As per Intent Market Research, the Ammonia Market was valued at USD 78.3 billion in 2023 and will surpass USD 102.6 billion by 2030; growing at a CAGR of 3.9% during 2024 - 2030.

The ammonia market is a crucial segment of the global chemical industry, driven primarily by its use in the production of fertilizers, industrial chemicals, and various other applications. As one of the most widely produced chemicals, ammonia plays a key role in modern agriculture, where it is predominantly used as a nitrogen source in fertilizers. Beyond agriculture, ammonia is also essential for refrigeration, water treatment, and the production of industrial chemicals, contributing to its vast application base. With a rising global population and increased food production demand, the ammonia market is expected to witness continued growth, particularly in emerging economies.

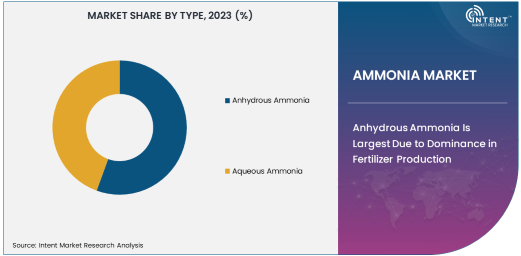

The ammonia market is divided into two major types: anhydrous ammonia and aqueous ammonia. Anhydrous ammonia, known for its higher concentration of nitrogen, is more widely used in the fertilizer industry, while aqueous ammonia, which is a solution of ammonia in water, serves applications in refrigeration and industrial processes. Additionally, the production of ammonia is primarily dominated by the Haber-Bosch process, although newer methods, such as the electrochemical process, are gaining traction due to their lower environmental impact.

Anhydrous Ammonia Is Largest Due to Dominance in Fertilizer Production

Anhydrous ammonia is the largest segment in the ammonia market, accounting for the majority of ammonia consumption globally. This is primarily driven by its widespread use in the production of nitrogen-based fertilizers, which are essential for enhancing agricultural productivity. Anhydrous ammonia provides an efficient and concentrated source of nitrogen, a key nutrient for plants. It is directly injected into the soil, improving crop yields, especially in regions with intensive agricultural activities.

As global demand for food continues to rise, driven by a growing population and changing dietary habits, the need for efficient and high-yielding fertilizers is increasing. Anhydrous ammonia’s role in this process ensures its position as the largest segment in the market. Its cost-effectiveness, high nitrogen content, and effectiveness in enhancing soil fertility are key factors contributing to its dominance in the ammonia market.

Fertilizers Application Is Largest Due to Strong Agricultural Demand

The fertilizers application segment is the largest in the ammonia market, largely due to the growing need for food production and agricultural sustainability. Ammonia is a core component in the production of nitrogen fertilizers, which are vital for the growth of crops and increasing agricultural yields. As the global population rises and arable land becomes more limited, the demand for fertilizers, particularly ammonia-based fertilizers, continues to grow.

In regions such as Asia-Pacific, North America, and Latin America, where agricultural practices are extensive, ammonia-based fertilizers are essential for maintaining soil health and boosting crop productivity. The shift towards sustainable farming practices and the development of advanced fertilizer formulations are expected to support the continued dominance of ammonia in the fertilizers segment.

Agriculture End-Use Industry Is Largest Due to Need for Fertilizers and Crop Production

The agriculture end-use industry is the largest in the ammonia market, as ammonia plays a critical role in crop production through its use in fertilizers. Ammonia-based fertilizers are integral to modern farming, providing essential nutrients to plants for optimal growth. In regions where agriculture is a dominant sector, such as in India, China, and parts of the U.S., ammonia demand is particularly strong.

Additionally, as the world faces increasing challenges in food security, the demand for fertilizers that can enhance agricultural output is expected to remain high. The agriculture industry’s reliance on ammonia for producing high-quality crops ensures that this end-use industry remains the largest in the ammonia market.

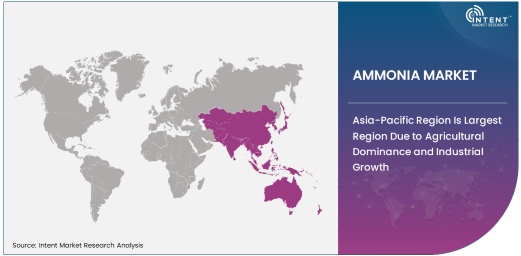

Asia-Pacific Region Is Largest Region Due to Agricultural Dominance and Industrial Growth

The Asia-Pacific region is the largest market for ammonia, driven by the extensive agricultural activities in countries like China, India, and Japan. These countries are among the largest producers and consumers of ammonia-based fertilizers, supporting the region’s dominance in the global ammonia market. The rapid industrialization and urbanization in Asia-Pacific also contribute to the demand for ammonia in sectors such as refrigeration, water treatment, and chemicals.

China and India are two of the largest agricultural producers globally, and their increasing reliance on ammonia fertilizers to boost crop yields ensures sustained market demand. As the region continues to grow both economically and industrially, the ammonia market in Asia-Pacific is expected to remain robust, with continued expansion in both the agricultural and industrial sectors.

Leading Companies and Competitive Landscape

The ammonia market is highly competitive, with several key global players dominating the production and supply of ammonia. Major companies such as Yara International, CF Industries, and Nutrien have a significant share of the market due to their extensive production capacities and global distribution networks. These companies are continuously investing in improving the efficiency of their ammonia production processes and expanding their product offerings.

The competitive landscape is also influenced by the shift toward more sustainable production methods, such as the electrochemical process, which reduces carbon emissions compared to the traditional Haber-Bosch method. This trend is expected to shape the future of the ammonia market, with companies striving to meet environmental regulations and sustainability goals. The emergence of new players and innovations in ammonia production technology will likely intensify competition, leading to further advancements in efficiency and environmental impact.

Recent Developments:

- In December 2024, Yara International expanded its ammonia production capabilities in Europe to meet rising demand for fertilizers.

- In November 2024, CF Industries announced the opening of a new ammonia plant in North America to support agricultural needs.

- In October 2024, SABIC partnered with a leading water treatment company to explore ammonia's role in sustainable water purification processes.

- In September 2024, Nutrien introduced a new ammonia-based fertilizer product designed to reduce emissions during use.

- In August 2024, The Dow Chemical Company launched a new ammonia refrigeration technology to improve energy efficiency in industrial cooling.

List of Leading Companies:

- Yara International

- CF Industries

- Nutrien

- BASF SE

- The Dow Chemical Company

- Koch Industries, Inc.

- Agrium Inc.

- OCI Nitrogen

- SABIC

- Mitsubishi Chemical Corporation

- Ineos

- Linde Group

- Air Products and Chemicals, Inc.

- Ballance Agri-Nutrients

- Sinochem International Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 78.3 billion |

|

Forecasted Value (2030) |

USD 102.6 billion |

|

CAGR (2024 – 2030) |

3.9% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Ammonia Market By Type (Anhydrous Ammonia, Aqueous Ammonia), By Application (Fertilizers, Refrigeration, Industrial Chemicals, Pharmaceuticals, Water Treatment), By Production Process (Haber-Bosch Process, Electrochemical Process), By End-Use Industry (Agriculture, Automotive, Chemical Manufacturing, Food & Beverage, Pharmaceuticals) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Yara International, CF Industries, Nutrien, BASF SE, The Dow Chemical Company, Koch Industries, Inc., Agrium Inc., OCI Nitrogen, SABIC, Mitsubishi Chemical Corporation, Ineos, Linde Group, Air Products and Chemicals, Inc., Ballance Agri-Nutrients, Sinochem International Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Ammonia Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Anhydrous Ammonia |

|

4.2. Aqueous Ammonia |

|

5. Ammonia Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Fertilizers |

|

5.2. Refrigeration |

|

5.3. Industrial Chemicals |

|

5.4. Pharmaceuticals |

|

5.5. Water Treatment |

|

6. Ammonia Market, by Production Process (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Haber-Bosch Process |

|

6.2. Electrochemical Process |

|

7. Ammonia Market, by End-Use Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Agriculture |

|

7.2. Automotive |

|

7.3. Chemical Manufacturing |

|

7.4. Food & Beverage |

|

7.5. Pharmaceuticals |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Ammonia Market, by Type |

|

8.2.7. North America Ammonia Market, by Application |

|

8.2.8. North America Ammonia Market, by Production Process |

|

8.2.9. North America Ammonia Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Ammonia Market, by Type |

|

8.2.10.1.2. US Ammonia Market, by Application |

|

8.2.10.1.3. US Ammonia Market, by Production Process |

|

8.2.10.1.4. US Ammonia Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Yara International |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. CF Industries |

|

10.3. Nutrien |

|

10.4. BASF SE |

|

10.5. The Dow Chemical Company |

|

10.6. Koch Industries, Inc. |

|

10.7. Agrium Inc. |

|

10.8. OCI Nitrogen |

|

10.9. SABIC |

|

10.10. Mitsubishi Chemical Corporation |

|

10.11. Ineos |

|

10.12. Linde Group |

|

10.13. Air Products and Chemicals, Inc. |

|

10.14. Ballance Agri-Nutrients |

|

10.15. Sinochem International Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Ammonia Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Ammonia Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Ammonia Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA