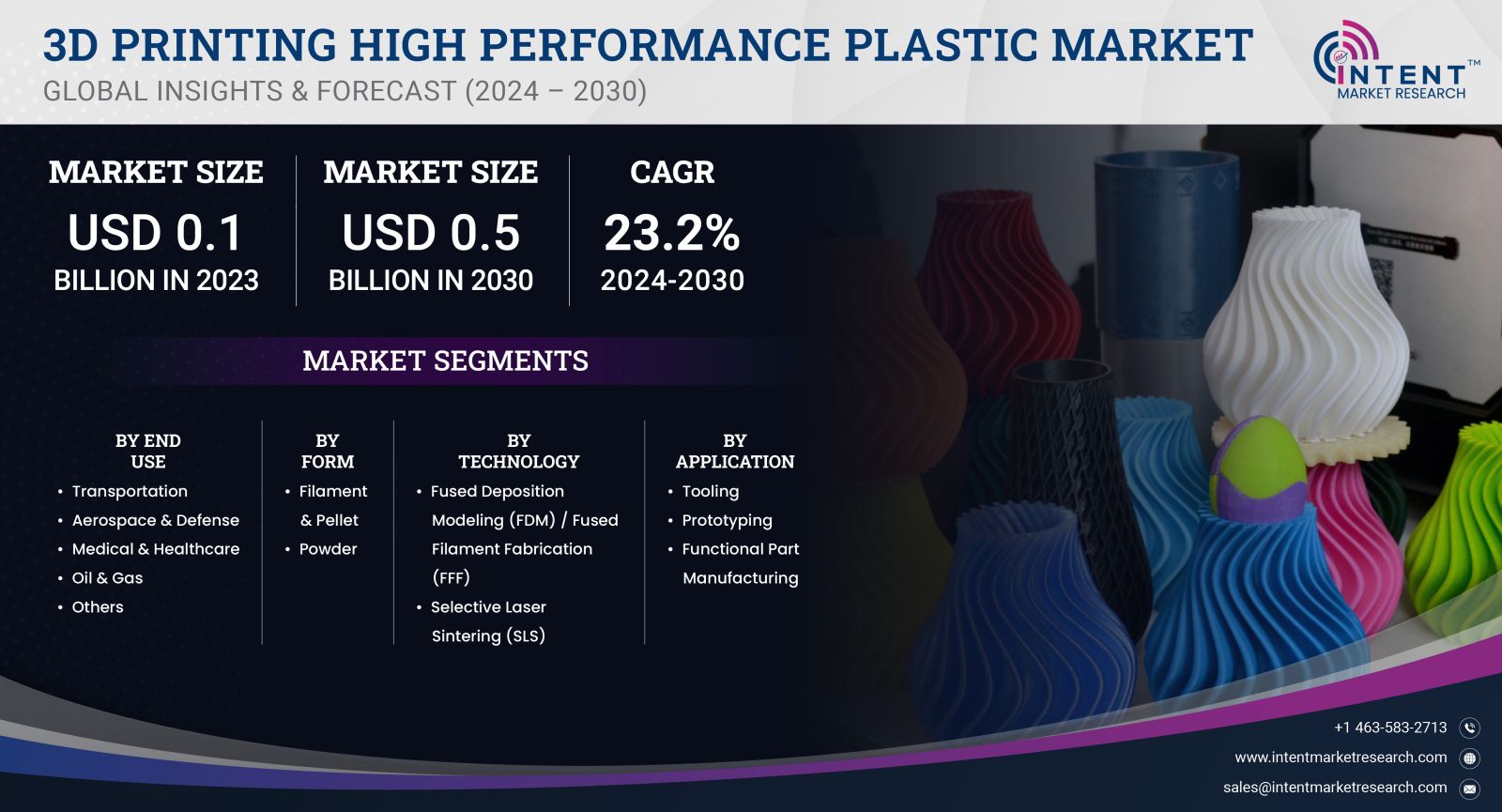

As per Intent Market Research, the 3D Printing High Performance Plastic Market was valued at USD 0.1 billion in 2023 and will surpass USD 0.5 billion by 2030; growing at a CAGR of 23.2% during 2024 - 2030.

