Action |

|

9.2.11.1.3. US Anca Vasculitis Drug Market, by Treatment Phase |

|

9.2.11.1.4. US Anca Vasculitis Drug Market, by Route of Administration |

|

9.2.11.1.5. US Anca Vasculitis Drug Market, by End-User |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. GlaxoSmithKline |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Bristol-Myers Squibb |

|

11.3. Pfizer |

|

11.4. Novartis |

|

11.5. Roche |

|

11.6. AbbVie |

|

11.7. Johnson & Johnson |

|

11.8. Merck & Co. |

|

11.9. Amgen |

|

11.10. Sanofi |

|

11.11. Takeda Pharmaceuticals |

|

11.12. AstraZeneca |

|

11.13. Eli Lilly and Co. |

|

11.14. Teva Pharmaceutical Industries |

|

11.15. Boehringer Ingelheim |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the ANCA Vasculitis Drug Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the ANCA Vasculitis Drug Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the ANCA Vasculitis Drug Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA