sales@intentmarketresearch.com

+1 463-583-2713

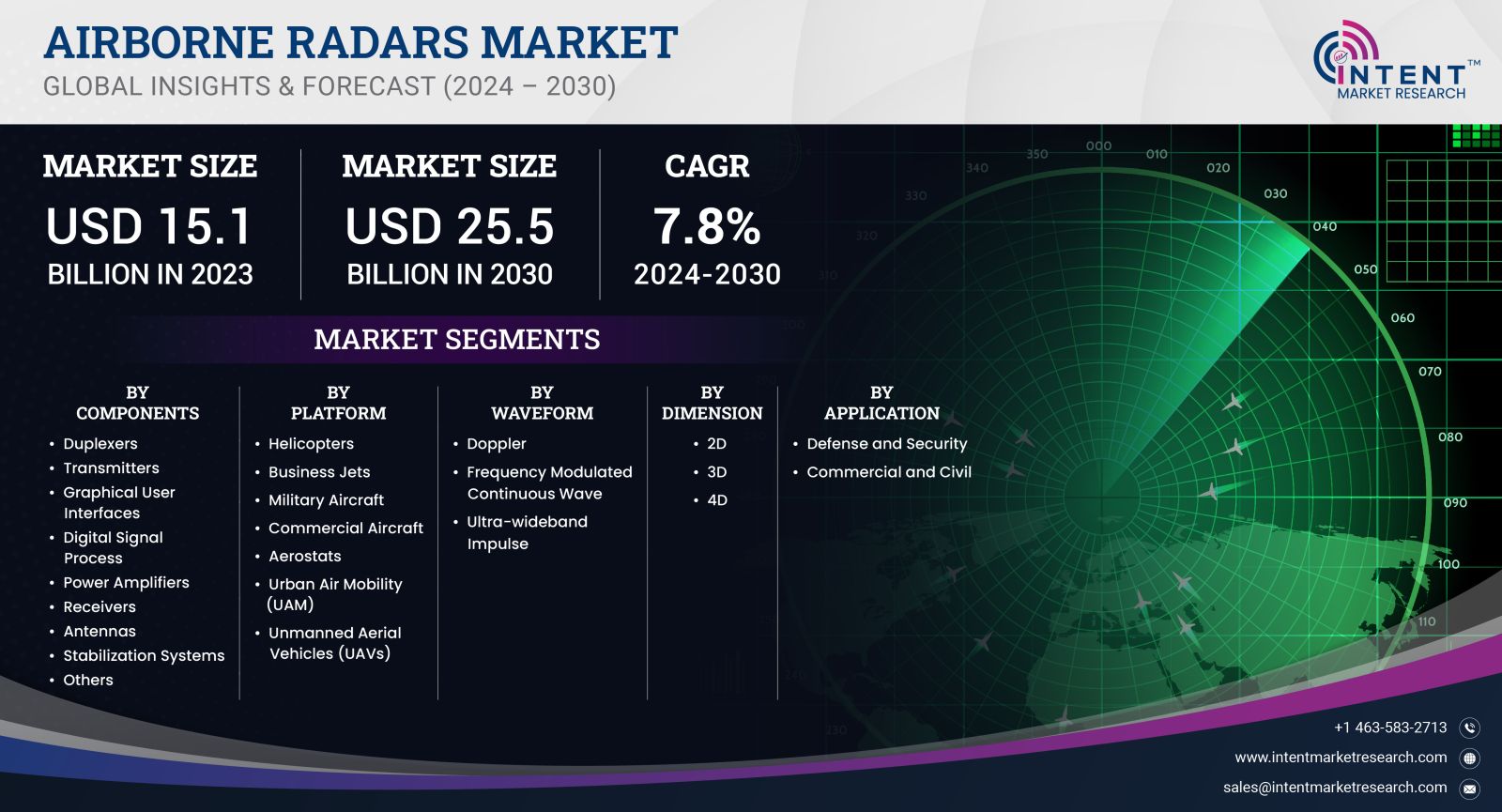

Airborne Radars Market By Component (Antenna, Transmitter, Duplexer, Receiver, Power Amplifier, Digital Signal Processor), By Platform (Commercial Aircraft, Military Aircraft, Business Jets), By Application (Defense & Security, Commercial & Civil), By Waveform (Frequency Modulated Continuous Wave, Doppler, Ultra-wideband Impulse), By Dimension (2D, 3D, 4D), and by Region; Global Insights & Forecast (2024 - 2030)

As per Intent Market Research, the Airborne Radars Market was valued at USD 15.1 billion in 2023-e and will surpass USD 25.5 billion by 2030; growing at a CAGR of 7.8% during 2024 - 2030.

The airborne radars market is witnessing significant growth, driven by advancements in radar technology and the increasing demand for sophisticated surveillance and reconnaissance systems. Airborne radars are critical components in various military and civilian applications, including air traffic control, maritime surveillance, and defense operations.

Military Segment is Largest Owing to Defense Modernization

The military segment represents the largest portion of the airborne radars market, primarily driven by ongoing defense modernization initiatives across the globe. Nations are investing heavily in upgrading their military assets to address evolving security threats and to maintain a strategic advantage over potential adversaries. Advanced airborne radars, equipped with high-resolution imaging capabilities and target tracking features, are essential for various military operations, including surveillance, reconnaissance, and target acquisition. The continuous enhancement of aerial combat systems, such as unmanned aerial vehicles (UAVs) and fighter jets, further contributes to the demand for military airborne radars.

In addition, the increasing geopolitical tensions and the need for border security are propelling the procurement of advanced radar systems by defense forces worldwide. Countries are focusing on developing indigenous radar technologies to ensure operational independence and to enhance their capabilities. This trend is particularly noticeable in regions such as North America and Asia-Pacific, where defense budgets are rising, and governments are prioritizing investments in advanced military technologies, thereby solidifying the military segment's position as the largest in the airborne radars market.

Commercial Segment is Fastest Growing Owing to Expanding Aviation Sector

The commercial segment of the airborne radars market is witnessing rapid growth, primarily fueled by the expanding aviation sector and increasing air traffic worldwide. With the rise in passenger and cargo flights, the need for efficient air traffic management and safety measures has become paramount. Airborne radars play a crucial role in air traffic control systems, facilitating safe navigation and preventing mid-air collisions. As commercial airlines invest in modernizing their fleet and improving operational efficiencies, the demand for advanced radar systems is expected to surge.

Moreover, the integration of airborne radars in various commercial applications, such as weather monitoring and maritime surveillance, is contributing to the segment's growth. The rising need for real-time data for decision-making in aviation and logistics is also a significant driver. With global initiatives aimed at improving aviation safety and the increasing adoption of next-generation radar technologies, the commercial segment is projected to grow at the fastest rate in the airborne radars market, making it a key focus area for industry stakeholders.

Ground-Based Segment is Largest Owing to Strategic Applications

The ground-based segment of the airborne radars market is the largest, owing to its strategic applications in military and civilian domains. Ground-based radars are essential for providing situational awareness and threat detection capabilities, making them indispensable for military operations, border surveillance, and law enforcement. Their ability to monitor large areas and track multiple targets simultaneously enhances the security of airspace and ground infrastructure. As nations prioritize border security and counter-terrorism efforts, the demand for advanced ground-based radar systems continues to grow.

Furthermore, technological advancements in ground-based radar systems, such as improved signal processing algorithms and enhanced detection ranges, have made them more effective in diverse operational scenarios. The integration of these radars with command and control systems allows for seamless data sharing and real-time threat assessment, further driving their adoption. As governments focus on enhancing their defense infrastructure, the ground-based segment is expected to maintain its position as the largest segment in the airborne radars market.

Space-Based Segment is Fastest Growing Owing to Satellite Technology Advancements

The space-based segment is emerging as the fastest-growing segment within the airborne radars market, primarily due to advancements in satellite technology and the increasing importance of global surveillance. Space-based radars provide extensive coverage and the ability to monitor large geographic areas, making them invaluable for military and civilian applications, including environmental monitoring and disaster management. The rising demand for high-resolution imaging and real-time data from space has prompted both governmental and private entities to invest in satellite radar systems.

Additionally, the increasing focus on climate change and natural disaster preparedness has amplified the need for space-based radar solutions. These systems play a crucial role in providing critical data for weather forecasting, climate research, and monitoring natural disasters. As more countries and organizations recognize the value of space-based radar technology, this segment is poised for significant growth, driven by technological innovation and expanding applications across various sectors.

Airborne Early Warning and Control Segment is Largest Owing to Strategic Importance

The airborne early warning and control (AEW&C) segment is the largest within the airborne radars market, attributed to its strategic importance in modern military operations. AEW&C systems are equipped with advanced radar technologies that provide real-time situational awareness, allowing military forces to detect and track aerial threats over vast distances. The increasing complexity of modern warfare and the need for integrated defense systems have heightened the demand for AEW&C platforms, solidifying their position as a critical component of air defense.

Furthermore, the growing emphasis on multi-domain operations, where military forces coordinate efforts across land, sea, and air, has driven investments in AEW&C systems. Countries are focusing on developing indigenous AEW&C capabilities to enhance their operational independence and strategic deterrence. This trend is particularly evident in regions with rising defense budgets and a focus on strengthening national security, ensuring that the AEW&C segment remains the largest in the airborne radars market.

Weather Surveillance Segment is Fastest Growing Owing to Climate Change Awareness

The weather surveillance segment is the fastest growing within the airborne radars market, driven by the increasing awareness of climate change and its impacts on weather patterns. Advanced airborne weather radars are critical for accurate weather forecasting, enabling timely warnings for severe weather events such as hurricanes, floods, and tornadoes. The growing frequency and intensity of extreme weather events have led to heightened demand for sophisticated weather monitoring systems that can provide real-time data and analytics.

Moreover, the integration of artificial intelligence and machine learning technologies in weather surveillance radars is enhancing their predictive capabilities, making them more effective in analyzing complex meteorological data. As governments and organizations invest in improving disaster preparedness and response measures, the weather surveillance segment is expected to witness robust growth, driven by technological advancements and increasing environmental concerns.

North America is Largest Region Owing to Defense Expenditure

North America is the largest region in the airborne radars market, primarily due to substantial defense expenditure and ongoing modernization efforts in military capabilities. The United States, in particular, plays a pivotal role in driving the demand for advanced radar technologies, with significant investments in defense research and development. The presence of key players in the aerospace and defense sector, coupled with government initiatives to enhance national security, contributes to the region's dominance in the airborne radars market.

Furthermore, the North American region is witnessing a growing emphasis on integrating cutting-edge technologies, such as artificial intelligence and autonomous systems, into radar solutions. This trend is supported by collaborations between government agencies and private sector companies focused on innovation. As defense budgets continue to increase and the need for advanced surveillance and reconnaissance capabilities grows, North America is expected to maintain its position as the largest market for airborne radars.

Competitive Landscape and Leading Companies

The airborne radars market is characterized by a competitive landscape comprising several key players that are instrumental in driving innovation and growth. Major companies, including Raytheon Technologies, Northrop Grumman Corporation, Thales Group, and BAE Systems, are at the forefront of developing advanced radar technologies. These companies invest significantly in research and development to enhance the capabilities of airborne radars, ensuring they meet the evolving demands of military and commercial applications.

The competitive dynamics of the market are influenced by factors such as technological advancements, strategic partnerships, and mergers and acquisitions. As companies strive to maintain a competitive edge, collaborations with governments and other industry stakeholders are becoming increasingly common. Additionally, the emergence of new players focusing on niche applications and innovative radar solutions is further intensifying competition within the market. As the airborne radars market continues to expand, the landscape will evolve, driven by the need for advanced surveillance, reconnaissance, and situational awareness solutions.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023-e) |

USD 15.1 billion |

|

Forecasted Value (2030) |

USD 25.5 billion |

|

CAGR (2024-2030) |

7.8% |

|

Base Year for Estimation |

2023-e |

|

Historic Year |

2022 |

|

Forecast Period |

2024-2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Airborne Radars Market By Component (Antenna, Transmitter, Duplexer, Receiver, Power Amplifier, Digital Signal Processor), By Platform (Commercial Aircraft, Military Aircraft, Business Jets), By Application (Defense and Security, Commercial and Civil), By Waveform (Frequency Modulated Continuous Wave, Doppler, Ultra-wideband Impulse), By Dimension (2D, 3D, 4D) |

|

Regional Analysis |

North America (US, Canada), Europe (Germany, France, UK, Spain, Italy & Rest of Europe), Asia Pacific (China, Japan, South Korea, India, and rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, & Rest of Latin America), Middle East & Africa (Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1.Introduction |

|

1.1.Market Definition |

|

1.2.Scope of the Study |

|

1.3.Research Assumptions |

|

1.4.Study Limitations |

|

2.Research Methodology |

|

2.1.Research Approach |

|

2.1.1.Top-Down Method |

|

2.1.2.Bottom-Up Method |

|

2.1.3.Factor Impact Analysis |

|

2.2.Insights & Data Collection Process |

|

2.2.1.Secondary Research |

|

2.2.2.Primary Research |

|

2.3.Data Mining Process |

|

2.3.1.Data Analysis |

|

2.3.2.Data Validation and Revalidation |

|

2.3.3.Data Triangulation |

|

3.Executive Summary |

|

3.1.Major Markets & Segments |

|

3.2.Highest Growing Regions and Respective Countries |

|

3.3.Impact of Growth Drivers & Inhibitors |

|

3.4.Regulatory Overview by Country |

|

4.Airborne Radars Market, by Components (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

4.1.Duplexers |

|

4.2.Transmitters |

|

4.3.Graphical User Interfaces |

|

4.4.Digital Signal Process |

|

4.5.Power Amplifiers |

|

4.6.Receivers |

|

4.7.Antennas |

|

4.8.Stabilization Systems |

|

4.9.Others |

|

5.Airborne Radars Market, by Platform (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

5.1.Helicopters |

|

5.2.Business Jets |

|

5.3.Military Aircraft |

|

5.4.Commercial Aircraft |

|

5.5.Aerostats |

|

5.6.Urban Air Mobility (UAM) |

|

5.7.Unmanned Aerial Vehicles (UAVs) |

|

6.Airborne Radars Market, by Waveform (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.Doppler |

|

6.2.Frequency Modulated Continuous Wave |

|

6.3.Ultra-wideband Impulse |

|

7.Airborne Radars Market, by Dimension (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.2D |

|

6.2.3D |

|

6.3.4D |

|

8.Airborne Radars Market, by Application (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

7.1.Defense and Security |

|

7.2.Commercial and Civil |

|

9.Regional Analysis (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

9.1.Regional Overview |

|

9.2.North America |

|

9.2.1.Regional Trends & Growth Drivers |

|

9.2.2.Barriers & Challenges |

|

9.2.3.Opportunities |

|

9.2.4.Factor Impact Analysis |

|

8.2.5.Technology Trends |

|

9.2.6.North America Airborne Radars Market, by Components |

|

9.2.7.North America Airborne Radars Market, by Platform |

|

9.2.8.North America Airborne Radars Market, by Technology |

|

9.2.9.North America Airborne Radars Market, by Dimension |

|

9.2.10.North America Airborne Radars Market, by Application |

|

*Similar segmentation will be provided at each regional level |

|

9.3.By Country |

|

9.3.1.US |

|

9.3.1.1.US Airborne Radars Market, by Components |

|

9.3.1.2.US Airborne Radars Market, by Platform |

|

9.3.1.3.US Airborne Radars Market, by Technology |

|

9.3.1.4.US Airborne Radars Market, by Dimension |

|

9.3.1.5.US Airborne Radars Market, by Application |

|

9.3.2.Canada |

|

*Similar segmentation will be provided at each country level |

|

9.4.Europe |

|

9.5.APAC |

|

9.6.Latin America |

|

9.7.Middle East & Africa |

|

10.Competitive Landscape |

|

10.1.Overview of the Key Players |

|

10.2.Competitive Ecosystem |

|

10.2.1.Platform Manufacturers |

|

10.2.2.Subsystem Manufacturers |

|

10.2.3.Service Providers |

|

10.2.4.Software Providers |

|

10.3.Company Share Analysis |

|

10.4.Company Benchmarking Matrix |

|

10.4.1.Strategic Overview |

|

10.4.2.Product Innovations |

|

10.5.Start-up Ecosystem |

|

10.6.Strategic Competitive Insights/ Customer Imperatives |

|

10.7.ESG Matrix/ Sustainability Matrix |

|

10.8.Manufacturing Network |

|

10.8.1.Locations |

|

10.8.2.Supply Chain and Logistics |

|

10.8.3.Product Flexibility/Customization |

|

10.8.4.Digital Transformation and Connectivity |

|

10.8.5.Environmental and Regulatory Compliance |

|

10.10.Technology Readiness Level Matrix |

|

10.10.Technology Maturity Curve |

|

10.11.Buying Criteria |

|

11.Company Profiles |

|

11.1.Raytheon Technologies Corporation |

|

11.1.1.Company Overview |

|

11.1.2.Company Financials |

|

11.1.3.Product/Service Portfolio |

|

11.1.4.Recent Developments |

|

11.1.5.IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2.Lockheed Martin Corporation |

|

11.3.Thales Group |

|

11.4.Northrop Grumman Corporation |

|

11.5.SAAB AB |

|

11.6.Honeywell International |

|

11.7.BAE Systems |

|

11.8.L3harris Technologies |

|

11.9.Boeing |

|

11.10.Airbus |

|

12.Appendix |

Let us connect with you TOC

A comprehensive market research approach was employed to gather and analyze data on the Airborne Radars Market. In the process, the analysis was also done to estimate the parent market and relevant adjacencies to major the impact of them on the airborne radars Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the airborne radars ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Estimation

A combination of top-down and bottom-up approaches was utilized to estimate the overall size of the airborne radars market. These methods were also employed to estimate the size of various subsegments within the market. The market size estimation methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size estimates, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size estimates.

Available Formats