Between 2024 and 2030, the market is expected to expand with a CAGR of approximately 22%, propelled by innovations in materials science, greater adoption of 3D printing technologies, and the continuous need for performance-driven solutions in industrial applications. The market is highly dynamic, with research focused on developing new materials that offer enhanced properties, lower costs, and better performance for a variety of end-use applications. As the market matures, the integration of these materials in industrial and consumer products is anticipated to increase, opening up new avenues for growth

Aerospace & Defense Segment is Largest Owing to Demand for Lightweight and Durable Parts

The Aerospace & Defense segment holds the largest share in the 3D Printing High Performance Plastic market, driven by the growing need for lightweight, durable, and high-precision components. In this sector, the demand for high-performance plastics, such as PEEK (Polyetheretherketone), ULTEM, and PEI, has surged due to their ability to withstand extreme environments while maintaining structural integrity. 3D printing enables the production of intricate, customized parts that are lighter and more cost-effective than traditionally manufactured components, which is crucial in industries where reducing weight directly impacts fuel efficiency, performance, and operational costs.

With the aerospace industry increasingly focusing on reducing the weight of aircraft to improve fuel efficiency and overall performance, high-performance plastics play a pivotal role in achieving these goals. Furthermore, the complexity of aerospace components, which often require specific geometries and properties, makes 3D printing an ideal manufacturing technique. As aerospace and defense industries continue to adopt additive manufacturing technologies, the use of high-performance plastics in these sectors will remain a dominant driver of market growth.

Automotive Segment is Fastest Growing Owing to Customization and Lightweighting Needs

The Automotive segment is the fastest growing in the 3D Printing High Performance Plastic market, driven by the demand for custom, lightweight, and performance-enhancing components. Automotive manufacturers are increasingly adopting 3D printing technologies to produce parts such as engine components, structural elements, and interior parts that are lighter, more durable, and optimized for performance. High-performance plastics like PEEK, polyamide, and ABS are gaining popularity in automotive applications due to their strength, flexibility, and ability to withstand harsh conditions such as high temperatures, chemical exposure, and mechanical stress.

The automotive industry is also focusing on producing customized components in smaller production runs to meet evolving consumer demands and regulatory requirements for fuel efficiency and emissions reductions. 3D printing technologies allow for rapid prototyping, rapid production of parts with complex geometries, and the ability to produce bespoke components that reduce the weight of vehicles without compromising on strength or safety. As automotive manufacturers continue to invest in additive manufacturing, the demand for high-performance plastics in this segment is expected to grow at an accelerated pace.

Materials Segment is Largest Owing to Advancements in Performance Plastics

The Materials segment is the largest in the 3D Printing High Performance Plastic market, as the development and adoption of high-performance plastics are critical to the expansion of the market. Key materials such as PEEK, PEI, ULTEM, and PPS (Polyphenylene sulfide) are at the forefront of this segment, offering exceptional mechanical, thermal, and chemical properties. These materials enable 3D printing to produce components that can endure extreme conditions, making them highly sought after for industries like aerospace, automotive, medical, and industrial manufacturing.

Innovations in material formulations are driving growth in this segment. For example, researchers are working on enhancing the printability of these high-performance plastics, improving their compatibility with 3D printers, and reducing their overall cost. This is making these materials more accessible for a wider range of industries and applications. As demand grows for lightweight, durable, and customizable components, the material segment will continue to drive the expansion of the 3D printing high-performance plastic market.

North America Region is Largest Owing to Technological Advancements and Industry Adoption

North America is the largest region for the 3D Printing High Performance Plastic market, driven by the presence of leading players in aerospace, automotive, and healthcare industries, which are major consumers of high-performance plastics. The United States, in particular, is a hub for technological innovation, with substantial investments in research and development for 3D printing technologies. The region's robust infrastructure, coupled with favorable government policies supporting the development and adoption of advanced manufacturing technologies, is further contributing to market growth.

In aerospace and defense, major companies like Boeing and Lockheed Martin are leading the way in adopting 3D printing technologies to produce high-performance components. Similarly, in automotive, companies such as Ford, General Motors, and Tesla are leveraging 3D printing for rapid prototyping and manufacturing of performance parts. North America's advanced manufacturing ecosystem, coupled with a growing emphasis on sustainability, is expected to keep the region as the leader in the 3D printing high-performance plastic market throughout the forecast period.

Asia Pacific Region is Fastest Growing Owing to Increasing Industrialization and Technological Advancements

The Asia Pacific (APAC) region is the fastest growing market for 3D Printing High Performance Plastics, driven by rapid industrialization, technological advancements, and growing adoption of additive manufacturing technologies in countries like China, Japan, and India. The automotive and aerospace sectors in these countries are increasingly embracing 3D printing to streamline manufacturing processes, reduce costs, and create high-performance components. Moreover, the region's focus on developing smart manufacturing solutions and optimizing supply chains is further accelerating the adoption of 3D printing technologies.

China, in particular, is making significant strides in adopting 3D printing for industrial applications. The country's initiatives to enhance its manufacturing capabilities and its growing automotive and aerospace industries are driving the demand for high-performance plastics in 3D printing. As the region continues to develop its technological infrastructure, APAC is expected to see rapid growth in the adoption of high-performance plastics in additive manufacturing, making it the fastest growing market for the forecast period.

Leading Companies and Competitive Landscape

The 3D Printing High Performance Plastic market is highly competitive, with several key players driving innovation and technological advancements in materials, printers, and solutions. Prominent companies in the market include Stratasys Ltd., 3D Systems Corporation, EOS GmbH, HP Inc., and Materialise NV. These companies are at the forefront of the development of 3D printing solutions and high-performance plastics. They focus on expanding their product portfolios, investing in R&D to improve the mechanical properties of 3D printing materials, and increasing production efficiency to reduce costs.

The competitive landscape is also characterized by collaborations and partnerships between material suppliers, 3D printing technology developers, and end-users. Companies are working on improving material formulations to make them more suitable for 3D printing and expanding their capabilities in industrial-scale production. As the market grows, competition will intensify with a strong focus on enhancing performance, reducing production costs, and improving material availability. These factors are expected to drive continued innovation in the 3D printing high-performance plastic market.

Report Objectives:

The report will help you answer some of the most critical questions in the 3D Printing High Performance Plastic Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the 3D printing high performance plastic market?

- What is the size of the 3D printing high performance plastic market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023-e) |

USD 0.1 billion |

|

Forecasted Value (2030) |

USD 0.5 billion |

|

CAGR (2024-2030) |

23.2% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024-2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

3D Printing High Performance Plastic By Form (Filament & Pellet, Powder), By Technology (FDM/FFF, SLS), By Application (Prototyping, Tooling, Functional Part Manufacturing), By End Use (Medical & Healthcare, Aerospace & Defense, Transportation, Oil & Gas), |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Spain, Italy & Rest of Europe), Asia Pacific (China, Japan, South Korea, India, and rest of Asia Pacific), Latin America (Brazil, Argentina, & Rest of Latin America), Middle East & Africa (Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1.Introduction |

|

1.1.Market Definition |

|

1.2.Scope of the Study |

|

1.3.Research Assumptions |

|

1.4.Study Limitations |

|

2.Research Methodology |

|

2.1.Research Approach |

|

2.1.1.Top-Down Method |

|

2.1.2.Bottom-Up Method |

|

2.1.3.Factor Impact Analysis |

|

2.2.Insights & Data Collection Process |

|

2.2.1.Secondary Research |

|

2.2.2.Primary Research |

|

2.3.Data Mining Process |

|

2.3.1.Data Analysis |

|

2.3.2.Data Validation and Revalidation |

|

2.3.3.Data Triangulation |

|

3.Executive Summary |

|

3.1.Major Markets & Segments |

|

3.2.Highest Growing Regions and Respective Countries |

|

3.3.Impact of Growth Drivers & Inhibitors |

|

3.4.Regulatory Overview by Country |

|

4.3D Printing High Performance Plastic Market, by End Use (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

4.1.Transportation |

|

4.2.Aerospace & Defense |

|

4.3.Medical & Healthcare |

|

4.4.Oil & Gas |

|

4.5.Others |

|

5.3D Printing High Performance Plastic Market, by Form (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

5.1.Filament & Pellet |

|

5.2.Powder |

|

6.3D Printing High Performance Plastic Market, by Technology (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.Fused Deposition Modeling (FDM) / Fused Filament Fabrication (FFF) |

|

6.2.Selective Laser Sintering (SLS) |

|

7.3D Printing High Performance Plastic Market, by Application (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

7.1.Tooling |

|

7.2.Prototyping |

|

7.3.Functional Part Manufacturing |

|

8.Regional Analysis (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

8.1.Regional Overview |

|

8.2.North America |

|

8.2.1.Regional Trends & Growth Drivers |

|

8.2.2.Barriers & Challenges |

|

8.2.3.Opportunities |

|

8.2.4.Factor Impact Analysis |

|

8.2.5.Technology Trends |

|

8.2.6.North America 3D Printing High Performance Plastic Market, by Form |

|

8.2.7.North America 3D Printing High Performance Plastic Market, by End Use |

|

8.2.8.North America 3D Printing High Performance Plastic Market, by Technology |

|

8.2.9.North America 3D Printing High Performance Plastic Market, by Application |

|

*Similar segmentation will be provided at each regional level |

|

8.3.By Country |

|

8.3.1.US |

|

8.3.1.1.US 3D Printing High Performance Plastic Market, by Form |

|

8.3.1.2.US 3D Printing High Performance Plastic Market, by End Use |

|

8.3.1.3.US 3D Printing High Performance Plastic Market, by Technology |

|

8.3.1.4.US 3D Printing High Performance Plastic Market, by Application |

|

8.3.2.Canada |

|

8.3.3.Mexico |

|

*Similar segmentation will be provided at each country level |

|

8.4.Europe |

|

8.5.APAC |

|

8.6.Latin America |

|

8.7.Middle East & Africa |

|

9.Competitive Landscape |

|

9.1.Overview of the Key Players |

|

9.2.Competitive Ecosystem |

|

9.2.1.Platform Manufacturers |

|

9.2.2.Subsystem Manufacturers |

|

9.2.3.Service Providers |

|

9.2.4.Software Providers |

|

9.3.Company Share Analysis |

|

9.4.Company Benchmarking Matrix |

|

9.4.1.Strategic Overview |

|

9.4.2.Product Innovations |

|

9.5.Start-up Ecosystem |

|

9.6.Strategic Competitive Insights/ Customer Imperatives |

|

9.7.ESG Matrix/ Sustainability Matrix |

|

9.9.Manufacturing Network |

|

9.9.1.Locations |

|

9.9.2.Supply Chain and Logistics |

|

9.9.3.Product Flexibility/Customization |

|

9.9.4.Digital Transformation and Connectivity |

|

9.9.5.Environmental and Regulatory Compliance |

|

9.10.Technology Readiness Level Matrix |

|

9.11.Technology Maturity Curve |

|

9.12.Buying Criteria |

|

10.Company Profiles |

|

10.1.Arkema |

|

10.1.1.Company Overview |

|

10.1.2.Company Financials |

|

10.1.3.Product/Service Portfolio |

|

10.1.4.Recent Developments |

|

10.1.5.IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2.Stratasys |

|

10.3.Evonik Industries |

|

10.4.3D Systems, Inc. |

|

10.5.Markforged |

|

10.6.Oxford Performance Materials |

|

10.7.SABIC |

|

10.8.Ensinger |

|

10.9.BASF |

|

10.10.Solvay |

|

11.Appendix |

A comprehensive market research approach was employed to gather and analyze data on the 3D Printing High Performance Plastic Market. In the process, the analysis was also done to estimate the parent market and relevant adjacencies to major the impact of them on the 3D printing high performance plastic market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the 3D printing high performance plastic ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Estimation

A combination of top-down and bottom-up approaches was utilized to estimate the overall size of the 3D printing high performance plastic market. These methods were also employed to estimate the size of various sub segments within the market. The market size estimation methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size estimates, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size estimates.

NA