As per Intent Market Research, the 3D Camera Market was valued at USD 3.6 billion in 2023 and will surpass USD 13.0 billion by 2030; growing at a CAGR of 20.3% during 2024 - 2030.

The 3D camera market has witnessed significant growth and innovation over recent years, driven by advancements in technology and increasing applications across various sectors. The market encompasses a range of products designed to capture three-dimensional images and videos, allowing for enhanced visual experiences in fields such as entertainment, gaming, healthcare, and industrial applications. The demand for high-quality visual content, coupled with the rise of virtual reality (VR) and augmented reality (AR), has propelled the adoption of 3D cameras, making them integral tools for creators, professionals, and consumers alike.This growth trajectory reflects the increasing integration of 3D imaging technologies in various industries, alongside rising consumer expectations for immersive experiences.

Consumer Electronics Segment is Largest Owing to Widespread Adoption

The consumer electronics segment remains the largest in the 3D camera market, primarily driven by the growing demand for smartphones and personal devices equipped with 3D imaging capabilities. Manufacturers are increasingly integrating advanced camera technologies into smartphones, tablets, and other consumer gadgets to enhance user experiences. The ability to capture and share 3D images and videos has become a desirable feature, leading to a competitive advantage in the crowded consumer electronics market.

Additionally, the rise of social media and content creation platforms has amplified the need for high-quality visual content. Consumers are more inclined to engage with immersive and visually appealing content, further propelling the demand for 3D cameras in this segment. As brands continue to innovate and differentiate their products, the consumer electronics segment is likely to maintain its dominant position in the 3D camera market throughout the forecast period.

Healthcare Segment is Fastest Growing Owing to Technological Advancements

The healthcare segment of the 3D camera market is emerging as the fastest-growing, fueled by advancements in medical imaging technologies. The adoption of 3D imaging in healthcare is revolutionizing diagnostics, treatment planning, and surgical procedures. 3D cameras provide detailed and accurate representations of anatomical structures, facilitating better visualization for healthcare professionals. This technology is particularly beneficial in fields such as orthopedics, dentistry, and cosmetic surgery, where precision is crucial.

Furthermore, the increasing demand for minimally invasive surgical procedures has led to a rise in the use of 3D cameras for intraoperative imaging. As hospitals and clinics invest in advanced imaging technologies to improve patient outcomes and streamline operations, the healthcare segment is expected to see substantial growth. This trend is bolstered by continuous research and development efforts aimed at enhancing the capabilities of 3D imaging systems, thus positioning the healthcare segment for long-term success in the 3D camera market.

Industrial Segment is Largest Owing to Precision in Manufacturing

The industrial segment is characterized by the largest share of the 3D camera market, primarily due to the increasing demand for precision in manufacturing and quality control processes. Industries such as automotive, aerospace, and electronics utilize 3D cameras for applications such as reverse engineering, product design, and inspection. The ability to capture high-resolution 3D images facilitates accurate measurements and enhances product development, making 3D cameras an essential tool in the industrial sector.

Moreover, the integration of 3D imaging technologies with automation and artificial intelligence (AI) is further driving growth in this segment. Manufacturers are increasingly leveraging 3D cameras for automated quality inspection, reducing human error and ensuring compliance with stringent quality standards. As industries continue to embrace digital transformation and seek ways to optimize production processes, the industrial segment of the 3D camera market is poised for sustained growth.

Entertainment Segment is Fastest Growing Owing to Rising Demand for Immersive Experiences

The entertainment segment is witnessing rapid growth within the 3D camera market, fueled by the rising demand for immersive experiences in gaming, film, and virtual reality applications. As technology evolves, the entertainment industry is increasingly adopting 3D cameras to create lifelike visuals that captivate audiences. This trend is particularly evident in the gaming sector, where the integration of 3D imaging enhances gameplay and player engagement.

Additionally, the resurgence of 3D films and live events, coupled with advancements in 3D broadcasting technologies, is contributing to the segment's growth. Content creators are leveraging 3D cameras to push the boundaries of storytelling and visual effects, creating unique and engaging experiences for viewers. As consumer preferences shift towards more immersive entertainment options, the entertainment segment is set to thrive, making it a key area of focus for industry stakeholders in the coming years.

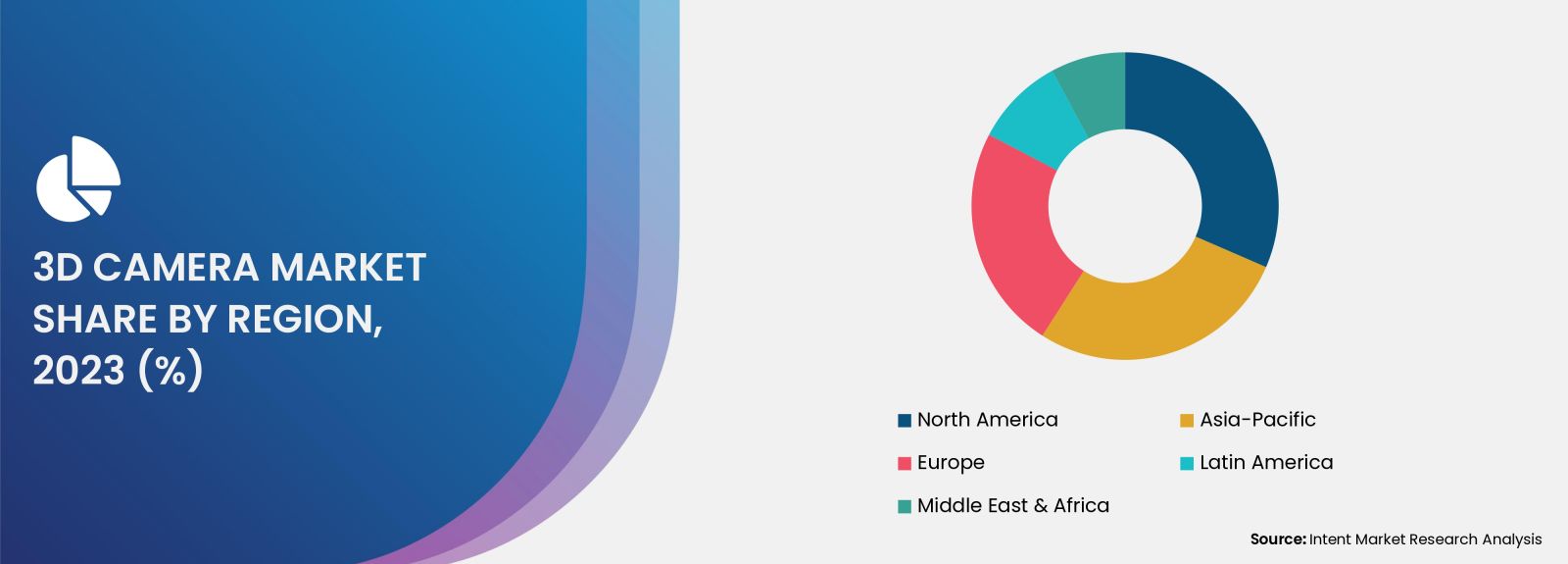

Fastest Growing Region: Asia-Pacific Region

The Asia-Pacific region is emerging as the fastest-growing market for 3D cameras, driven by rapid technological advancements and increasing investments in digital infrastructure. Countries such as China, Japan, and India are witnessing significant growth in the adoption of 3D imaging technologies across various sectors, including consumer electronics, healthcare, and entertainment. The expanding middle-class population in these countries is also contributing to the rising demand for advanced consumer electronics, thereby boosting the 3D camera market.

Moreover, the Asia-Pacific region is home to several leading manufacturers and technology companies that are actively investing in research and development to enhance their product offerings. The proliferation of start-ups focused on 3D imaging and VR technologies further accelerates market growth. As the region continues to embrace innovation and digital transformation, it is expected to maintain its position as a key player in the global 3D camera market.

Competitive Landscape

The competitive landscape of the 3D camera market is characterized by the presence of several key players and a dynamic environment marked by rapid technological advancements. Leading companies such as Canon Inc., Nikon Corporation, Sony Corporation, and GoPro, Inc. dominate the market by offering a diverse range of 3D camera products tailored to various applications. These companies are actively engaged in strategic partnerships, mergers, and acquisitions to enhance their market presence and expand their product portfolios.

Furthermore, the market is witnessing the emergence of niche players and start-ups specializing in innovative 3D imaging solutions. These companies are focusing on developing cutting-edge technologies, such as AI-powered imaging systems and compact 3D cameras, to cater to the evolving needs of consumers and industries. As competition intensifies, players in the 3D camera market are likely to invest heavily in research and development to maintain their competitive edge and capitalize on emerging trends, ensuring a vibrant and rapidly evolving market landscape through the forecast period and beyond.

Report Objectives:

The report will help you answer some of the most critical questions in the 3D Camera Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the 3D Camera Market?

- What is the size of the 3D Camera Market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.6 billion |

|

Forecasted Value (2030) |

USD 13.0 billion |

|

CAGR (2024 – 2030) |

20.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

3D Camera Market By Image Detection Technique (Structured Light, Stereoscopic Vision, Time of Flight), By Type (Target Camera, Target-Free Camera), and By End-User Industry (Aerospace & Defense, Construction, Automotive, Consumer Electronics, Industrial) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3.Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

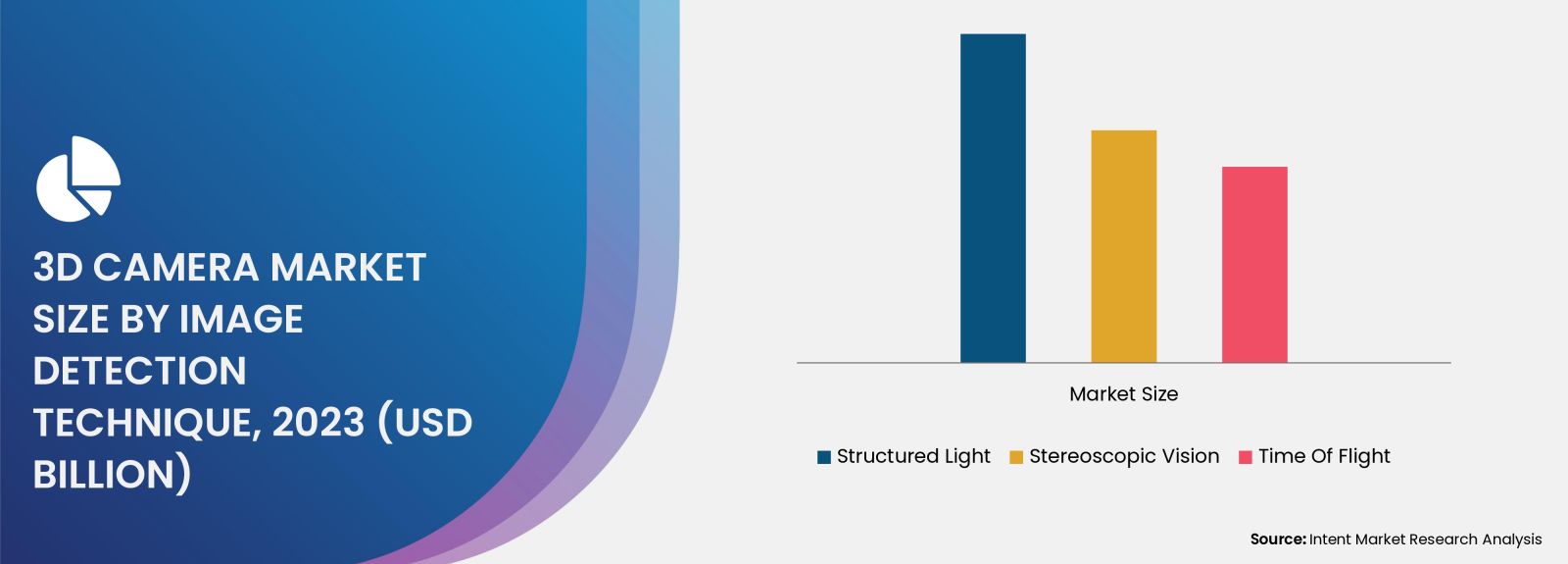

4. 3D Camera Market, by Image Detection Technique (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Structured Light |

|

4.2. Stereoscopic Vision |

|

4.3. Time of Flight |

|

5. 3D Camera Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Target Camera |

|

5.2. Target-Free Camera |

|

6. 3D Camera Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Aerospace & Defense |

|

6.2. Construction |

|

6.3. Automotive |

|

6.4. Consumer Electronics |

|

6.5. Industrial |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America 3D Camera Market, by Image Detection Technique |

|

7.2.7. North America 3D Camera Market, by Type |

|

7.2.8. North America 3D Camera Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US 3D Camera Market, by Image Detection Technique |

|

7.2.9.1.2. US 3D Camera Market, by Type |

|

7.2.9.1.3. US 3D Camera Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Orbbec Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. FARO |

|

9.3. Matterport, Inc. |

|

9.4. Ricoh Co., Ltd. |

|

9.5. Leica Geosystems AG |

|

9.6. Panasonic Life Solutions India Pvt. Ltd. |

|

9.7. ARASHI VISION INC. |

|

9.8. NavVis |

|

9.9. Intel |

|

9.10. Giraffe360 |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the 3D Camera Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the 3D Camera Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the 3D Camera ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the 3D Camera Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA