As per Intent Market Research, the Agrochemicals Market was valued at USD 231.2 billion in 2023 and will surpass USD 286.5 billion by 2030; growing at a CAGR of 3.1% during 2024 - 2030.

The increasing global demand for food and the growing need for efficient farming techniques are propelling the agrochemicals market forward. As farmers face challenges related to pests, diseases, and soil fertility, agrochemicals play a crucial role in ensuring food supply stability and agricultural productivity. Furthermore, government initiatives and regulations promoting sustainable farming practices are encouraging the adoption of innovative agrochemical solutions. As the market evolves, the emphasis on environmentally friendly products and precision agriculture is expected to shape future trends in the agrochemicals sector.

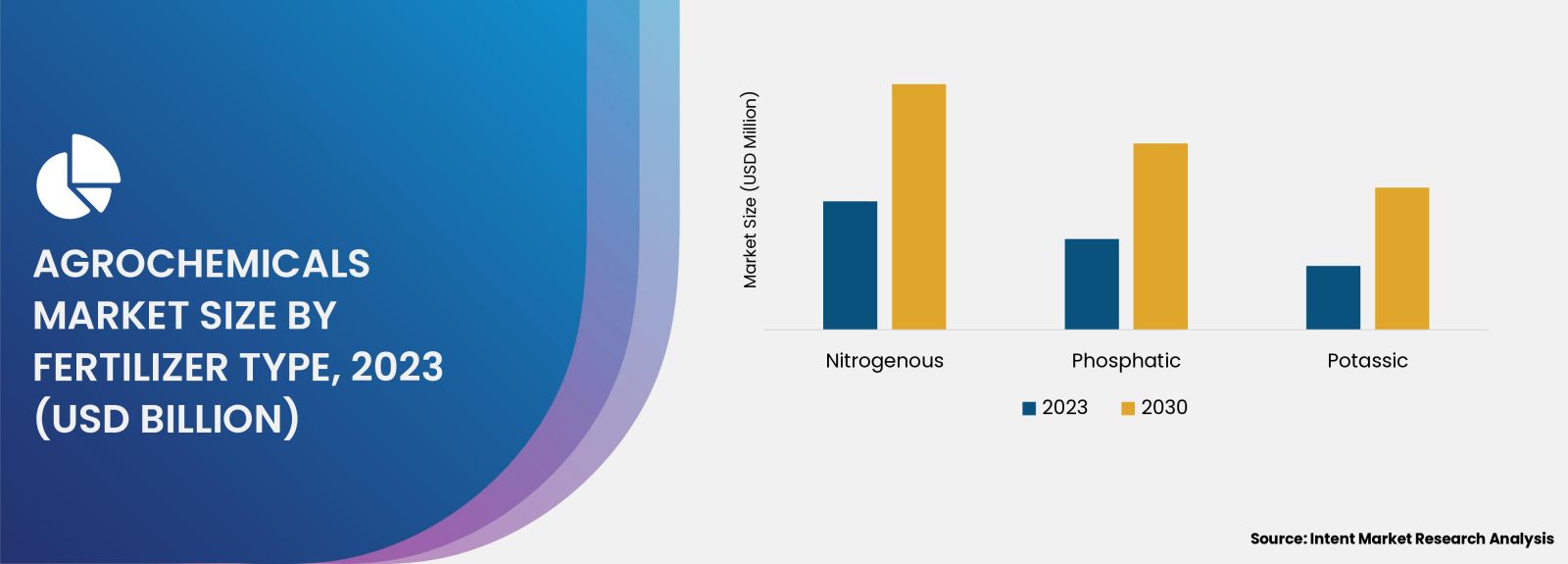

Fertilizers Segment is Largest Owing to Essential Nutrient Supply

The fertilizers segment constitutes the largest portion of the agrochemicals market, primarily due to the critical role fertilizers play in providing essential nutrients for crop growth. Fertilizers enhance soil fertility, improve crop yields, and contribute to higher food production, which is increasingly vital as the global population continues to rise. Within this segment, nitrogen-based fertilizers hold the largest market share, driven by their effectiveness in promoting plant growth and boosting agricultural productivity.

Nitrogen fertilizers, such as urea and ammonium nitrate, are widely used due to their high availability and efficiency in providing plants with the necessary nitrogen for photosynthesis and protein synthesis. As farmers strive to meet the increasing food demand, the adoption of nitrogen fertilizers is expected to remain strong. Additionally, advancements in slow-release and coated fertilizers are enhancing nutrient efficiency and reducing environmental impact, further solidifying the fertilizers segment's dominance in the agrochemicals market.

Pesticides Segment is Fastest Growing Owing to Increased Pest Resistance

The pesticides segment is the fastest-growing area within the agrochemicals market, driven by the increasing incidence of pest resistance and the need for effective crop protection solutions. With the rise of pest resistance to conventional pesticides, there is a growing demand for innovative and more efficient pesticide formulations. Integrated pest management (IPM) strategies, which combine biological, cultural, and chemical control methods, are gaining popularity, leading to the development of new pesticide products that are both effective and environmentally sustainable.

Biopesticides, a subsegment of pesticides derived from natural materials, are experiencing significant growth due to their reduced toxicity and lower environmental impact. As consumers increasingly prefer sustainably produced food, the demand for biopesticides is expected to rise. Furthermore, regulatory support for biopesticide development and the growing focus on organic farming practices are contributing to the rapid expansion of the pesticides segment in the agrochemicals market.

Herbicides Segment is Largest Owing to Weed Control Necessity

The herbicides segment is the largest within the agrochemicals market, primarily due to the crucial role herbicides play in weed management and crop protection. Effective weed control is essential for maximizing crop yields and reducing competition for nutrients, water, and sunlight. Glyphosate-based herbicides are among the most widely used products in this segment, offering broad-spectrum weed control for various crops. Their effectiveness and cost-efficiency have made them a staple for farmers worldwide.

Despite concerns regarding glyphosate's environmental impact, the herbicides segment continues to thrive as new formulations and application methods are developed to address these issues. The rise of herbicide-resistant crops is also driving innovation in this sector, leading to the introduction of novel herbicides that can be used in conjunction with these crops. As the demand for efficient weed control solutions grows, the herbicides segment is expected to maintain its significant presence in the agrochemicals market.

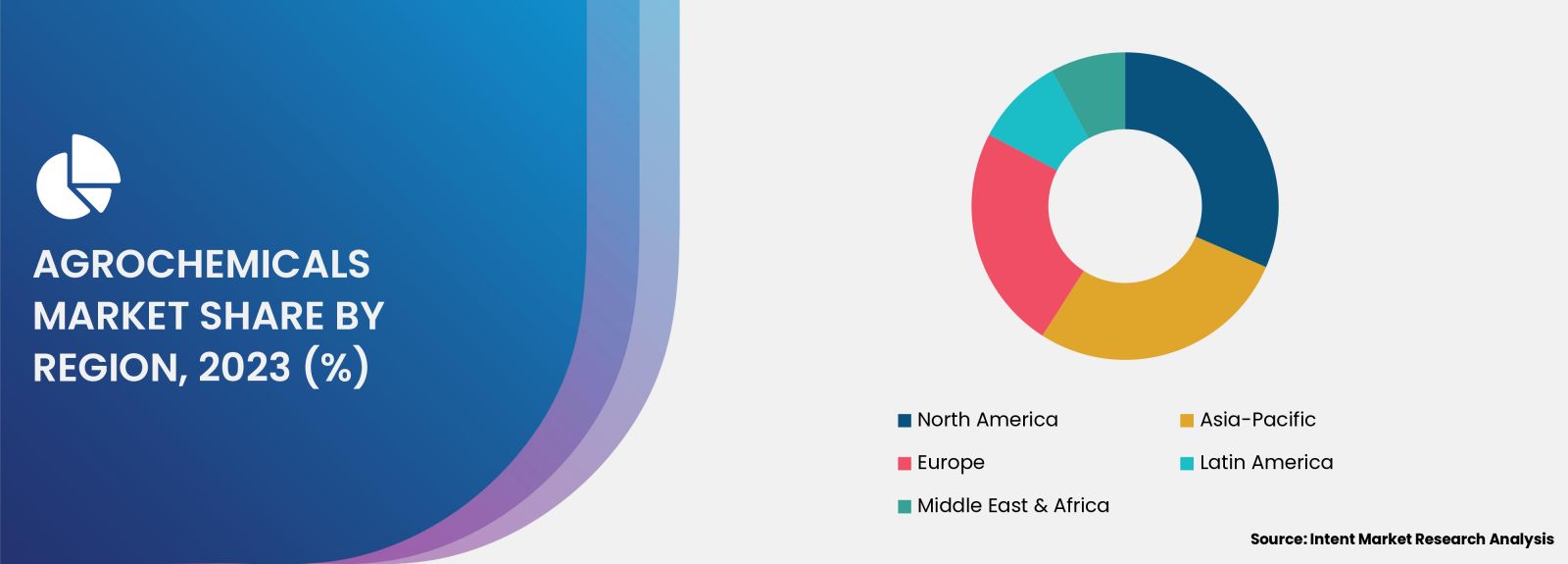

Asia-Pacific Region is Fastest Growing Owing to Agricultural Expansion

The Asia-Pacific region is the fastest-growing market for agrochemicals, driven by rapid agricultural expansion and increasing food demand. Countries like India and China are major contributors to this growth, as they seek to improve crop yields and enhance food security to support their large populations. The region's diverse agricultural landscape presents a unique opportunity for agrochemical companies to develop targeted products that cater to local needs.

Furthermore, the rise of precision agriculture and modern farming practices in Asia-Pacific is fostering the adoption of advanced agrochemical solutions. Governments in the region are also implementing policies to promote sustainable farming practices, which include the use of eco-friendly agrochemicals. As farmers become more aware of the benefits of agrochemicals in improving productivity and sustainability, the Asia-Pacific region is poised for significant growth in the agrochemicals market.

Competitive Landscape of Leading Companies

The agrochemicals market is characterized by a competitive landscape comprising several key players that dominate the industry. Prominent companies include:

- Bayer AG: A global leader in agricultural solutions, Bayer offers a comprehensive portfolio of crop protection products, seeds, and digital farming solutions.

- Syngenta AG: Known for its innovative crop protection and seed products, Syngenta focuses on enhancing agricultural productivity and sustainability.

- Corteva Agriscience: Specializing in seeds and crop protection, Corteva is committed to providing sustainable agricultural solutions to farmers worldwide.

- BASF SE: A major player in the agrochemicals sector, BASF offers a wide range of crop protection products and solutions for sustainable farming.

- FMC Corporation: FMC focuses on crop protection solutions, providing farmers with effective tools to manage pests and diseases.

- Nufarm Limited: Nufarm specializes in crop protection products, including herbicides, insecticides, and fungicides, catering to a diverse range of crops.

- Adama Agricultural Solutions Ltd.: Adama is known for its extensive portfolio of crop protection products, focusing on meeting the needs of farmers globally.

- Nutrien Ltd.: A leading provider of crop inputs and services, Nutrien offers a wide range of fertilizers and agrochemical products.

- Yara International ASA: Yara specializes in crop nutrition and offers a variety of fertilizers, contributing to sustainable agricultural practices.

- UPL Limited: UPL is a global player in the agrochemicals market, providing a comprehensive range of crop protection solutions and sustainable agricultural products.

These companies are actively engaged in research and development to innovate and expand their product offerings, focusing on sustainable solutions to meet the growing demand for food production. Collaborations, mergers, and acquisitions are common in the agrochemicals market, as firms seek to enhance their market presence and strengthen their competitive advantage. As sustainability becomes a key priority for the agricultural sector, the competitive landscape will continue to evolve, driving innovation and fostering the adoption of environmentally friendly agrochemical products.

Report Objectives:

The report will help you answer some of the most critical questions in the Agrochemicals Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the Agrochemicals Market?

- What is the size of the Agrochemicals Market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 231.2 billion |

|

Forecasted Value (2030) |

USD 286.5 billion |

|

CAGR (2024 – 2030) |

3.1% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Agrochemicals Market By Type (Fertilizers, Pesticides), By Pesticides Type (Insecticides, Herbicides, Fungicides, Nematicides), By Fertilizer Type (Nitrogenous {Urea, Ammonium Nitrate, Ammonium Sulfate, Ammonia, Calcium Ammonium Nitrate}, Phosphatic {Diammonium Phosphate, Monoammonium Phosphate, Triple Superphosphate}, Potassic {Potassium Chloride, Potassium Sulphate), By Crop Type {Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables} |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3.Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Agrochemicals Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Fertilizers |

|

4.2. Pesticides |

|

5. Agrochemicals Market, by Pesticides Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Insecticides |

|

5.2. Herbicides |

|

5.3. Fungicides |

|

5.4. Nematicides |

|

5.5. Others |

|

6. Agrochemicals Market, by Fertilizer Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Nitrogenous |

|

6.1.1. Urea |

|

6.1.2. Ammonium Nitrate |

|

6.1.3. Ammonium Sulfate |

|

6.1.4. Ammonia |

|

6.1.5. Calcium Ammonium Nitrate |

|

6.1.6. Others |

|

6.2. Phosphatic |

|

6.2.1. Diammonium Phosphate |

|

6.2.2. Monoammonium Phosphate |

|

6.2.3. Triple Superphosphate |

|

6.2.4. Others |

|

6.3. Potassic |

|

6.3.1. Potassium Chloride |

|

6.3.2. Potassium Sulphate |

|

7. Agrochemicals Market, by Crop Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Cereals & Grains |

|

7.2. Oilseeds & Pulses |

|

7.3. Fruits & Vegetables |

|

7.4. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Agrochemicals Market, by Type |

|

8.2.7. North America Agrochemicals Market, by Pesticides Type |

|

8.2.8. North America Agrochemicals Market, by Fertilizer Type |

|

8.2.9. North America Agrochemicals Market, by Crop Type |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Agrochemicals Market, by Type |

|

8.2.10.1.2. US Agrochemicals Market, by Pesticides Type |

|

8.2.10.1.3. US Agrochemicals Market, by Fertilizer Type |

|

8.2.10.1.4. US Agrochemicals Market, by Crop Type |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. BASF |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Syngenta |

|

10.3. UPL |

|

10.4. Bayer Crop Science |

|

10.5. Sumitomo Chemical |

|

10.6. Corteva AG |

|

10.7. EuroChem |

|

10.8. K+S AG |

|

10.9. Nutrien |

|

10.10. Yara International |

|

10.11. ICL |

|

10.12. Verdesian Life Sciences |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Agrochemicals Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Agrochemicals Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the Agrochemicals ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Agrochemicals Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

.jpg)