As per Intent Market Research, the Alcoholic Beverages Market was valued at USD 1,457.3 Billion in 2024-e and will surpass USD 2,197.1 Billion by 2030; growing at a CAGR of 7.1% during 2025-2030.

The alcohol market continues to experience substantial growth, driven by diverse consumer preferences across different regions. From casual drinkers to connoisseurs, alcohol consumption is an ingrained part of social and cultural experiences globally. The industry is segmented into various types such as beer, wine, spirits, and others, each with its unique appeal and consumer base. With the increasing availability of alcohol through both traditional and modern distribution channels, the market is expected to grow steadily, catering to the varying demands of consumers.

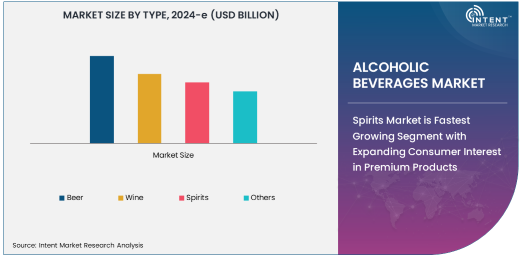

Among these segments, beer remains the largest in the alcohol market. Its enduring popularity, especially in social settings and casual consumption, ensures its dominance. Beer is widely consumed across different age groups, and its variety—ranging from light to dark beers, craft varieties, and international brands—ensures broad appeal. Beer’s availability in both on-trade (bars, restaurants, clubs) and off-trade (supermarkets, liquor stores, online retail) channels has further cemented its position as the largest product type in the market. Furthermore, beer’s strong presence in major global markets, particularly in Europe, North America, and parts of Asia, contributes to its leadership position in the overall alcohol industry.

Spirits Market is Fastest Growing Segment with Expanding Consumer Interest in Premium Products

While beer dominates the alcohol market in terms of volume, the spirits segment is the fastest growing. The spirits category, encompassing whiskey, vodka, rum, tequila, gin, brandy, cognac, and others, is gaining popularity due to increasing consumer interest in premium, artisanal, and craft beverages. This growth is particularly notable among younger, affluent consumers seeking unique and high-quality alcoholic products. A shift toward high-end and luxury brands in spirits, especially whiskey, vodka, and gin, is contributing significantly to the segment's rapid expansion.

Whiskey is particularly noteworthy within the spirits category, experiencing strong growth globally, driven by its premiumization trend. Consumers are increasingly seeking aged, single malt, and small-batch whiskey, which is driving higher sales and growth. Additionally, the rise of craft distilleries and innovation in flavored spirits is attracting a new generation of drinkers, further boosting the spirits segment's growth. As more consumers shift towards premium and luxury spirits, the category is expected to maintain its rapid pace of expansion in the coming years.

Online Retail is the Fastest Growing Distribution Channel for Alcohol Sales

The distribution channels for alcohol are vast, ranging from traditional on-trade outlets such as bars and restaurants to off-trade locations like supermarkets and liquor stores. Among these channels, online retail is emerging as the fastest growing segment. The ease of purchasing alcohol from the comfort of home, combined with a wider selection of products and convenience, has contributed to the rapid adoption of online alcohol sales. Both direct online sales from brand websites and marketplace platforms are capitalizing on this trend, offering consumers a seamless shopping experience.

As digital commerce continues to expand, alcohol sales through online platforms are seeing accelerated growth, particularly during the COVID-19 pandemic, which accelerated the adoption of e-commerce across various sectors. Consumers are increasingly drawn to the convenience of ordering alcoholic beverages online, with many services offering home delivery. The online channel also appeals to consumers seeking niche products or exclusive international brands that may not be available in local retail stores. With e-commerce continuing to grow globally, online retail will remain a key distribution channel for alcohol in the foreseeable future.

Hospitality and Tourism Industry is the Largest End-Use Segment for Alcohol

The hospitality and tourism industry is the largest end-use segment for alcohol, as bars, restaurants, hotels, and resorts serve as primary consumption venues. Alcoholic beverages are integral to socializing and entertainment, making them a key part of the dining and travel experiences. The rise in global travel and tourism, coupled with the expanding number of hospitality venues, has driven steady demand for alcohol. In particular, regions like Europe and North America, known for their strong hospitality industries, are major consumers of alcohol in this segment.

As the hospitality industry evolves, there is an increasing demand for higher-quality alcoholic beverages, especially premium wines, spirits, and craft beers. Additionally, the rise in “mixology” and the demand for unique cocktail experiences is contributing to the popularity of certain types of alcohol, such as gin and tequila. The tourism sector also plays a crucial role in driving alcohol sales, with bars and restaurants catering to both local customers and international tourists. This ensures that the hospitality and tourism sector remains a cornerstone of alcohol consumption globally.

Asia-Pacific is the Fastest Growing Region in the Alcohol Market

Asia-Pacific is the fastest growing region in the alcohol market, driven by an expanding middle class, urbanization, and changing consumer preferences. Countries such as China, India, and Japan are witnessing significant growth in alcohol consumption, particularly in spirits and beer segments. While traditionally, alcohol consumption in some Asian countries was relatively low, the growing influence of Western culture and the rise of disposable incomes are driving an increased demand for alcohol products, including premium spirits.

The rapid growth of e-commerce in the region also supports the alcohol market, as consumers increasingly turn to online platforms for purchasing alcoholic beverages. Additionally, as disposable incomes rise and more people travel, the demand for premium and imported alcohol brands has surged. The Asia-Pacific market is expected to continue its strong growth trajectory, offering ample opportunities for market players to expand their presence in the region.

Competitive Landscape: Leading Players and Innovation Drive Growth

The alcohol market is highly competitive, with numerous global and regional players operating across various product categories. Major multinational companies such as Anheuser-Busch InBev, Diageo, Pernod Ricard, and Heineken dominate the beer and spirits sectors, leveraging their brand recognition and extensive distribution networks to capture market share. These companies are focused on product innovation, strategic mergers and acquisitions, and expanding into emerging markets to sustain growth.

The market is also witnessing a rise in niche players, particularly in the premium and craft alcohol categories. These players are introducing unique, high-quality products that cater to discerning consumers seeking novel experiences. The shift towards healthier and sustainable options, such as low-alcohol or organic beverages, is also shaping the competitive landscape. Overall, as consumer preferences evolve, companies will continue to innovate and diversify their offerings to stay ahead in this dynamic market.

Recent Developments:

- Anheuser-Busch InBev announced the launch of a new low-alcohol beer line aimed at health-conscious consumers.

- Diageo acquired a premium spirits brand to expand its product portfolio in the growing craft spirits segment.

- Heineken N.V. introduced a new alcohol-free beer variant targeting younger, health-conscious drinkers.

- Pernod Ricard launched a sustainability initiative, focusing on reducing carbon emissions and packaging waste across its product lines.

- Molson Coors Beverage Company revealed plans to expand its production capacity for non-alcoholic beverages, including hard seltzers and alcohol-free beers.

List of Leading Companies:

- Anheuser-Busch InBev

- Diageo

- Heineken N.V.

- Pernod Ricard

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings

- Suntory Holdings Limited

- Constellation Brands

- Kirin Holdings Company, Limited

- Bacardi Limited

- Brown-Forman Corporation

- Remy Cointreau

- The Boston Beer Company

- Hennessy (LVMH)

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1,457.3 Billion |

|

Forecasted Value (2030) |

USD 2,197.1 Billion |

|

CAGR (2025 – 2030) |

7.1% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Alcoholic Beverages Market By Type (Beer, Wine, Spirits {Whiskey, Vodka, Rum, Tequila, Gin, Brandy, Cognac}), By Distribution Channel (On-Trade {Bars, Restaurants, Clubs and Nightclubs}, Off-Trade {Supermarkets, Retail Stores, Liquor Stores}, Online Retail {Direct Online Sales, Marketplace Platforms}, Duty-Free {Airports, Cruise Ships, Train Stations}), and By End-Use Industries (Hospitality and Tourism, Retail and Consumer Goods, Event and Entertainment, Healthcare, Food and Beverage Manufacturing, Sports and Fitness, Bars and Nightclubs) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Anheuser-Busch InBev, Diageo, Heineken N.V., Pernod Ricard, Carlsberg Group, Molson Coors Beverage Company, Asahi Group Holdings, Suntory Holdings Limited, Constellation Brands, Kirin Holdings Company, Limited, Bacardi Limited, Brown-Forman Corporation, Remy Cointreau, The Boston Beer Company, Hennessy (LVMH) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Alcoholic Beverages Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Beer |

|

4.2. Wine |

|

4.3. Spirits |

|

4.3.1. Whiskey |

|

4.3.2. Vodka |

|

4.3.3. Rum |

|

4.3.4. Tequila |

|

4.3.5. Gin |

|

4.3.6. Brandy |

|

4.3.7. Cognac |

|

4.3.8. Others |

|

4.4. Others |

|

5. Alcoholic Beverages Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. On-Trade |

|

5.1.1. Bars |

|

5.1.2. Restaurants |

|

5.1.3. Clubs and Nightclubs |

|

5.2. Off-Trade |

|

5.2.1. Supermarkets |

|

5.2.2. Retail Stores |

|

5.2.3. Liquor Stores |

|

5.3. Online Retail |

|

5.3.1. Direct Online Sales |

|

5.3.2. Marketplace Platforms |

|

5.4. Duty-Free |

|

5.4.1. Airports |

|

5.4.2. Cruise Ships |

|

5.4.3. Train Stations |

|

5.5. Others |

|

6. Alcoholic Beverages Market, by End Use Industries (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitality and Tourism |

|

6.2. Retail and Consumer Goods |

|

6.3. Event and Entertainment |

|

6.4. Bars and Nightclubs |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Alcoholic Beverages Market, by Type |

|

7.2.7. North America Alcoholic Beverages Market, by Distribution Channel |

|

7.2.8. North America Alcoholic Beverages Market, by End Use Industries |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Alcoholic Beverages Market, by Type |

|

7.2.9.1.2. US Alcoholic Beverages Market, by Distribution Channel |

|

7.2.9.1.3. US Alcoholic Beverages Market, by End Use Industries |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Anheuser-Busch InBev |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Diageo |

|

9.3. Heineken N.V. |

|

9.4. Pernod Ricard |

|

9.5. Carlsberg Group |

|

9.6. Molson Coors Beverage Company |

|

9.7. Asahi Group Holdings |

|

9.8. Suntory Holdings Limited |

|

9.9. Constellation Brands |

|

9.10. Kirin Holdings Company, Limited |

|

9.11. Bacardi Limited |

|

9.12. Brown-Forman Corporation |

|

9.13. Remy Cointreau |

|

9.14. The Boston Beer Company |

|

9.15. Hennessy (LVMH) |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Alcoholic Beverages Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Alcoholic Beverages Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Alcoholic Beverages Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA