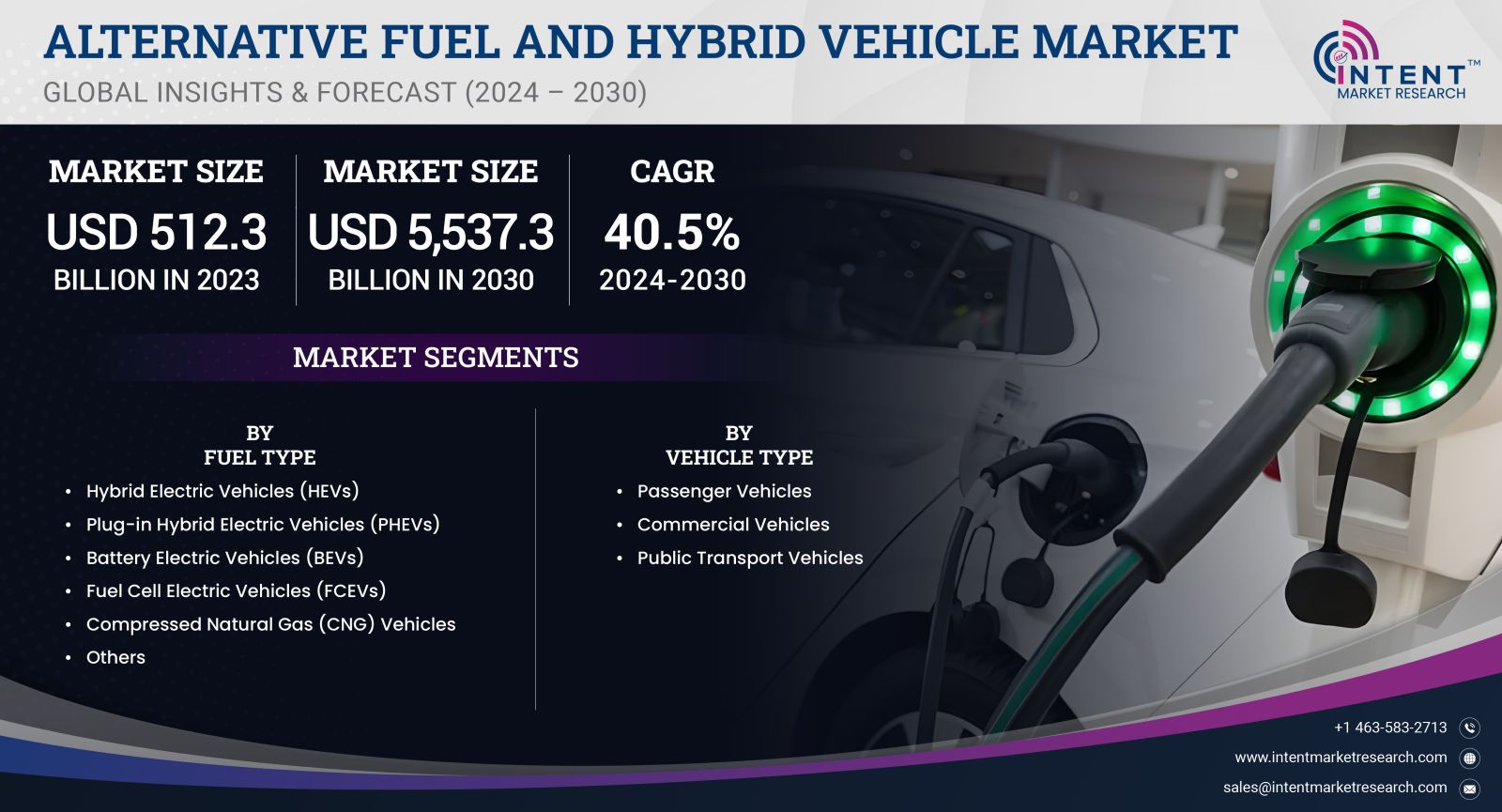

As per Intent Market Research, the Alternative Fuel and Hybrid Vehicle Market was valued at USD 512.3 billion in 2023 and will surpass USD 5,537.3 billion by 2030; growing at a CAGR of 40.5% during 2024 - 2030.

The global Alternative Fuel and Hybrid Vehicle Market is rapidly evolving, driven by increasing environmental awareness, stringent emission regulations, and a growing demand for sustainable transportation solutions. As the world transitions toward a greener future, the market is witnessing significant advancements in vehicle technology, resulting in a surge of innovative alternatives to traditional gasoline and diesel engines. The market encompasses a variety of segments, including hybrid vehicles, battery electric vehicles (BEVs), hydrogen fuel cell vehicles (FCVs), and alternative fuels like biofuels and compressed natural gas (CNG).

Hybrid Vehicle Segment is Largest Owing to Increased Adoption

The hybrid vehicle segment remains the largest in the alternative fuel market, primarily due to the widespread adoption of hybrid electric vehicles (HEVs). HEVs combine a conventional internal combustion engine (ICE) with an electric propulsion system, which enhances fuel efficiency and reduces emissions. The popularity of HEVs is attributed to their ability to provide a seamless driving experience while delivering better fuel economy than traditional vehicles. Major automotive manufacturers have invested heavily in hybrid technology, leading to a diverse range of models that cater to varying consumer preferences.

The growing awareness of environmental issues and rising fuel prices have further fueled the demand for hybrid vehicles. Government incentives and subsidies, along with the introduction of advanced hybrid technologies, have made HEVs more appealing to consumers. As a result, the hybrid vehicle segment is expected to dominate the market during the forecast period, contributing significantly to the overall growth of the alternative fuel and hybrid vehicle market.

Battery Electric Vehicles Segment is Fastest Growing Owing to Technological Advancements

The battery electric vehicle (BEV) segment is the fastest-growing sub-segment in the alternative fuel market, propelled by rapid advancements in battery technology and a strong push toward zero-emission transportation. BEVs, which run entirely on electric power, have gained traction as consumers increasingly prioritize sustainability and energy efficiency. The decline in battery costs, coupled with enhancements in energy density and charging infrastructure, has made BEVs more accessible to a broader audience.

The rising global commitment to carbon neutrality and stringent emission regulations in many regions have catalyzed the shift towards BEVs. With governments implementing favorable policies, such as tax incentives and subsidies, the adoption of BEVs is expected to surge. Major automakers are expanding their electric vehicle portfolios, introducing new models that cater to different market segments, thereby fueling the growth of this dynamic sub-segment. As a result, the BEV segment is poised for remarkable growth during the forecast period, marking a significant shift in consumer preferences toward fully electric mobility solutions.

Hydrogen Fuel Cell Vehicles Segment is Gaining Momentum Owing to Sustainable Solutions

The hydrogen fuel cell vehicle (FCV) segment is gaining momentum, driven by the increasing emphasis on sustainable solutions and the need for zero-emission alternatives in the transportation sector. FCVs utilize hydrogen gas to generate electricity, emitting only water vapor as a byproduct. This technology offers an attractive solution for long-range transportation, as FCVs can refuel in minutes, similar to conventional vehicles, and provide a driving range comparable to gasoline-powered cars.

The growth of the hydrogen FCV segment is being supported by significant investments in hydrogen infrastructure and technology development. Governments and private enterprises are collaborating to establish hydrogen production, storage, and distribution networks, which are critical for the widespread adoption of FCVs. As public awareness of hydrogen technology increases and more manufacturers enter the market, the FCV segment is expected to experience robust growth, contributing to the overall advancement of alternative fuel vehicles.

Compressed Natural Gas Vehicles Segment is Largest Owing to Cost-Effectiveness

The compressed natural gas (CNG) vehicle segment remains the largest in the alternative fuel market due to its cost-effectiveness and relatively lower greenhouse gas emissions compared to traditional fuels. CNG vehicles utilize natural gas as a cleaner alternative to gasoline or diesel, making them popular among fleet operators and public transportation systems looking to reduce operational costs and emissions. The availability of natural gas infrastructure in many regions has further supported the adoption of CNG vehicles, particularly in urban areas where air quality is a significant concern.

The increasing demand for cleaner transportation solutions, coupled with favorable government policies promoting the use of natural gas, has led to the growth of the CNG vehicle segment. Furthermore, advancements in CNG vehicle technology, including improved engine efficiency and expanded vehicle offerings, have made CNG a viable option for a wider range of consumers. As a result, the CNG vehicle segment is expected to maintain its dominance in the alternative fuel market, appealing to both commercial and individual users seeking cost-effective and environmentally friendly transportation solutions.

Biofuels Segment is Fastest Growing Owing to Renewable Energy Trends

The biofuels segment is the fastest-growing sub-segment in the alternative fuel market, driven by the increasing emphasis on renewable energy sources and the quest for energy independence. Biofuels, produced from organic materials such as crops, waste, and algae, offer a sustainable alternative to fossil fuels. The growing awareness of climate change and the need to reduce carbon emissions have propelled governments and industries to invest in biofuel technologies.

Innovations in biofuel production, including advancements in second- and third-generation biofuels, are enhancing the efficiency and sustainability of biofuel sources. As more automakers adopt biofuel-compatible engines, the demand for biofuels is expected to rise significantly. Additionally, government policies promoting the blending of biofuels with conventional fuels further contribute to the growth of this segment. With a clear focus on renewable energy, the biofuels segment is set to flourish, aligning with global efforts to transition towards cleaner energy solutions.

Leading Regions in the Alternative Fuel and Hybrid Vehicle Market

In the Alternative Fuel and Hybrid Vehicle Market, North America is the largest region, driven by a combination of technological advancements, stringent emission regulations, and growing consumer awareness regarding sustainable transportation. The United States, in particular, has been at the forefront of adopting alternative fuel technologies, with a well-established electric vehicle market and supportive infrastructure. The region's commitment to reducing greenhouse gas emissions, coupled with government incentives for electric and hybrid vehicles, has led to significant growth in the market.

Asia-Pacific is the fastest-growing region, fueled by rising urbanization, increased disposable income, and government initiatives to promote electric and hybrid vehicles. Countries like China and Japan are leading the charge in adopting alternative fuel technologies, with significant investments in electric vehicle manufacturing and infrastructure development. The growing demand for clean and efficient transportation solutions, along with the expansion of charging networks, positions the Asia-Pacific region for substantial growth in the alternative fuel and hybrid vehicle market during the forecast period.

Competitive Landscape and Leading Companies

The competitive landscape of the Alternative Fuel and Hybrid Vehicle Market is characterized by a diverse array of players, ranging from established automotive giants to emerging startups focused on innovative technologies. Major companies, including Toyota, Tesla, Honda, Ford, and General Motors, dominate the market with their extensive portfolios of hybrid and electric vehicles. These companies are actively investing in research and development to enhance their product offerings, focusing on improving battery technologies, expanding charging infrastructure, and enhancing the overall driving experience.

As the market continues to evolve, collaboration among industry players is becoming increasingly important. Partnerships between automotive manufacturers, technology firms, and energy providers are driving the development of integrated solutions that address consumer needs for sustainable transportation. The competitive landscape is expected to intensify as new entrants enter the market and existing players expand their offerings, further accelerating the growth of the Alternative Fuel and Hybrid Vehicle Market.

Report Objectives:

The report will help you answer some of the most critical questions in the Alternative Fuel and Hybrid Vehicle Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the Alternative Fuel and Hybrid Vehicle Market?

- What is the size of the Alternative Fuel and Hybrid Vehicle Market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 512.3 billion |

|

Forecasted Value (2030) |

USD 5,537.3 billion |

|

CAGR (2024 – 2030) |

40.5% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Alternative Fuel and Hybrid Vehicle Market By Fuel Type (Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Battery Electric Vehicles (BEVs), Fuel Cell Electric Vehicles (FCEVs), Compressed Natural Gas (CNG) Vehicles), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Public Transport Vehicles, Two-wheelers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Alternative Fuel and Hybrid Vehicle Market, by Fuel Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Hybrid Electric Vehicles (HEVs) |

|

4.2. Plug-in Hybrid Electric Vehicles (PHEVs) |

|

4.3. Battery Electric Vehicles (BEVs) |

|

4.4. Fuel Cell Electric Vehicles (FCEVs) |

|

4.5. Compressed Natural Gas (CNG) Vehicles |

|

4.6. Others |

|

5. Alternative Fuel and Hybrid Vehicle Market, by Vehicle Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Passenger Vehicles |

|

5.2. Commercial Vehicles |

|

5.3. Public Transport Vehicles |

|

6. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Regional Overview |

|

6.2. North America |

|

6.2.1. Regional Trends & Growth Drivers |

|

6.2.2. Barriers & Challenges |

|

6.2.3. Opportunities |

|

6.2.4. Factor Impact Analysis |

|

6.2.5. Technology Trends |

|

6.2.6. North America Alternative Fuel and Hybrid Vehicle Market, by Fuel Type |

|

6.2.7. North America Alternative Fuel and Hybrid Vehicle Market, by Vehicle Type |

|

6.2.8. By Country |

|

6.2.8.1. US |

|

6.2.8.1.1. US Alternative Fuel and Hybrid Vehicle Market, by Fuel Type |

|

6.2.8.1.2. US Alternative Fuel and Hybrid Vehicle Market, by Vehicle Type |

|

6.2.8.2. Canada |

|

6.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

6.3. Europe |

|

6.4. Asia-Pacific |

|

6.5. Latin America |

|

6.6. Middle East & Africa |

|

7. Competitive Landscape |

|

7.1. Overview of the Key Players |

|

7.2. Competitive Ecosystem |

|

7.2.1. Level of Fragmentation |

|

7.2.2. Market Consolidation |

|

7.2.3. Product Innovation |

|

7.3. Company Share Analysis |

|

7.4. Company Benchmarking Matrix |

|

7.4.1. Strategic Overview |

|

7.4.2. Product Innovations |

|

7.5. Start-up Ecosystem |

|

7.6. Strategic Competitive Insights/ Customer Imperatives |

|

7.7. ESG Matrix/ Sustainability Matrix |

|

7.8. Manufacturing Network |

|

7.8.1. Locations |

|

7.8.2. Supply Chain and Logistics |

|

7.8.3. Product Flexibility/Customization |

|

7.8.4. Digital Transformation and Connectivity |

|

7.8.5. Environmental and Regulatory Compliance |

|

7.9. Technology Readiness Level Matrix |

|

7.10. Technology Maturity Curve |

|

7.11. Buying Criteria |

|

8. Company Profiles |

|

8.1. BMW |

|

8.1.1. Company Overview |

|

8.1.2. Company Financials |

|

8.1.3. Product/Service Portfolio |

|

8.1.4. Recent Developments |

|

8.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

8.2. BYD |

|

8.3. Daimler |

|

8.4. Ford |

|

8.5. General Motors |

|

8.6. Honda |

|

8.7. Hyundai Motor |

|

8.8. Nissan |

|

8.9. Tesla |

|

8.10. Toyota |

|

8.11. Volkswagen |

|

8.12. Volvo |

|

9. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Alternative Fuel and Hybrid Vehicle Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Alternative Fuel and Hybrid Vehicle Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the Alternative Fuel and Hybrid Vehicle ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Alternative Fuel and Hybrid Vehicle Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA