As per Intent Market Research, the Allergic Asthma Therapeutics Market was valued at USD 18.6 Billion in 2024-e and will surpass USD 32.7 Billion by 2030; growing at a CAGR of 9.9% during 2025-2030.

The allergic asthma therapeutics market is growing rapidly as the global prevalence of asthma continues to rise, particularly among children and young adults. Asthma is a chronic respiratory condition characterized by inflammation and narrowing of the airways, making it difficult to breathe. Allergic asthma, in which allergens such as pollen, dust mites, and animal dander trigger asthma symptoms, is one of the most common forms. The market for therapeutic solutions is expanding due to the increasing need for effective treatments, advancements in pharmaceutical research, and the growing understanding of the immunological mechanisms involved in asthma. Additionally, new and improved treatment options are helping to manage symptoms, reduce inflammation, and improve quality of life for patients.

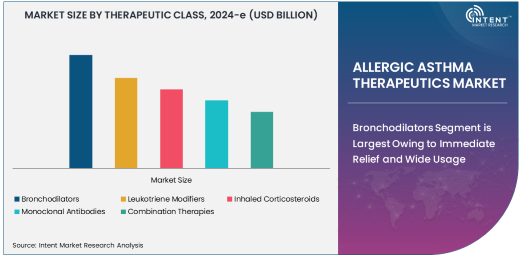

Among the key therapeutic classes, bronchodilators, leukotriene modifiers, inhaled corticosteroids, monoclonal antibodies, and combination therapies are commonly used in the management of allergic asthma. As healthcare providers continue to personalize treatment regimens based on the severity of the disease, the demand for a variety of treatment options across different age groups and asthma severities is driving the growth of this market. Furthermore, the increasing focus on patient-friendly administration methods such as inhalation devices and oral medications, along with the rise of biologics, is making it easier for patients to manage their condition effectively.

Bronchodilators Segment is Largest Owing to Immediate Relief and Wide Usage

Among the different therapeutic classes, bronchodilators are the largest segment within the allergic asthma therapeutics market. Bronchodilators work by relaxing the muscles around the airways, allowing them to open up and making it easier for patients to breathe. This class of drugs is widely used to provide quick relief during asthma attacks or to manage symptoms on a daily basis. Short-acting beta-agonists (SABAs) and long-acting beta-agonists (LABAs) are the two primary types of bronchodilators, with SABAs providing fast relief and LABAs offering longer-term control of symptoms.

The popularity of bronchodilators is due to their ability to deliver rapid and effective relief from acute asthma symptoms. They are often used as rescue medications, making them an essential part of asthma treatment plans. The increasing number of asthma cases globally, coupled with the need for quick symptom relief, has made bronchodilators a staple in the management of allergic asthma. Their availability in both inhalation and oral forms further enhances their accessibility, ensuring that they remain the most widely prescribed treatment for asthma, especially in emergency and outpatient settings.

Inhaled Corticosteroids Are the Fastest Growing Segment Due to Long-Term Control Benefits

Inhaled corticosteroids (ICS) are the fastest-growing therapeutic class within the allergic asthma therapeutics market, largely because of their effectiveness in providing long-term asthma control. ICS are considered the first-line treatment for persistent asthma due to their ability to reduce inflammation and prevent asthma exacerbations. By delivering medication directly to the lungs, ICS can reduce swelling and mucus production in the airways, helping to prevent both acute symptoms and long-term damage to lung function.

The rising preference for ICS is driven by their proven efficacy in improving asthma control, particularly in patients with moderate to severe asthma. As patients and healthcare providers increasingly focus on preventive care to reduce the frequency of asthma attacks, the demand for ICS is growing. Furthermore, the availability of advanced inhalation devices that ensure better drug delivery and patient compliance has also contributed to the expansion of this market segment. As part of personalized asthma management strategies, ICS are often combined with other medications to maximize therapeutic outcomes.

Monoclonal Antibodies Segment is Expanding Due to Targeted Therapy

The monoclonal antibodies segment is expanding rapidly in the allergic asthma therapeutics market, driven by the growing interest in biologic therapies for asthma management. Monoclonal antibodies, such as omalizumab and mepolizumab, are designed to target specific molecules involved in the inflammatory process of asthma, such as immunoglobulin E (IgE) or interleukin-5 (IL-5). These drugs offer a more targeted approach to treating allergic asthma, especially in patients with severe or difficult-to-control asthma who do not respond well to traditional therapies.

Biologics have revolutionized the treatment of allergic asthma by addressing the underlying causes of inflammation rather than merely alleviating symptoms. The increased availability of these targeted therapies and their ability to provide lasting relief for patients with severe asthma has driven the adoption of monoclonal antibodies in clinical practice. As the understanding of asthma pathophysiology deepens and more biologic treatments are developed, this segment is expected to experience continued growth, further enhancing the precision and effectiveness of asthma management.

Oral Administration Route Is Preferred Due to Convenience and Ease of Use

Among the various routes of administration, oral medications are increasingly preferred by patients with allergic asthma due to their convenience and ease of use. Oral medications, such as leukotriene modifiers and corticosteroids, offer the advantage of being easy to take, especially for patients who may have difficulty using inhalation devices or for those who prefer a non-invasive treatment option. Oral therapies also provide the flexibility of at-home management, reducing the need for frequent visits to healthcare providers.

The convenience of oral administration, combined with the effectiveness of oral drugs in managing asthma symptoms and inflammation, has made them a popular choice in asthma treatment regimens. While inhalation remains the preferred method for delivering certain medications directly to the lungs, the demand for oral treatments is increasing, particularly among patients seeking long-term control of their asthma. The development of new oral medications with improved efficacy and safety profiles is further contributing to the growth of this route in the allergic asthma therapeutics market.

Hospitals and Clinics Segment Dominates as the Primary Treatment Setting

The hospitals and clinics segment dominates the allergic asthma therapeutics market in terms of end-users, as these settings provide a comprehensive range of diagnostic and treatment options for asthma patients. Hospitals and clinics offer specialized care, including monitoring, diagnosis, and access to a variety of treatment options such as inhalers, bronchodilators, and biologic therapies. These facilities are typically the first point of contact for patients experiencing severe or acute asthma exacerbations, making them a central hub for asthma care.

Additionally, hospitals and clinics are equipped with trained healthcare professionals who can provide personalized treatment plans, ensuring that patients receive the most appropriate therapy based on the severity of their asthma. The demand for advanced asthma treatments, including monoclonal antibodies and inhaled corticosteroids, is high in these settings, further driving the growth of this segment. As healthcare infrastructure improves globally and the number of asthma cases continues to rise, hospitals and clinics are expected to remain the primary treatment setting for allergic asthma.

Online Pharmacies Are Gaining Popularity Due to Convenience

The online pharmacies segment is witnessing a significant surge in demand as more patients seek convenient and accessible ways to purchase asthma medications. Online pharmacies offer a wide range of therapeutic options, including bronchodilators, corticosteroids, and leukotriene modifiers, and provide the convenience of home delivery. With the growing trend of telemedicine and remote consultations, many patients now prefer to order their asthma medications online, especially for long-term management.

The growth of online pharmacies is also fueled by their ability to provide competitive pricing and quick access to medications. As the global e-commerce market expands and consumers increasingly prioritize convenience and ease of access, online pharmacies are becoming an increasingly important distribution channel for allergic asthma therapeutics. This trend is expected to continue, further transforming the way asthma medications are purchased and distributed.

North America Dominates the Allergic Asthma Therapeutics Market

North America holds the largest share of the allergic asthma therapeutics market, primarily driven by the high prevalence of asthma, particularly in the United States. The region benefits from advanced healthcare infrastructure, high awareness levels about asthma, and strong research and development capabilities. The U.S. market, in particular, is well-established with a wide variety of available treatments, including inhaled corticosteroids, bronchodilators, and biologics such as monoclonal antibodies, which are gaining increasing adoption.

Moreover, the high spending on healthcare, a favorable reimbursement system, and the presence of key pharmaceutical companies such as GlaxoSmithKline, AstraZeneca, and Novartis contribute to North America's dominance. The rise in asthma prevalence, especially among children, is pushing the demand for more effective and personalized treatment options. As a result, North America is expected to maintain its lead in the market throughout the forecast period.

Competitive Landscape and Leading Companies

The allergic asthma therapeutics market is highly competitive, with several key players driving innovation and expanding their product portfolios to meet the growing demand for effective asthma treatments. Leading companies in this space include GlaxoSmithKline, AstraZeneca, Novartis, Boehringer Ingelheim, and Teva Pharmaceuticals, which are focused on developing new and improved therapies, including biologics and combination treatments.

The competitive landscape is characterized by the ongoing development of novel treatments, strategic partnerships, and mergers and acquisitions as companies seek to strengthen their market position. With a growing emphasis on personalized medicine, many companies are also investing in research and development to introduce new drug delivery systems and improve patient outcomes. As the market for allergic asthma therapeutics continues to expand, companies that can offer innovative solutions and meet the evolving needs of asthma patients will be well-positioned to lead the market.

Recent Developments:

- GlaxoSmithKline plc launched a new inhaled corticosteroid for the treatment of moderate to severe allergic asthma in the US market.

- AstraZeneca PLC announced the approval of a new monoclonal antibody therapy for allergic asthma in Europe.

- Novartis International AG expanded its portfolio of asthma treatments by acquiring a new biologic for severe allergic asthma management.

- Sanofi S.A. unveiled a combination therapy for allergic asthma, designed to reduce the frequency of asthma attacks in children and adults.

- Boehringer Ingelheim International GmbH received FDA approval for its new long-acting beta-agonist inhaler for the treatment of allergic asthma.

List of Leading Companies:

- GlaxoSmithKline plc

- AstraZeneca PLC

- Novartis International AG

- Sanofi S.A.

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc.

- Teva Pharmaceutical Industries Ltd.

- Johnson & Johnson

- Regeneron Pharmaceuticals, Inc.

- Roche Holding AG

- Eli Lilly and Company

- Mylan N.V.

- Pfizer Inc.

- AbbVie Inc.

- Amgen Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 18.6 Billion |

|

Forecasted Value (2030) |

USD 32.7 Billion |

|

CAGR (2025 – 2030) |

9.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Allergic Asthma Therapeutics Market By Therapeutic Class (Bronchodilators: Short-Acting Beta-Agonists, Long-Acting Beta-Agonists, Leukotriene Modifiers, Inhaled Corticosteroids, Monoclonal Antibodies, Combination Therapies), By Route of Administration (Inhalation, Oral), By End-User (Hospitals and Clinics, Homecare Settings), and By Distribution Channel (Direct Sales, Retail Pharmacies, Online Pharmacies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

GlaxoSmithKline plc, AstraZeneca PLC, Novartis International AG, Sanofi S.A., Boehringer Ingelheim International GmbH, Merck & Co., Inc., Teva Pharmaceutical Industries Ltd., Johnson & Johnson, Regeneron Pharmaceuticals, Inc., Roche Holding AG, Eli Lilly and Company, Mylan N.V., Pfizer Inc., AbbVie Inc., Amgen Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Allergic Asthma Therapeutics Market, by Type of Vehicle (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Passenger Vehicles |

|

4.2. Commercial Vehicles |

|

5. Allergic Asthma Therapeutics Market, by Drive Configuration (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Full-Time All-Wheel Drive (AWD) |

|

5.2. Part-Time All-Wheel Drive (AWD) |

|

6. Allergic Asthma Therapeutics Market, by Powertrain Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Electric All-Wheel Drive |

|

6.2. Hybrid All-Wheel Drive |

|

6.3. Internal Combustion Engine (ICE) All-Wheel Drive |

|

7. Allergic Asthma Therapeutics Market, by Sales Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. OEM (Original Equipment Manufacturer) |

|

7.2. Aftermarket |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Allergic Asthma Therapeutics Market, by Type of Vehicle |

|

8.2.7. North America Allergic Asthma Therapeutics Market, by Drive Configuration |

|

8.2.8. North America Allergic Asthma Therapeutics Market, by Powertrain Type |

|

8.2.9. North America Allergic Asthma Therapeutics Market, by Sales Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Allergic Asthma Therapeutics Market, by Type of Vehicle |

|

8.2.10.1.2. US Allergic Asthma Therapeutics Market, by Drive Configuration |

|

8.2.10.1.3. US Allergic Asthma Therapeutics Market, by Powertrain Type |

|

8.2.10.1.4. US Allergic Asthma Therapeutics Market, by Sales Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. GlaxoSmithKline plc |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. AstraZeneca PLC |

|

10.3. Novartis International AG |

|

10.4. Sanofi S.A. |

|

10.5. Boehringer Ingelheim International GmbH |

|

10.6. Merck & Co., Inc. |

|

10.7. Teva Pharmaceutical Industries Ltd. |

|

10.8. Johnson & Johnson |

|

10.9. Regeneron Pharmaceuticals, Inc. |

|

10.10. Roche Holding AG |

|

10.11. Eli Lilly and Company |

|

10.12. Mylan N.V. |

|

10.13. Pfizer Inc. |

|

10.14. AbbVie Inc. |

|

10.15. Amgen Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Allergic Asthma Therapeutics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Allergic Asthma Therapeutics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Allergic Asthma Therapeutics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA