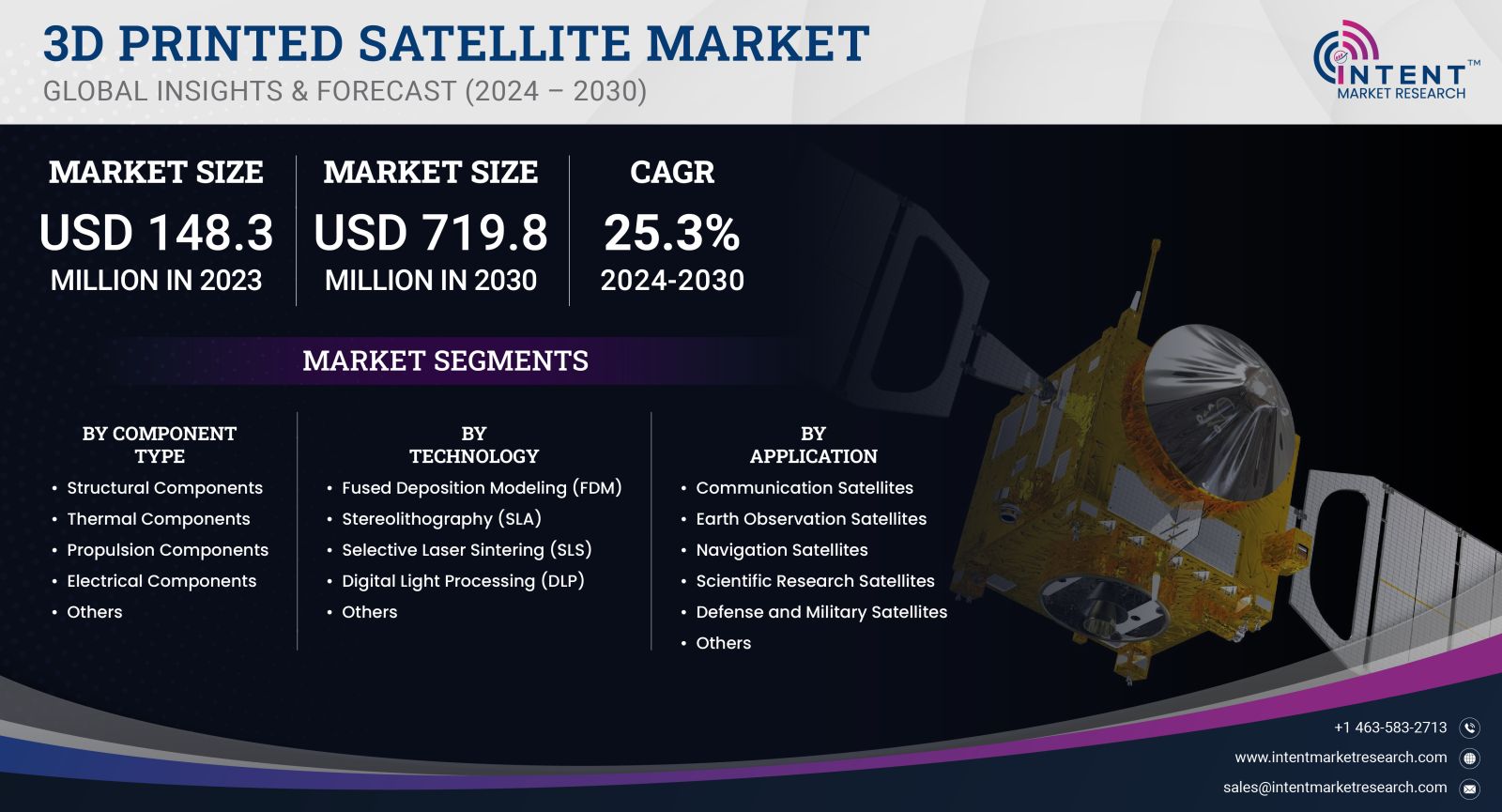

As per Intent Market Research, the 3D Printed Satellite Market was valued at USD 148.3 million in 2023 and will surpass USD 719.8 million by 2030; growing at a CAGR of 25.3% during 2024 - 2030.

The 3D printed satellite market represents a groundbreaking shift in satellite manufacturing and design, driven by the need for more cost-effective, lightweight, and quickly deployable solutions. With advancements in additive manufacturing (AM) technologies, satellite manufacturers are increasingly adopting 3D printing techniques to produce components with intricate designs that are difficult to achieve with traditional methods. This market has seen a remarkable growth trajectory due to the rise in demand for small satellites (smallsats) and CubeSats, which are vital for telecommunications, earth observation, and defense applications.

Application Segment: Telecommunications Segment is Largest Owing to Expanding Connectivity Needs

The telecommunications sector has emerged as the largest subsegment in the 3D printed satellite market, primarily due to the growing global demand for high-speed internet and communication services. As nations and corporations endeavor to bridge the digital divide, the deployment of constellations of small satellites has become a priority. 3D printing allows for rapid prototyping and customization of satellite components, reducing manufacturing lead times and lowering costs, making it ideal for the telecommunications sector.

Telecommunications satellites, especially in Low Earth Orbit (LEO), benefit significantly from 3D printing as it facilitates the production of lighter and more efficient antenna arrays and transponder housings. This weight reduction allows for higher payload capacities and extended operational lifespans, directly impacting service quality. As demand for internet services continues to grow, particularly in rural and underserved regions, the telecommunications segment will remain the largest driver of the 3D printed satellite market throughout the forecast period.

Component Segment: Structural Components Segment is Fastest Growing Owing to Innovations in Lightweight Materials

Among the different components used in satellite manufacturing, the structural components segment is experiencing the fastest growth. Structural parts of satellites, such as frames, brackets, and enclosures, have been traditionally manufactured using heavy, rigid materials. However, with the adoption of 3D printing technologies, these components are now being produced using advanced, lightweight materials such as titanium alloys and composite polymers.

The ability to 3D print complex geometries with internal support structures reduces the overall weight of the satellite while maintaining its durability and strength, which is crucial for surviving the harsh environment of space. The reduction in weight also leads to lower launch costs and the ability to incorporate more sophisticated payloads. As satellite manufacturers continue to experiment with new materials and designs, the structural components segment is expected to grow rapidly, offering further efficiencies in satellite production.

End-User Segment: Commercial Segment is Largest Owing to Increased Private Sector Investments

The commercial segment is currently the largest end-user of 3D printed satellites, driven by private sector investments in space exploration, telecommunications, and data services. Companies like SpaceX, Amazon, and OneWeb are leading the charge in developing satellite constellations for internet services, positioning the commercial sector as a key driver of growth in this market.

Commercial enterprises are embracing 3D printed satellites for their flexibility, reduced production timelines, and lower costs. This trend is amplified by the increasing demand for earth observation data, where satellites are utilized for monitoring climate change, agricultural trends, and urban development. With the private sector's increasing focus on innovative satellite services and the potential for lucrative returns on investment, the commercial segment is expected to remain the largest user of 3D printed satellites in the foreseeable future.

Orbit Segment: Low Earth Orbit (LEO) Segment is Fastest Growing Owing to Demand for Smallsats

The Low Earth Orbit (LEO) segment is witnessing the fastest growth in the 3D printed satellite market due to the rising demand for small satellites (smallsats) and CubeSats. These satellites are often deployed in LEO for a variety of applications, including earth observation, scientific research, and telecommunications. The proximity of LEO to Earth allows for reduced communication latency and quicker data transmission, which is crucial for real-time applications such as satellite internet.

The trend towards deploying satellite constellations in LEO has accelerated the adoption of 3D printing for satellite manufacturing, as it allows for the mass production of components at a fraction of the cost and time required by traditional manufacturing methods. As the number of LEO satellites continues to rise, this segment is expected to experience exponential growth, driven by the need for rapid, scalable satellite solutions.

Region: North America is Largest Owing to Strong Space Sector Infrastructure

North America, particularly the United States, is the largest region in the 3D printed satellite market, owing to its well-established space industry and continuous investments in space exploration and defense. Major players like NASA, SpaceX, and Boeing are at the forefront of integrating 3D printing technologies into satellite manufacturing processes, driving the market's expansion in the region.

The presence of advanced research facilities, coupled with government support for space initiatives, has created a favorable environment for the development of 3D printed satellite components. Additionally, the U.S. military’s interest in space-based assets for national defense has further fueled growth. North America’s dominance is expected to continue, as it remains a hub for satellite technology innovation and deployment, catering to both commercial and defense applications.

Competitive Landscape and Leading Companies

The competitive landscape of the 3D printed satellite market is characterized by both established aerospace companies and innovative startups, all aiming to capitalize on the benefits of additive manufacturing. Leading companies in this space include Lockheed Martin, Boeing, Airbus, and SpaceX, who are integrating 3D printing into their satellite production lines to improve efficiency and reduce costs. Additionally, newer entrants like Relativity Space are pioneering fully 3D-printed satellites and rockets, positioning themselves as key disruptors.

The competition is intense, with companies focusing on rapid innovation, cost reduction, and strategic partnerships to enhance their market position. Intellectual property related to 3D printing techniques, materials, and design optimizations is becoming a critical aspect of the competitive dynamics, as firms seek to protect their technological advancements in this emerging field. As the market evolves, companies that can scale production and deliver high-quality, cost-effective satellite components are expected to lead in the coming years.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 148.3 million |

|

Forecasted Value (2030) |

USD 719.8 million |

|

CAGR (2024 – 2030) |

25.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

3D Printed Satellite Market By Component Type (Structural Components, Thermal Components, Propulsion Components, Electrical Components), By Technology (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), Digital Light Processing (DLP)), and By Application (Communication Satellites, Earth Observation Satellites, Navigation Satellites, Scientific Research Satellites, Defense and Military Satellites) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. 3D Printed Satellite Market, by Component Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Structural Components |

|

4.2. Thermal Components |

|

4.3. Propulsion Components |

|

4.4. Electrical Components |

|

4.5. Others |

|

5. 3D Printed Satellite Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Fused Deposition Modeling (FDM) |

|

5.2. Stereolithography (SLA) |

|

5.3. Selective Laser Sintering (SLS) |

|

5.4. Digital Light Processing (DLP) |

|

5.5. Others |

|

6. 3D Printed Satellite Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Communication Satellites |

|

6.2. Earth Observation Satellites |

|

6.3. Navigation Satellites |

|

6.4. Scientific Research Satellites |

|

6.5. Defense and Military Satellites |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America 3D Printed Satellite Market, by Component Type |

|

7.2.7. North America 3D Printed Satellite Market, by Technology |

|

7.2.8. North America 3D Printed Satellite Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US 3D Printed Satellite Market, by Component Type |

|

7.2.9.1.2. US 3D Printed Satellite Market, by Technology |

|

7.2.9.1.3. US 3D Printed Satellite Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. 3D Systems Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Airbus |

|

9.3. Boeing |

|

9.4. Lockheed Martin |

|

9.5. Materialise NV |

|

9.6. Northrop Grumman |

|

9.7. Relativity Space |

|

9.8. Rocket Lab |

|

9.9. Sierra Nevada Corporation |

|

9.10. Stratolaunch |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the 3D Printed Satellite Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the 3D Printed Satellite Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the 3D Printed Satellite ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the 3D Printed Satellite Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA