As per Intent Market Research, the Aluminum Market was valued at USD 0.2 Billion in 2024-e and will surpass USD 0.4 Billion by 2030; growing at a CAGR of 7.2% during 2025-2030.

The global aluminum market is an essential part of the non-ferrous metals industry, driven by its key applications in sectors such as automotive, construction, aerospace, and packaging. Its lightweight, corrosion-resistant properties make aluminum a preferred material in multiple industries, leading to its growing demand worldwide. The market is expected to expand steadily, driven by increasing adoption in high-performance applications, recycling initiatives, and the need for sustainable materials. Aluminum’s versatility across various product forms such as sheets, foils, and alloys continues to create opportunities in numerous end-use industries.

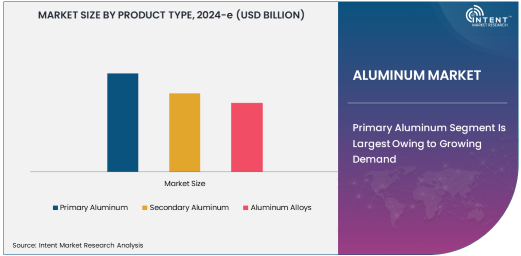

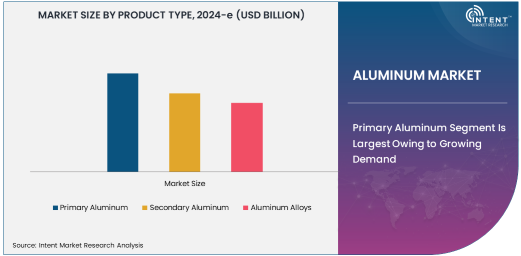

Primary Aluminum Segment Is Largest Owing to Growing Demand

The primary aluminum segment holds the largest share of the global aluminum market, primarily due to its extensive use in various manufacturing processes. As the foundational form of aluminum production, primary aluminum is used across diverse industries such as automotive, construction, and consumer electronics. Its significant application in building materials, vehicles, and packaging contributes to its dominance in the market. The production of primary aluminum is an energy-intensive process, but technological advancements in production efficiency and recycling are expected to sustain the growth of this segment.

The demand for primary aluminum in the automotive industry is particularly notable. With the growing emphasis on vehicle lightweighting for fuel efficiency and reducing emissions, automotive manufacturers are increasingly using aluminum in car bodies, engine components, and other structural parts. As global automotive production rises, the need for primary aluminum is expected to remain strong, further reinforcing its dominant position in the market.

Automotive & Transportation Industry Is Fastest Growing Due to Lightweighting Trends

The automotive and transportation industry is the fastest growing end-use sector for aluminum, driven by the widespread adoption of lightweight materials to improve fuel efficiency and reduce carbon emissions. As governments worldwide tighten regulations on emissions, automakers are turning to aluminum to help meet these standards. Aluminum's high strength-to-weight ratio makes it an ideal choice for the automotive sector, especially in the construction of car bodies, chassis, and engine components.

In addition to fuel efficiency, aluminum's recyclability and sustainability are becoming increasingly important in the transportation sector. With the automotive industry's focus on reducing environmental impact, the demand for aluminum as a preferred material is expected to continue rising. The shift toward electric vehicles (EVs) also plays a crucial role in this growth, as EVs require lightweight materials to improve range and energy efficiency. Thus, the automotive and transportation sector will remain a key driver for the aluminum market in the coming years.

Casting Application Is Largest Owing to Its Wide-Ranging Use

The casting application in the aluminum market is the largest, driven by its widespread use in industries such as automotive, machinery, and construction. Aluminum casting allows for the efficient production of complex shapes and designs, making it an attractive option for manufacturers. This versatility in design is particularly important in the automotive industry, where aluminum castings are used in engine blocks, transmission cases, and wheels.

The increased demand for lightweight, durable components in automotive manufacturing is a significant factor in the growth of aluminum casting. Additionally, the casting of aluminum is used extensively in the production of consumer electronics, industrial equipment, and military applications. As industries continue to innovate and adopt aluminum castings for new applications, this segment is expected to maintain its leading position in the market.

Asia Pacific Region Is Largest Market Driven by China’s Dominance

The Asia Pacific region is the largest market for aluminum, primarily driven by China’s dominance in both production and consumption. China is the world's largest producer of aluminum, accounting for over 50% of the global output. The country's strong industrial base, particularly in construction, automotive, and infrastructure, significantly contributes to the demand for aluminum. Additionally, China’s role as a global supplier of aluminum products has bolstered the region’s position in the global market.

Other countries in the Asia Pacific region, such as India and Japan, are also witnessing growing aluminum consumption due to industrial expansion and increasing demand for lightweight materials. As the region continues to urbanize, the need for aluminum in construction and transportation remains robust. The growing adoption of electric vehicles and the increase in automotive production in countries like China and India are expected to further drive the demand for aluminum, maintaining Asia Pacific's dominance in the market.

Competitive Landscape of the Aluminum Market

The global aluminum market is highly competitive, with several major players dominating the production and supply of aluminum products. Key companies such as Alcoa Corporation, Norsk Hydro ASA, and Rio Tinto Group hold significant market shares. These companies are focusing on expanding their production capacities, improving sustainability through recycling initiatives, and advancing technological innovations in aluminum processing.

In addition to large multinational companies, regional players also contribute to the competitive landscape, particularly in Asia Pacific. For instance, China Hongqiao Group and United Company RUSAL are significant players in the market, catering to the local and global demand for aluminum products. The competitive environment is also influenced by the growing emphasis on reducing carbon emissions, with many companies investing in energy-efficient production processes and sustainable practices to meet regulatory standards. As the demand for aluminum continues to rise, the competitive landscape will remain dynamic, with companies focusing on innovation, efficiency, and sustainability to maintain their market positions.

Overall, the aluminum market is expected to grow steadily as industries continue to seek lightweight, durable, and sustainable materials. The key drivers of growth will be the increasing adoption of aluminum in automotive, construction, and electronics, with the Asia Pacific region maintaining its position as the largest market for aluminum. Leading companies will continue to innovate and expand to meet the growing demand, ensuring the long-term prospects of the aluminum market remain positive.

Recent Developments:

- Alcoa Corporation announced the launch of a new aluminum alloy for automotive applications, promising enhanced strength and weight reduction for car manufacturers.

- . Norsk Hydro ASA acquired a major aluminum recycling plant in Europe, expanding its recycling capabilities and further reducing carbon emissions.

- China Hongqiao Group signed a joint venture agreement with a leading energy company to develop a large-scale, low-emission aluminum production facility.

- United Company RUSAL received regulatory approval for a new aluminum smelting plant in Siberia, expected to significantly boost its output and market share.

- Vedanta Resources launched a new line of aluminum products targeted at the rapidly growing electric vehicle market, focusing on lightweight components.

List of Leading Companies:

- Alcoa Corporation

- Rio Tinto Group

- Norsk Hydro ASA

- China Hongqiao Group Limited

- United Company RUSAL

- Emirates Global Aluminium

- Vedanta Resources Limited

- China Power Investment Corporation

- Norsk Hydro ASA

- Hindalco Industries Ltd.

- Jindal Aluminium Ltd.

- Novelis Inc.

- Constellium N.V.

- Manaksia Limited

- Aleris Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.2 Billion |

|

Forecasted Value (2030) |

USD 0.4 Billion |

|

CAGR (2025 – 2030) |

7.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Aluminum Market By Product Type (Primary Aluminum, Secondary Aluminum, Aluminum Alloys), By Application (Automotive, Construction, Electrical & Electronics, Packaging, Aerospace & Defense), By End-Use Industry (Automotive Industry, Construction Industry, Aerospace & Defense Industry, Electrical & Electronics Industry) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Alcoa Corporation, Rio Tinto Group, Norsk Hydro ASA, China Hongqiao Group Limited, United Company RUSAL, Emirates Global Aluminium, Vedanta Resources Limited, China Power Investment Corporation, Norsk Hydro ASA, Hindalco Industries Ltd., Jindal Aluminium Ltd., Novelis Inc., Constellium N.V., Manaksia Limited, Aleris Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Aluminum Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Primary Aluminum |

|

4.2. Secondary Aluminum |

|

4.3. Aluminum Alloys |

|

5. Aluminum Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Automotive & Transportation |

|

5.2. Building & Construction |

|

5.3. Electrical & Electronics |

|

5.4. Packaging |

|

5.5. Machinery & Equipment |

|

5.6. Consumer Goods |

|

6. Aluminum Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Casting |

|

6.2. Rolling |

|

6.3. Extrusion |

|

6.4. Forging |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Aluminum Market, by Product Type |

|

7.2.7. North America Aluminum Market, by End-Use Industry |

|

7.2.8. North America Aluminum Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Aluminum Market, by Product Type |

|

7.2.9.1.2. US Aluminum Market, by End-Use Industry |

|

7.2.9.1.3. US Aluminum Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Alcoa Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Rio Tinto Group |

|

9.3. Norsk Hydro ASA |

|

9.4. China Hongqiao Group Limited |

|

9.5. United Company RUSAL |

|

9.6. Emirates Global Aluminium |

|

9.7. Vedanta Resources Limited |

|

9.8. China Power Investment Corporation |

|

9.9. Norsk Hydro ASA |

|

9.10. Hindalco Industries Ltd. |

|

9.11. Jindal Aluminium Ltd. |

|

9.12. Novelis Inc. |

|

9.13. Constellium N.V. |

|

9.14. Manaksia Limited |

|

9.15. Aleris Corporation |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Aluminum Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Aluminum Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Aluminum Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA