As per Intent Market Research, the Air Defense System Market was valued at USD 45.2 billion in 2023 and will surpass USD 62.5 billion by 2030; growing at a CAGR of 4.7% during 2024 - 2030.

The global air defense system market has been witnessing significant growth, driven by the increasing need for advanced defense solutions to counter evolving threats. As geopolitical tensions rise and the need to secure airspaces becomes paramount, countries across the world are heavily investing in cutting-edge air defense technologies. Air defense systems comprise various components, including missile systems, radars, command and control systems, and other related equipment. These systems are designed to detect, intercept, and neutralize incoming threats, whether they are missiles, aircraft, or unmanned aerial vehicles (UAVs).

Missile Defense Segment is Largest Owing to Growing Threats from Ballistic and Cruise Missiles

The missile defense subsegment within the air defense system market is currently the largest and is expected to maintain its dominance throughout the forecast period. The growing threat from ballistic and cruise missiles, particularly in conflict-prone regions, has necessitated the deployment of advanced missile defense systems by various governments. Countries such as the United States, China, and Russia have been at the forefront of missile defense technology development, focusing on both offensive and defensive missile capabilities.

This segment includes both short-range and long-range missile defense systems. Long-range missile defense systems, such as Terminal High Altitude Area Defense (THAAD) and Aegis Ballistic Missile Defense (BMD), are designed to detect and intercept ballistic missiles in their terminal phase, while short-range systems cater to localized threats. Continuous research and development in missile interception technologies, along with the growing need to protect strategic assets, will ensure the missile defense segment remains the largest contributor to the air defense system market's revenue.

Radar Systems Segment is Fastest Growing Owing to Demand for Advanced Detection Capabilities

Radar systems represent the fastest-growing segment in the air defense market, driven by the need for precise and real-time detection of aerial threats. The increasing sophistication of airborne threats, including stealth technologies and hypersonic weapons, has fueled demand for radar systems with enhanced detection range, accuracy, and the ability to operate in complex environments.

Modern radars like Active Electronically Scanned Array (AESA) technology are gaining popularity due to their ability to simultaneously track multiple targets and their resilience against electronic warfare. AESA radars, in particular, are expected to witness rapid adoption in military air defense systems because of their multi-functional capabilities. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into radar systems will further enhance their detection capabilities, contributing to their rapid market growth.

Command and Control Systems Segment is Largest Owing to Network-Centric Warfare Needs

Command and control (C2) systems form the backbone of modern air defense strategies, acting as the central nodes that connect various components of the air defense infrastructure. The C2 segment is the largest within the air defense system market due to the increasing importance of network-centric warfare. The ability to integrate data from multiple sensors, radars, and missile systems into a centralized command hub allows for faster and more efficient decision-making in real-time combat scenarios.

The demand for highly secure and resilient C2 systems is growing, particularly in regions with heightened defense concerns. As nations enhance their air defense networks, interoperability between different branches of the military and their allies is becoming crucial. These systems enable multi-layered air defense operations, making them indispensable in modern warfare environments. Countries are heavily investing in upgrading their command and control infrastructures to ensure seamless communication and coordination during military operations.

Unmanned Aerial Vehicles (UAV) Defense Segment is Fastest Growing Owing to Proliferation of Drones

The UAV defense segment is emerging as one of the fastest-growing in the air defense system market, driven by the rapid proliferation of drones in both military and civilian applications. The increasing use of UAVs for surveillance, reconnaissance, and combat roles by both state and non-state actors has led to a significant rise in demand for counter-UAV systems. These defense systems are designed to detect, track, and neutralize hostile drones before they can pose a threat.

With the growing trend of drone swarming tactics, defense contractors are developing advanced counter-UAV solutions that combine radar, electro-optical systems, and jamming technologies. High-energy laser systems, capable of disabling or destroying drones, are also gaining traction in this segment. As the threat posed by UAVs continues to rise, especially in conflict zones and near sensitive military installations, the UAV defense subsegment is set to expand rapidly.

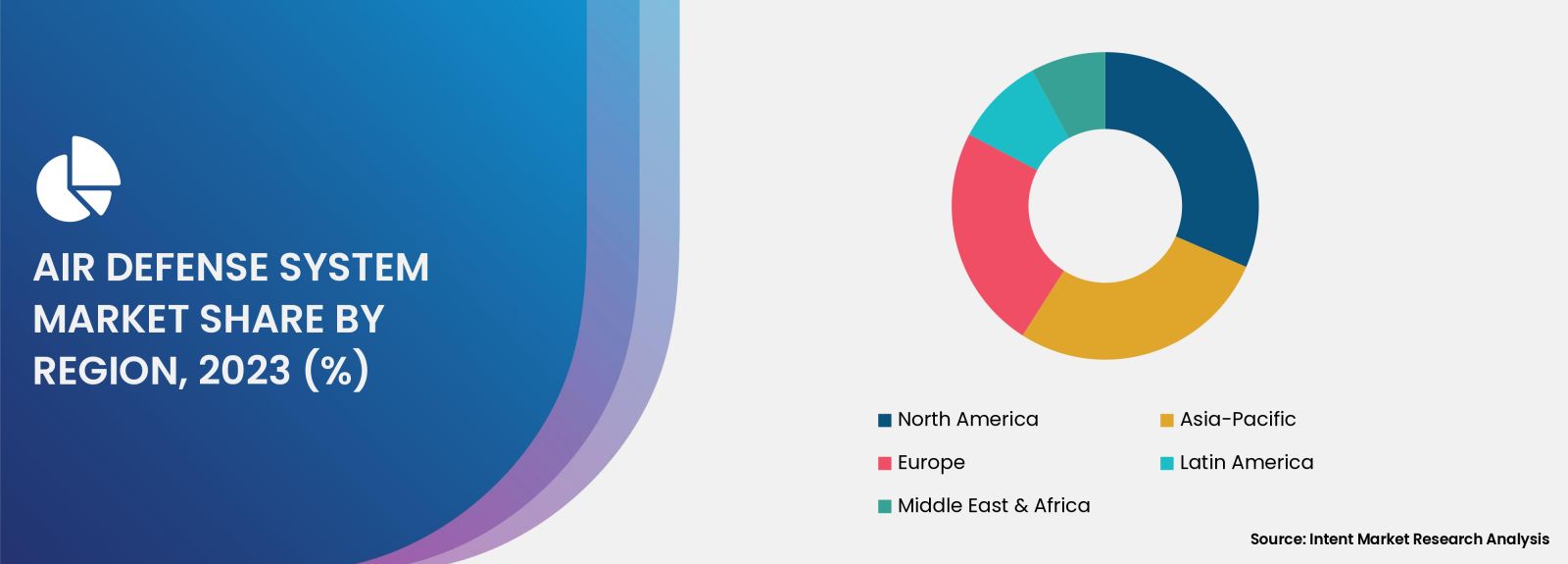

North America is Largest Region Owing to Strong Defense Investments and Technological Advancements

North America holds the largest share of the global air defense system market, driven by substantial investments in defense infrastructure and technological advancements. The United States, in particular, has consistently maintained high defense budgets to ensure air superiority, with a significant portion allocated to developing and procuring advanced air defense systems. The U.S. Department of Defense's focus on modernizing missile defense and radar systems to counter emerging threats has been a major factor in the region's dominance.

In addition to defense spending, North America's strong defense industrial base, characterized by leading defense contractors like Lockheed Martin, Raytheon Technologies, and Northrop Grumman, contributes to the region's leadership in the market. These companies are at the forefront of innovation in air defense systems, continually developing cutting-edge technologies that are sought after by governments worldwide. The presence of robust research and development initiatives and the growing demand for new generation defense technologies further solidify North America's leading position in the air defense system market.

Competitive Landscape and Leading Companies

The air defense system market is characterized by intense competition, with several leading defense contractors vying for contracts from governments worldwide. Key players in the market include Lockheed Martin Corporation, Raytheon Technologies, Northrop Grumman, and Thales Group. These companies dominate the market through their wide product portfolios, cutting-edge technologies, and long-standing relationships with major defense departments globally.

The competitive landscape is shaped by continuous innovation, with companies investing heavily in research and development to maintain a technological edge. Strategic collaborations and partnerships are also common, as defense firms seek to strengthen their global footprint. Additionally, the market is witnessing increasing consolidation as larger players acquire smaller specialized companies to enhance their capabilities. The focus on developing multi-layered air defense systems capable of countering a wide array of threats is a key trend driving competition in the market.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 45.2 billion |

|

Forecasted Value (2030) |

USD 62.5 billion |

|

CAGR (2024 – 2030) |

4.7% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Air Defense System Market By Type (Missile Defense System, Anti-Aircraft System, Counter Rocket, Artillery, and Mortar (C-RAM) System), By Component (Weapon System, Fire Control System, Command and Control System), By Range (Long Range Air Defense (LRAD) System, Medium Range Air Defense (MRAD) System, Short Range Air Defense (SHORAD) System), By Platform (Airborne, Land, Naval) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3.Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Air Defense System Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Missile Defense System |

|

4.2. Anti-Aircraft System |

|

4.3. Counter Rocket, Artillery, and Mortar (C-RAM) System |

|

5. Air Defense System Market, by Component (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Weapon System |

|

5.1.1. Gun / Turret System |

|

5.1.1.1. 20 mm |

|

5.1.1.2. 23 mm |

|

5.1.1.3. 25 mm |

|

5.1.1.4. 30 mm |

|

5.1.1.5. 35 mm |

|

5.1.2. Missile Launcher |

|

5.2. Fire Control System |

|

5.2.1. Air Defense Radar |

|

5.2.1.1. Fire Control Radar |

|

5.2.1.2. Surveillance Radar |

|

5.2.2. Electro-Optic Sensor and Laser Range Finder |

|

5.3. Command and Control System |

|

5.4. Others |

|

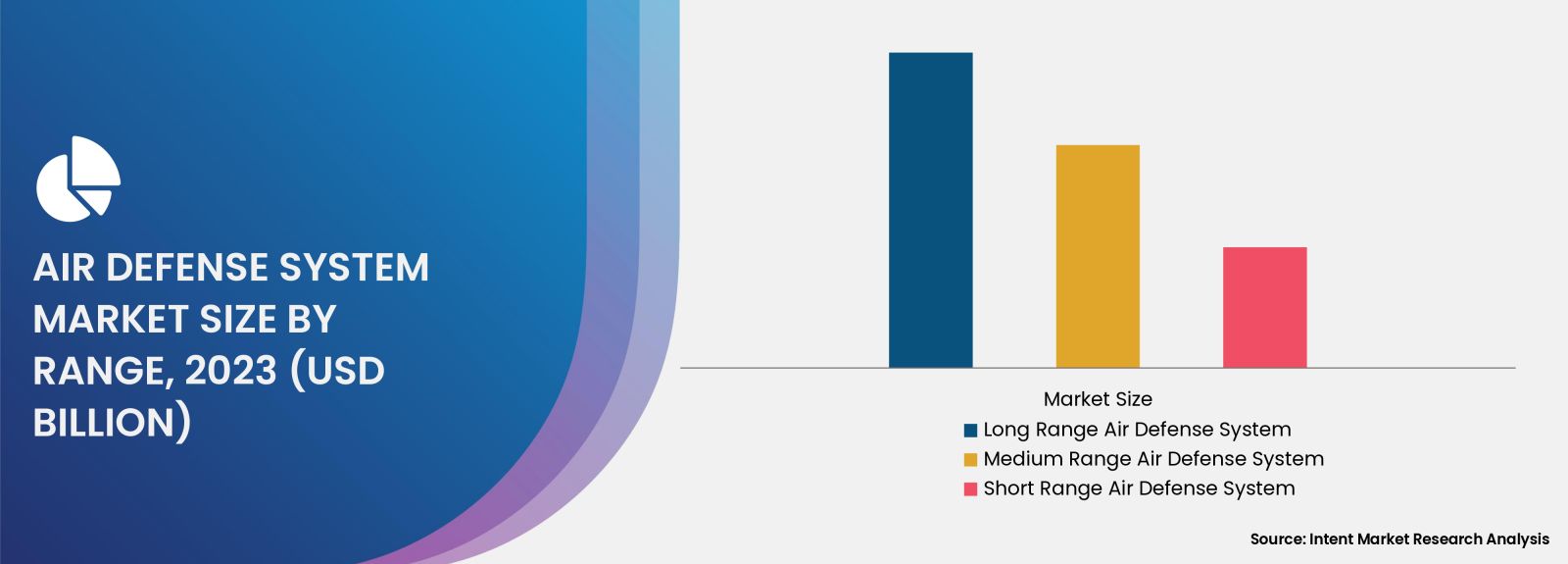

6. Air Defense System Market, by Range (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Long Range Air Defense (LRAD) System |

|

6.2. Medium Range Air Defense (MRAD) System |

|

6.3. Short Range Air Defense (SHORAD) System |

|

7. Air Defense System Market, by Platform (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Airborne |

|

7.2. Land |

|

7.3. Naval |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Air Defense System Market, by Type |

|

8.2.7. North America Air Defense System Market, by Component |

|

8.2.8. North America Air Defense System Market, by Range |

|

8.2.9. North America Air Defense System Market, by Platform |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Air Defense System Market, by Type |

|

8.2.10.1.2. US Air Defense System Market, by Component |

|

8.2.10.1.3. US Air Defense System Market, by Range |

|

8.2.10.1.4. US Air Defense System Market, by Platform |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. BAE Systems PLC |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Hanwha Systems Co., Ltd. |

|

10.3. Israel Aerospace Industries Ltd. |

|

10.4. Leonardo S.p.A. |

|

10.5. Lockheed Martin Corporation |

|

10.6. Northrop Grumman Corporation |

|

10.7. Rheinmetall AG |

|

10.8. RTX |

|

10.9. Saab |

|

10.10. THALES |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Air Defense System Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Air Defense System Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the Air Defense System ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Air Defense System Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Market Size Assessment

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA