As per Intent Market Research, the Almond Flour Market was valued at USD 1.8 billion in 2023 and will surpass USD 3.3 billion by 2030; growing at a CAGR of 9.5% during 2024 - 2030.

The almond flour market is witnessing significant growth as consumers increasingly opt for gluten-free and healthy alternatives to traditional wheat flour. A key player in this market is blanched almond flour, made by removing the skin of the almonds before grinding them into a fine powder. This process results in a smoother texture and lighter color, making it ideal for a wide variety of baked goods. Blanched almond flour is especially popular in recipes for cakes, cookies, pancakes, and bread, as it provides a light and airy texture, while also offering nutritional benefits such as protein, fiber, and healthy fats.

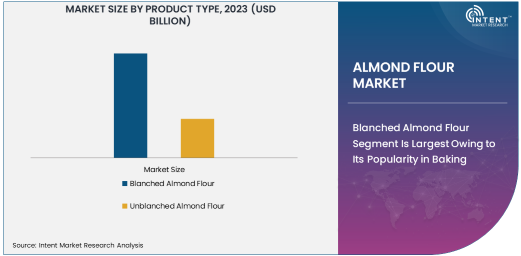

Blanched Almond Flour Segment Is Largest Owing to Its Popularity in Baking

Blanched almond flour is the largest subsegment within the almond flour market, owing to its dominant position in the gluten-free baking space. Its smooth texture and neutral flavor make it highly versatile, appealing to both health-conscious consumers and professional bakers. As the demand for gluten-free and low-carb diets continues to rise, the need for blanched almond flour is expected to increase, further cementing its position as the leading product type in the market.

Supermarkets/Hypermarkets Segment Is Largest Due to Wide Consumer Reach

The almond flour market is expanding rapidly, with various distribution channels contributing to its growth. Among these, supermarkets and hypermarkets hold the largest share, driven by their widespread consumer reach and established infrastructure. These retail outlets are convenient for customers who prefer to purchase almond flour alongside other grocery items. Additionally, supermarkets and hypermarkets often offer a wide variety of brands and types of almond flour, allowing consumers to easily compare products and prices.

The large number of shoppers visiting supermarkets and hypermarkets regularly makes this channel the largest subsegment in the distribution of almond flour. Furthermore, the increasing consumer demand for gluten-free and health-conscious products has led to an expansion of almond flour offerings in these retail stores. As more consumers prioritize health and wellness, supermarkets and hypermarkets will continue to be the primary distribution channel for almond flour.

Bakery Products Application Is Largest Due to Growing Demand for Healthy Baked Goods

Almond flour is increasingly being used in the preparation of bakery products, making this the largest application segment in the almond flour market. With the rising demand for gluten-free, low-carb, and high-protein foods, almond flour has gained popularity as a substitute for traditional wheat flour in various baked goods. Its ability to provide a delicate, moist texture without compromising on flavor has made it a staple ingredient in cakes, cookies, muffins, and other baked items. The growing trend of healthier eating habits is driving the demand for almond flour in bakery applications, as consumers seek nutritious alternatives to conventional baked goods.

The bakery products application will continue to be the largest subsegment in the almond flour market. As consumers become more health-conscious and focused on gluten-free and low-carb diets, the need for almond flour in bakery products is expected to rise. This trend is particularly prevalent in North America and Europe, where the demand for gluten-free and organic products is robust, encouraging bakeries and food manufacturers to incorporate almond flour into their offerings.

Food and Beverages End-Use Industry Is Largest Due to Expanding Health Trends

The food and beverages industry is the largest end-user of almond flour, driven by the increasing consumer demand for healthier, gluten-free, and plant-based food products. Almond flour is used in a wide range of food products, from baked goods to snacks, beverages, and even dairy alternatives. As consumers prioritize health-conscious diets, the demand for ingredients like almond flour, known for its high protein and low carbohydrate content, has surged. Additionally, almond flour is becoming a common ingredient in plant-based and dairy-free alternatives, further expanding its use in the food and beverages industry.

The food and beverages segment will continue to dominate the almond flour market due to its broad application across a variety of product categories. The growing trend of clean label products, where consumers look for natural, minimally processed ingredients, will also drive the demand for almond flour. As the focus on health and wellness grows globally, the food and beverages industry will remain the largest consumer of almond flour.

North America Region Is Largest Due to High Demand for Gluten-Free Products

In terms of regional growth, North America holds the largest share of the almond flour market. The region is home to a large population of health-conscious consumers who are increasingly adopting gluten-free, low-carb, and high-protein diets. North America's strong preference for plant-based and organic food products has significantly boosted the demand for almond flour, making it a key ingredient in a variety of food products. Additionally, the region's advanced retail infrastructure, including supermarkets, hypermarkets, and e-commerce platforms, has made it easier for consumers to access almond flour.

North America’s dominance in the almond flour market is expected to continue as the trend of healthy eating and gluten-free diets grows. The U.S., in particular, is the largest market for almond flour, driven by both consumer demand and the growing popularity of almond-based products in the food and beverage industry. As the demand for clean-label and gluten-free products continues to rise, the North American almond flour market is set to expand further.

Leading Companies and Competitive Landscape

The almond flour market is highly competitive, with several key players leading the way in product innovation, distribution, and consumer outreach. Companies like Blue Diamond Growers, Bob’s Red Mill Natural Foods, and Honeyville are some of the largest players in the market, known for their high-quality almond flour products and strong brand presence. These companies leverage strategic partnerships, strong distribution networks, and innovation in product offerings to maintain their market leadership.

The competitive landscape is also marked by an increasing focus on organic and clean-label products, with companies introducing new almond flour variants that cater to the growing health-conscious consumer base. As demand for gluten-free and low-carb products continues to rise, companies are focusing on expanding their product portfolios and improving production efficiency. Furthermore, with the growing popularity of e-commerce, companies are increasingly investing in online sales channels to reach a wider consumer base, positioning themselves for continued growth in the almond flour market.

Recent Developments:

- Bob’s Red Mill recently introduced new almond flour blends, expanding its range of gluten-free baking products to cater to growing consumer demand for healthy alternatives.

- Blue Diamond Growers has signed new distribution agreements with major supermarket chains in North America, increasing its presence in the almond flour market.

- Honeyville has expanded its distribution network in Europe and Asia, increasing its market footprint and meeting the rising demand for gluten-free baking ingredients.

- Cargill has acquired an almond processing facility in California to enhance its supply chain and improve the production efficiency of almond-based products, including almond flour.

- Nature’s Eats announced that its almond flour line has received organic certification, catering to the increasing preference for organic and clean-label food products.

List of Leading Companies:

- Blue Diamond Growers

- Nature's Eats

- Honeyville

- Wellness Bakeries

- Bob’s Red Mill Natural Foods

- King Arthur Baking Company

- The Real Almond Company

- Anthony's Goods

- Almonds Australia

- Lydia’s Organics

- Cargill, Incorporated

- Bunge Limited

- Mariani Nut Company

- Flourish Baking Co.

- Living Tree Community Foods

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.8 Billion |

|

Forecasted Value (2030) |

USD 3.3 Billion |

|

CAGR (2024 – 2030) |

9.5% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Almond Flour Market By Product Type (Blanched Almond Flour, Unblanched Almond Flour), By Distribution Channel (Supermarkets/Hypermarkets, Online Retailers, Specialty Stores, Convenience Stores), By Application (Bakery Products, Snacks and Confectionery, Dairy Products, Beverages), By End-Use Industry (Food and Beverages, Personal Care and Cosmetics, Pharmaceuticals) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Blue Diamond Growers, Nature's Eats, Honeyville, Wellness Bakeries, Bob’s Red Mill Natural Foods, King Arthur Baking Company, The Real Almond Company, Anthony's Goods, Almonds Australia, Lydia’s Organics, Cargill, Incorporated, Bunge Limited, Mariani Nut Company, Flourish Baking Co., Living Tree Community Foods |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Almond Flour Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Blanched Almond Flour |

|

4.2. Unblanched Almond Flour |

|

5. Almond Flour Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Supermarkets/Hypermarkets |

|

5.2. Online Retailers |

|

5.3. Specialty Stores |

|

5.4. Convenience Stores |

|

6. Almond Flour Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Bakery Products |

|

6.2. Snacks and Confectionery |

|

6.3. Dairy Products |

|

6.4. Beverages |

|

6.5. Others (Cosmetics, Nutritional Supplements) |

|

7. Almond Flour Market, by End-Use Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Food and Beverages |

|

7.2. Personal Care and Cosmetics |

|

7.3. Pharmaceuticals |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Almond Flour Market, by Product Type |

|

8.2.7. North America Almond Flour Market, by Distribution Channel |

|

8.2.8. North America Almond Flour Market, by Application |

|

8.2.9. North America Almond Flour Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Almond Flour Market, by Product Type |

|

8.2.10.1.2. US Almond Flour Market, by Distribution Channel |

|

8.2.10.1.3. US Almond Flour Market, by Application |

|

8.2.10.1.4. US Almond Flour Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Blue Diamond Growers |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Nature's Eats |

|

10.3. Honeyville |

|

10.4. Wellness Bakeries |

|

10.5. Bob’s Red Mill Natural Foods |

|

10.6. King Arthur Baking Company |

|

10.7. The Real Almond Company |

|

10.8. Anthony's Goods |

|

10.9. Almonds Australia |

|

10.10. Lydia’s Organics |

|

10.11. Cargill, Incorporated |

|

10.12. Bunge Limited |

|

10.13. Mariani Nut Company |

|

10.14. Flourish Baking Co. |

|

10.15. Living Tree Community Foods |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Almond Flour Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Almond Flour Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Almond Flour Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA