As per Intent Market Research, the Air Data Indicator Market was valued at USD 657.9 Million in 2024-e and will surpass USD 944.9 Million by 2030; growing at a CAGR of 6.2% during 2025-2030.

The air data indicator market is crucial for ensuring the safety and efficiency of aircraft operations, providing pilots with essential real-time data on altitude, airspeed, vertical speed, and other critical parameters. These instruments are pivotal in navigation, flight performance monitoring, and situational awareness. As aviation continues to evolve with growing demand for safety and automation, the air data indicator market is witnessing sustained growth.

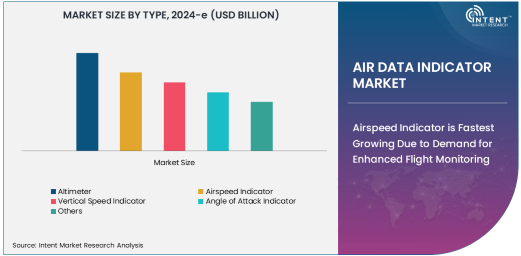

Altimeters are the largest product type in the market, due to their fundamental role in both commercial and military aviation. Altimeters measure the altitude of an aircraft, which is essential for flight control, navigation, and collision avoidance. In both commercial and military aviation, precise altitude measurement is critical for maintaining flight safety and ensuring adherence to air traffic control guidelines. The demand for advanced, reliable altimeters continues to increase, particularly with the rise in air traffic and the growing complexity of aircraft systems.

Airspeed Indicator is Fastest Growing Due to Demand for Enhanced Flight Monitoring

Airspeed indicators are experiencing the fastest growth in the air data indicator market. The growing emphasis on enhancing flight performance, fuel efficiency, and safety is driving the demand for more advanced airspeed indicators. These instruments help pilots monitor their airspeed, which is crucial for safe flight operations, particularly during take-off, cruising, and landing.

With the development of more sophisticated aircraft systems and the increasing adoption of automated and semi-automated flight controls, airspeed indicators are evolving to provide more accurate and real-time data. The rise of commercial aviation, as well as the introduction of advanced airspeed measurement technologies, is contributing to the rapid growth of this segment.

Commercial Aviation Leads Application Segment Due to High Demand for Air Data Indicators

Commercial aviation is the largest application segment in the air data indicator market. The growing global demand for air travel, alongside increasing passenger numbers, is driving the need for advanced air data indicators to ensure the safety and efficiency of aircraft. Commercial airlines, which operate a large fleet of aircraft, rely on air data indicators for precise and reliable measurements, ensuring smooth and safe operations across various flight phases.

As airlines continue to prioritize safety and regulatory compliance, the demand for accurate and robust air data indicator systems, including altimeters and airspeed indicators, is expected to remain high. Moreover, the trend toward incorporating next-generation avionics and automation in commercial aircraft further supports the continued dominance of this segment in the market.

North America Leads Market Due to Strong Aviation Infrastructure and Technology Advancements

North America holds the largest market share in the air data indicator market, primarily due to its well-established aviation infrastructure and high levels of technological innovation. The United States, with its large fleet of commercial, military, and general aviation aircraft, is a major contributor to the demand for air data indicators. The region’s focus on safety standards, aircraft modernization, and the growing demand for air travel continue to drive the market.

Moreover, the presence of leading aerospace manufacturers and avionics companies, such as Honeywell International, Collins Aerospace, and Rockwell Collins, further supports the dominance of North America in this market. The region’s regulatory environment, which enforces strict safety and performance standards, also bolsters the demand for advanced air data indicator systems.

Competitive Landscape: Technological Innovation and Strategic Partnerships Shape the Market

The air data indicator market is competitive, with key players such as Honeywell International, Thales Group, and Rockwell Collins leading the way. These companies focus on technological innovation, developing state-of-the-art air data indicator systems that offer enhanced accuracy, reliability, and integration with modern avionics systems.

Strategic partnerships with OEMs and MRO service providers are crucial for market growth, as these collaborations ensure that air data indicators are effectively integrated into new aircraft models and maintained throughout their lifecycle. Additionally, as the aviation industry moves toward automation and digitization, manufacturers are incorporating smart technologies, such as wireless connectivity and predictive maintenance capabilities, into their air data indicators to stay competitive. The market is expected to remain dynamic, driven by continuous advancements in aircraft technology and regulatory standards.

Recent Developments:

- Honeywell International Inc. launched an advanced air data indicator system with integrated digital displays for commercial aircraft.

- Collins Aerospace developed next-generation air data sensors designed for UAV applications.

- Thales Group announced a partnership to supply air data systems for a new fleet of military aircraft.

- Garmin Ltd. introduced a compact air data indicator for light and general aviation aircraft.

- Northrop Grumman Corporation unveiled an innovative air data module tailored for supersonic jets.

List of Leading Companies:

- Honeywell International Inc.

- Collins Aerospace (Raytheon Technologies)

- Thales Group

- Garmin Ltd.

- Northrop Grumman Corporation

- Safran Group

- Meggitt PLC

- Universal Avionics Systems Corporation

- L3Harris Technologies, Inc.

- AeroControlex Group

- Ametek, Inc.

- Rockwell Collins

- Esterline Technologies Corporation

- BAE Systems plc

- Dynon Avionics

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 657.9 Million |

|

Forecasted Value (2030) |

USD 944.9 Million |

|

CAGR (2025 – 2030) |

6.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Air Data Indicator Market By Type (Altimeter, Airspeed Indicator, Vertical Speed Indicator, Angle of Attack Indicator), By Application (Commercial Aviation, Military Aviation, General Aviation, Unmanned Aerial Vehicles (UAVs)), and By End-User (Original Equipment Manufacturers (OEMs), Maintenance, Repair & Overhaul (MRO)) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Honeywell International Inc., Collins Aerospace (Raytheon Technologies), Thales Group, Garmin Ltd., Northrop Grumman Corporation, Safran Group, Meggitt PLC, Universal Avionics Systems Corporation, L3Harris Technologies, Inc., AeroControlex Group, Ametek, Inc., Rockwell Collins, Esterline Technologies Corporation, BAE Systems plc, Dynon Avionics |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Air Data Indicator Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Altimeter |

|

4.2. Airspeed Indicator |

|

4.3. Vertical Speed Indicator |

|

4.4. Angle of Attack Indicator |

|

4.5. Others |

|

5. Air Data Indicator Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Commercial Aviation |

|

5.2. Military Aviation |

|

5.3. General Aviation |

|

5.4. Unmanned Aerial Vehicles (UAVs) |

|

5.5. Others |

|

6. Air Data Indicator Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Original Equipment Manufacturers (OEMs) |

|

6.2. Maintenance, Repair & Overhaul (MRO) |

|

6.3. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Air Data Indicator Market, by Type |

|

7.2.7. North America Air Data Indicator Market, by Application |

|

7.2.8. North America Air Data Indicator Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Air Data Indicator Market, by Type |

|

7.2.9.1.2. US Air Data Indicator Market, by Application |

|

7.2.9.1.3. US Air Data Indicator Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Honeywell International Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Collins Aerospace (Raytheon Technologies) |

|

9.3. Thales Group |

|

9.4. Garmin Ltd. |

|

9.5. Northrop Grumman Corporation |

|

9.6. Safran Group |

|

9.7. Meggitt PLC |

|

9.8. Universal Avionics Systems Corporation |

|

9.9. L3Harris Technologies, Inc. |

|

9.10. AeroControlex Group |

|

9.11. Ametek, Inc. |

|

9.12. Rockwell Collins |

|

9.13. Esterline Technologies Corporation |

|

9.14. BAE Systems plc |

|

9.15. Dynon Avionics |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Air Data Indicator Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Air Data Indicator Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Air Data Indicator Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA