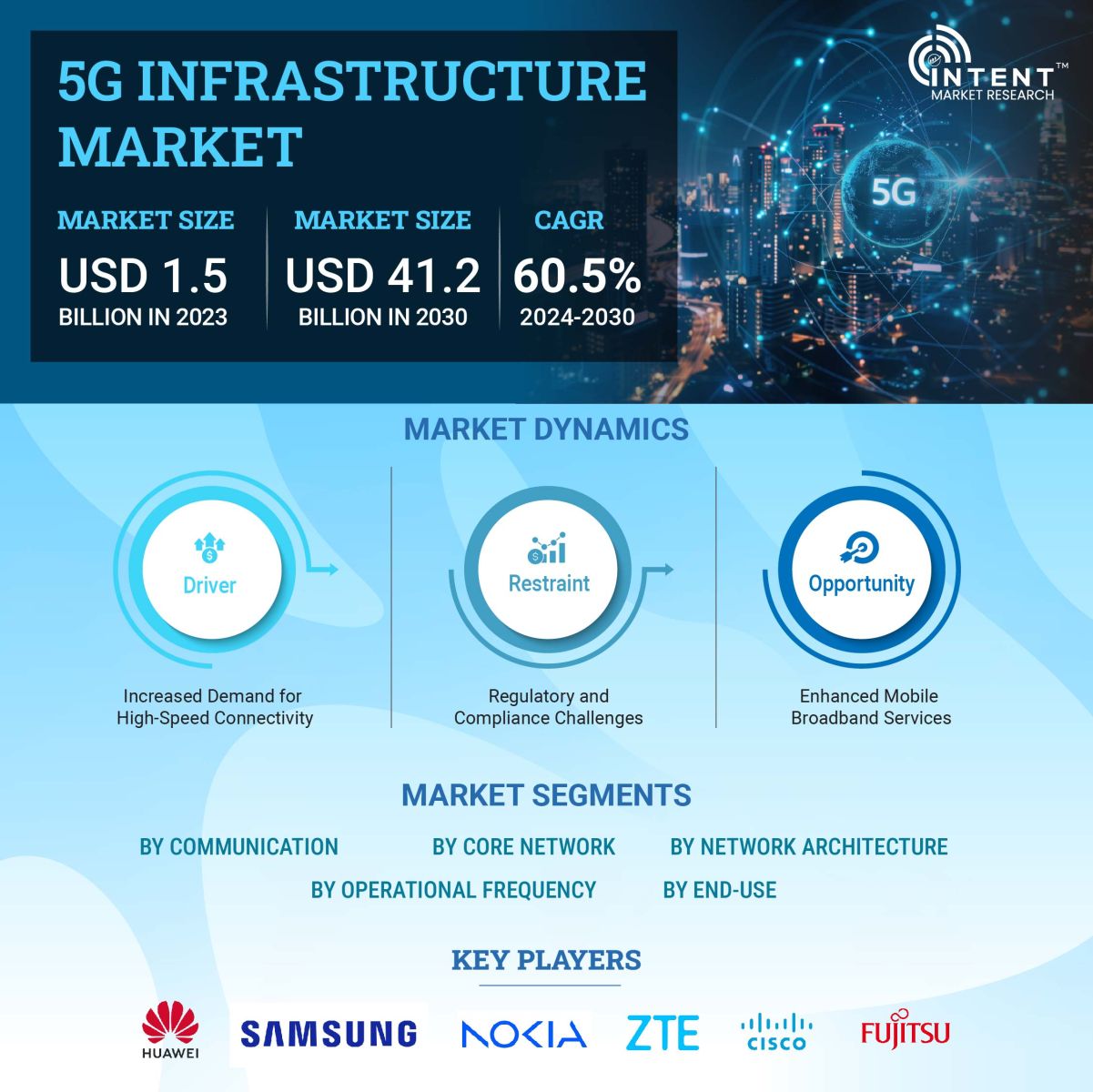

As per Intent Market Research, the 5G Infrastructure Market was valued at USD 1.5 billion in 2023 and will surpass USD 41.2 billion by 2030; growing at a CAGR of 60.5% during 2024 - 2030.

The 5G infrastructure market is poised for significant growth as global demand for high-speed connectivity and advanced communication technologies increases. With the advent of the fifth-generation wireless technology, 5G infrastructure promises to revolutionize various industries, enhancing operational efficiency and enabling new applications such as autonomous vehicles, smart cities, and the Internet of Things (IoT). The market is expected to reach a valuation of around $300 billion by 2030, driven by substantial investments in network deployment and upgrades, alongside growing consumer demand for high-speed internet.

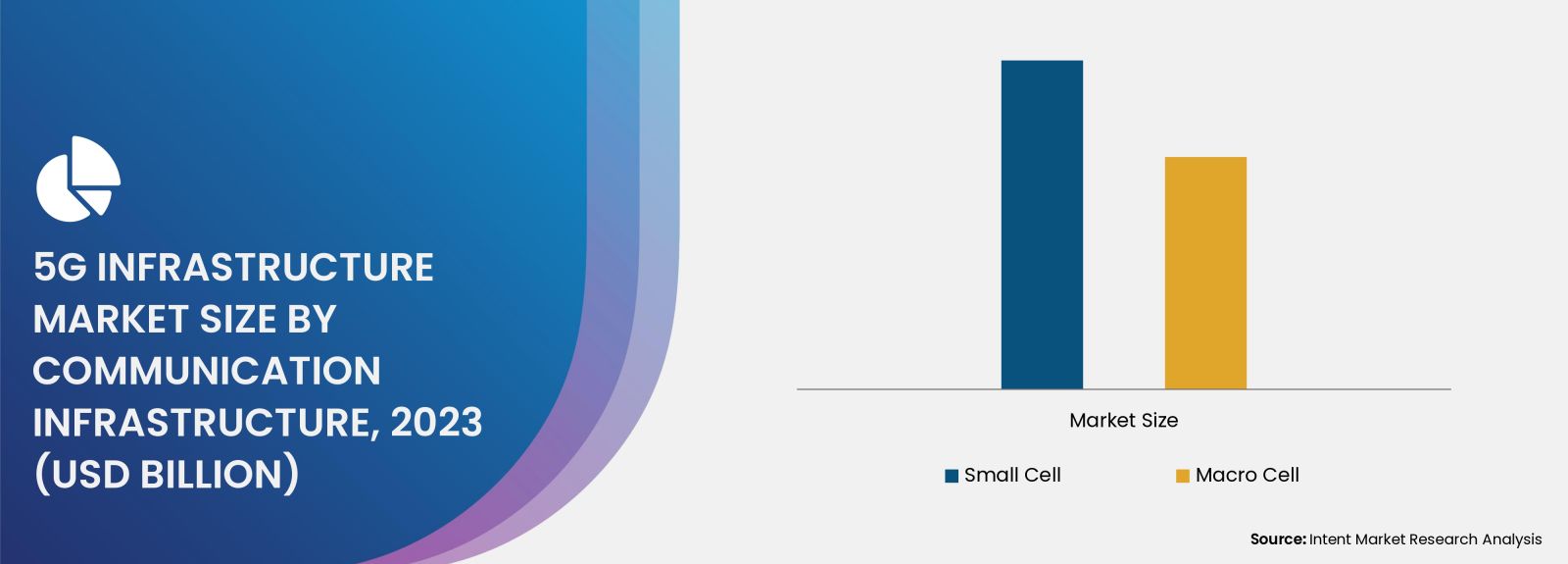

As 5G technology matures, different segments of the infrastructure market will emerge, characterized by varying growth dynamics. This market comprises several segments, including small cells, macro cells, distributed antenna systems (DAS), and core network technology. Each of these segments plays a crucial role in the development and deployment of 5G networks, contributing to their overall effectiveness and efficiency. This report delves into the largest or fastest-growing subsegments within each category, providing a comprehensive overview of the market landscape.

Small Cells Segment is Fastest Growing Owing to Increased Demand for Dense Network Coverage

Among the various subsegments of the small cells category, outdoor small cells are expected to experience the fastest growth in the coming years. Outdoor small cells enhance the capacity and coverage of mobile networks, particularly in densely populated urban areas where traditional macro cells may not suffice. Their ability to support high user density and improve the quality of service is driving rapid adoption, particularly in regions experiencing significant urbanization. As municipalities invest in smart city initiatives, the demand for outdoor small cells is expected to surge, further propelling market growth.

Additionally, outdoor small cells play a crucial role in enabling seamless connectivity for emerging technologies, such as augmented reality (AR) and virtual reality (VR), which require low latency and high bandwidth. This growing reliance on mobile data and bandwidth-intensive applications is catalyzing investments in small cell infrastructure. Consequently, telecommunications operators are focusing on expanding their small cell networks, which will likely result in a significant uptick in the deployment of outdoor small cells, positioning this subsegment as a key growth driver within the overall 5G infrastructure market.

Macro Cells Segment is Largest Owing to Extensive Network Coverage Requirements

In the macro cells segment, traditional macro cells remain the largest subsegment due to their extensive coverage capabilities and established infrastructure. These large antennas provide broad area coverage and are critical in ensuring the reliability of 5G services, particularly in rural and suburban areas where user density is lower. Macro cells are essential for operators looking to establish a robust 5G network, as they form the backbone of coverage, enabling widespread access to high-speed internet and improved communication services.

The deployment of macro cells is also facilitated by significant advancements in antenna technology, including the integration of Massive MIMO (Multiple Input Multiple Output) systems. These enhancements allow operators to increase network capacity and performance while optimizing spectrum utilization. As telecommunications companies strive to meet growing consumer demands, the macro cell segment is expected to continue dominating the market, providing essential connectivity solutions for both urban and rural populations.

Distributed Antenna Systems (DAS) Segment is Fastest Growing Owing to Indoor Connectivity Needs

Within the DAS segment, the in-building DAS subsegment is anticipated to grow at the fastest rate due to the rising demand for reliable indoor connectivity. As organizations recognize the importance of providing seamless mobile coverage within their facilities, investments in in-building DAS solutions have increased significantly. This trend is particularly prevalent in commercial buildings, airports, stadiums, and other high-traffic venues where consistent connectivity is critical for both operational efficiency and customer experience.

In-building DAS solutions are designed to distribute cellular signals throughout a structure, ensuring that users can maintain high-quality connections regardless of their location within the building. The increasing adoption of IoT devices and smart technologies in indoor environments further drives the demand for reliable connectivity solutions. As businesses seek to enhance their digital infrastructure, the in-building DAS segment is poised to play a vital role in shaping the future of 5G infrastructure, capitalizing on the growing emphasis on indoor network reliability.

Core Network Technology Segment is Largest Owing to Centralized Network Management

In the core network technology segment, virtualized core networks are emerging as the largest subsegment due to their flexibility and scalability. Virtualized core networks enable operators to efficiently manage network resources, optimize performance, and adapt to changing demands in real-time. This technology plays a pivotal role in supporting the diverse requirements of 5G applications, ranging from ultra-reliable low-latency communications to massive machine-type communications.

The shift towards cloud-native architectures and software-defined networking (SDN) is further accelerating the growth of virtualized core networks. These advancements allow telecommunications providers to streamline operations, reduce costs, and enhance service delivery. As operators increasingly adopt virtualized core solutions to support their 5G initiatives, this subsegment is expected to dominate the core network technology landscape, providing essential capabilities for effective network management and performance optimization.

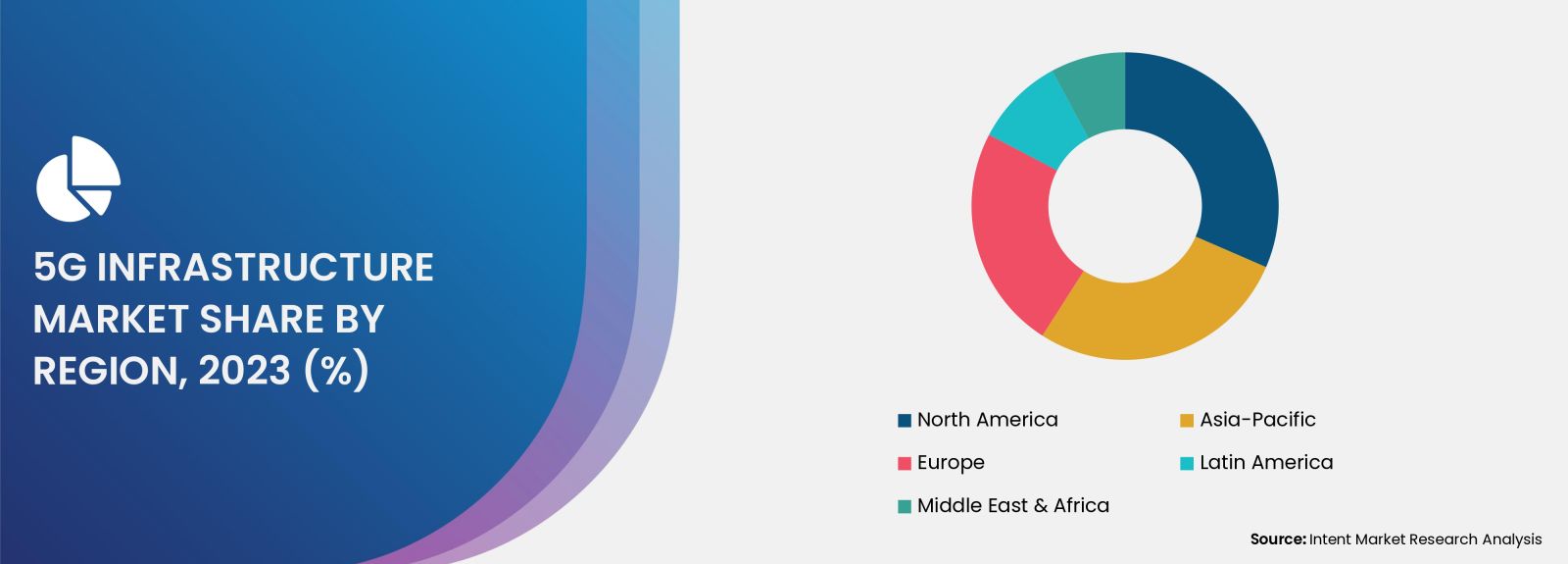

Regional Analysis: North America is Largest Region Owing to Early Adoption of 5G Technology

North America stands out as the largest region in the 5G infrastructure market, primarily driven by the early adoption of 5G technology and substantial investments from telecommunications operators. The presence of key market players, coupled with supportive government initiatives, has fostered a favorable environment for 5G deployment in this region. Companies are investing heavily in building robust 5G networks to meet the growing demand for high-speed internet and advanced communication services.

Moreover, North America is witnessing a surge in applications powered by 5G technology, including smart cities, autonomous vehicles, and industrial automation. The increasing deployment of 5G infrastructure across various sectors further cements the region's position as a leader in the global 5G landscape. As technology continues to advance and consumer demand grows, North America is expected to maintain its dominance in the 5G infrastructure market, shaping the future of connectivity and communication.

Competitive Landscape and Leading Companies

The competitive landscape of the 5G infrastructure market is characterized by the presence of several key players who are actively engaged in innovation and strategic partnerships to enhance their offerings. Leading companies such as Ericsson, Nokia, Huawei, and Qualcomm are at the forefront of the market, providing advanced technologies and solutions that support the deployment and management of 5G networks. These companies are investing heavily in research and development to drive innovation and improve network performance.

Additionally, collaborations between telecommunications operators and infrastructure providers are becoming increasingly common as companies seek to leverage each other's strengths to accelerate 5G deployment. Mergers and acquisitions within the industry are also contributing to market dynamics, allowing companies to expand their capabilities and reach. As the 5G infrastructure market continues to evolve, competition is expected to intensify, with companies focusing on enhancing service delivery, optimizing network performance, and driving customer engagement through innovative solutions.

Report Objectives:

The report will help you answer some of the most critical questions in the 5G Infrastructure Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the 5G Infrastructure Market?

- What is the size of the 5G Infrastructure Market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.5 billion |

|

Forecasted Value (2030) |

USD 41.2 billion |

|

CAGR (2024 – 2030) |

60.5% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

5G Infrastructure Market By Communication Infrastructure (Small Cell, Macro Cell), By Core Network (Software-Defined Networking, Network Function Virtualization), By Network Architecture (5G NR Non-Standalone, 5G Standalone), By Operational Frequency (Sub 6 GHz, Above 6 GHz), By End-Use (Residential, Commercial, Industrial, Government) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3.Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. 5G Infrastructure Market, by Communication Infrastructure (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Small Cell |

|

4.2. Macro Cell |

|

5. 5G Infrastructure Market, by Core Network (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Software-Defined Networking |

|

5.2. Network Function Virtualization |

|

6. 5G Infrastructure Market, by Network Architecture (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. 5G NR Non-Standalone |

|

6.2. 5G Standalone |

|

7. 5G Infrastructure Market, by Operational Frequency (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Sub 6 GHz |

|

7.2. Above 6 GHz |

|

8. 5G Infrastructure Market, by End-Use (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Residential |

|

8.2. Commercial |

|

8.3. Industrial |

|

8.4. Government |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America 5G Infrastructure Market, by Communication Infrastructure |

|

9.2.7. North America 5G Infrastructure Market, by Core Network |

|

9.2.8. North America 5G Infrastructure Market, by Network Architecture |

|

9.2.9. North America 5G Infrastructure Market, by Operational Frequency |

|

9.2.10. North America 5G Infrastructure Market, by End-Use |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US 5G Infrastructure Market, by Communication Infrastructure |

|

9.2.11.1.2. US 5G Infrastructure Market, by Core Network |

|

9.2.11.1.3. US 5G Infrastructure Market, by Network Architecture |

|

9.2.11.1.4. US 5G Infrastructure Market, by Operational Frequency |

|

9.2.11.1.5. US 5G Infrastructure Market, by End-Use |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Airspan |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. AT&T |

|

11.3. Cisco Systems |

|

11.4. Comba Telecom Systems |

|

11.5. Ericsson |

|

11.6. Fujitsu |

|

11.7. Hewlett Packard Enterprise |

|

11.8. Huawei |

|

11.9. Nokia |

|

11.10. Samsung |

|

11.11. ZTE Corporation |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the 5G Infrastructure Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the 5G Infrastructure Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the 5G Infrastructure ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the 5G Infrastructure Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.